Global| Mar 26 2015

Global| Mar 26 2015EMU Trends Turn Up for Credit and Money

Summary

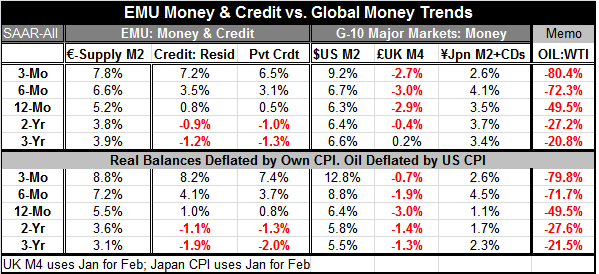

The EMU is showing a clear pick up in credit and money growth trends as of February 2015. It is beginning to look as though the ECB's special efforts to stimulate credit growth are starting to pay off. The QE effort is too recent to [...]

The EMU is showing a clear pick up in credit and money growth trends as of February 2015. It is beginning to look as though the ECB's special efforts to stimulate credit growth are starting to pay off. The QE effort is too recent to have its direct effect included in the data, but QE has been expected and other programs appear to be having some impact too.

The EMU is showing a clear pick up in credit and money growth trends as of February 2015. It is beginning to look as though the ECB's special efforts to stimulate credit growth are starting to pay off. The QE effort is too recent to have its direct effect included in the data, but QE has been expected and other programs appear to be having some impact too.

QE may be too recently implemented to have had a direct impact on the February data, but expectations of that program's adoption have been a factor behind the ongoing drop in the euro exchange rate and the lower trend of EMU interest rates. QE could be a plan having an impact before it's time. Also, in January, the ECB began to offer improved incentives on its existing lending program to banks by cutting the effective cost of four-year loans to just five basis points.

The ECB has just started QE. Still, QE is having an advance effect through expectations and its impact on the exchange rate and interest rates. Yet the weak euro does not seem to be what is driving the EMU to better economic results - at least not yet. In recent economic reports- some as up to date as for March- there is no clear evidence that the weak euro portion of ECB policy has gained traction yet. It is a bit surprising that the impact on lending has come before the impact of the weaker euro exchange rate, a process that has been in train for some time. But this could also be progress on the back of lower interest rates that has have come about also because of expectations about QE.

What to expect when you're expecting...QE

In the U.S., QE worked through four channels and it will do so in the EMU as well. QE has (1) an exchange rate effect, (2) a wealth effect, (3) an impact on lending or other private asset acquisition, and (4) an impact on interest rates and on interest rate expectations. While QE has been in place, the U.S. stock market has roared although in terms of P/E ratios that market has not gone greatly off the rails, but its expansion has progressed without seeing much in the way of the sort of pullbacks that come even in bull stock market runs. Still, the U.S. experience suggests that the wealth effect portion of QE has not been such a powerful driving force to growth. The immediate impact of U.S. QE on exchange rates was to push the dollar lower, leading to concerns expressed especially by developing countries that the U.S. was running a beggar-thy-neighbor policy. But these same countries cried `wolf' when the U.S. announced its plan to stop expanding these programs as well, an effect known as the taper-tantrum. While the U.S. has not yet unwound any of its QE purchases, the dollar has reversed course and it is rising strongly while the euro is plunging. U.S. policy seems headed for higher rates (and an eventual, if distant, unwind of QE) while the EMU is just embarking on its QE program. Of course, the QE effect on U.S. interest rates lingers but is dissipating while in Europe's QE is hitting markets in full force, aided by special ECB lending programs.

Still, the news for euro-data is that even the March PMI reports from Markit show that the services sector for the EMU and well as for the largest EMU members is outperforming the manufacturing sector. This is despite the fact that manufacturing is the sector most likely to respond to a sharply weakening euro.

The upturn in European data seems to be mostly on domestic-based measures. Still, there is a big difference between how Germany is responding and how other EMU members are responding making it important to go behind the scenes of aggregated EMU-area data to see what is happening on the member country level. There, the evidence still points to a recovery that is led more by domestic factors than one that is being induced by a performing export sector. Of course, Europe's banking sector is still somewhat rag-tag with many banks still needing to raise capital levels. Yet evidence shows that banks are taking up loans from the ECB and that commercial banks are on lending funds to the private sector. All of this is in advance of whatever direct effect QE might eventually bring.

The ECB must be pleased with the results. Forecasts have been ramping up for German growth and even France has elevated its outlook and indicated improved prospects for budget deficit reduction for the year ahead. Greece continues to hang in the balance and is a potential risk to the outlook.

For the time being, the flow of information and the timing of the rebound suggest that the ECB polices are having effect. It is always hard to say if that is really the case or if there had been some rebound in place in any event as Europe recovered from the multiple effects of Russian sanctions over the past year. But for now the timing certainly makes it seem as if the ECB policies are at work.

The fact that the international sector and the tradable goods sector (manufacturing) are not pushing the European economies ahead the most suggests that the apart of QE that works through exchange rates still has not taken hold and that is reason for some further optimism on the outlook. It is entirely possible that the wealth effect in Europe will be greater than it was in the U.S., but European stock markets have only just started to find their footing. It is hard at this point to say that stock market improvements in Europe are the cause of other economic improvements (such as in confidence and output) and it is more likely that cause and effect have worked the other way around. Stock markets are improving because the European economy is improving and because interest rates are falling and have even crashed through the zero-bound in some cases.

In terms of looking at the various channels through which QE and the ECB special loan program works, it appears that the ECB is still in the very early stages of stimulus and yet is starting to see some substantial impact from its polices on the exchange rate, lending, equity markets and interest rates. A number of EMU instruments are bearing negative interest rates and that will reinforce exchange rate weakness. The EMU QE program as announced is large enough to give investors hope; it was launched as a potentially open-ended plan giving it more potential to affect outcomes in markets. I would say that the program is having impact beyond even Mr. Draghi's wildest dreams. The question is whether Europe can keep it up. In the early stages, U.S. QE seemed to be having a substantial effect too, but after several rounds of QE it seemed to lose its effectiveness. So Europe still bears a good deal of watching. But it is easy to conclude this: so far so good.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief