Global| Mar 18 2019

Global| Mar 18 2019EMU Trade Surplus Expands on Weak Import Rise

Summary

In the EMU, both import and export gains were modest in January. Imports rose by just 0.3% while exports gained 0.8%, expanding the monthly surplus in January to 17.04 billion euros from 16.02 billion euros in December. The surplus [...]

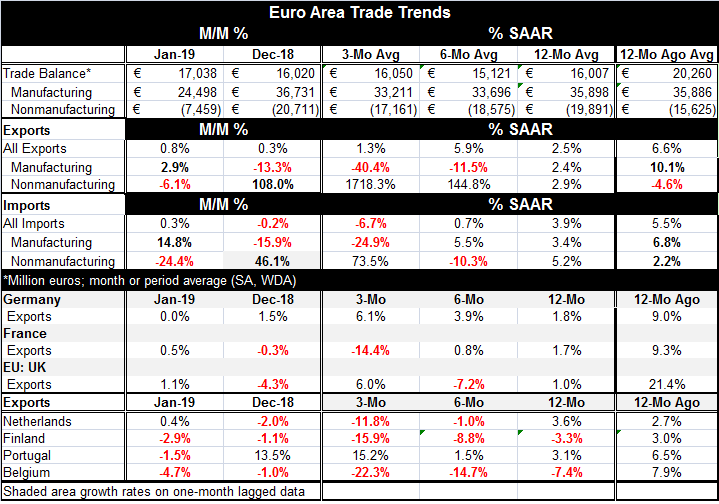

In the EMU, both import and export gains were modest in January. Imports rose by just 0.3% while exports gained 0.8%, expanding the monthly surplus in January to 17.04 billion euros from 16.02 billion euros in December. The surplus was down from 20.26 billion euros one year ago.

In the EMU, both import and export gains were modest in January. Imports rose by just 0.3% while exports gained 0.8%, expanding the monthly surplus in January to 17.04 billion euros from 16.02 billion euros in December. The surplus was down from 20.26 billion euros one year ago.

However, there was still a lot change going on among EMU trade flows. The balance of trade for manufactures plunged to a surplus reading of 24.5 billion euros in January from 36.7 billion euros in December while the balance on nonmanufactures trade contracted sharply to -7.5 billion euros from -20.7 billion euros. The surplus on manufactures trade was down sharply from 35.9 billion euros one year ago while the deficit on nonmanufactures trade was down sharply from -15.6 billion euros one year ago. These are striking and largely offsetting changes. While these shifts are extreme, the EMU has a history of such large changes occurring in January within the manufacturing and nonmanufacturing sectors. Historically, most of the time these shifts are meaningless and do not signal a trend change.

In January exports of manufactures are plunging and decelerating sharply from 12-months to 6-months to 3-months while nonmanufactures exports are accelerating sharply. And, both of these ‘trends’ are sharply opposed by the movement of nonmanufactures and of manufactures exports in the month of January. For imports there are no clear trends but manufacturing imports are off sharply over three-months while nonmanufactures imports are up extremely strongly over three-months.

In January, export trends among European countries have mixed trends. France, the U.K. and the Netherlands show export increases while Finland, Portugal and Belgium log declines. German exports are flat month-to-month in January. But viewed over three months, the tilt is to weakness with double-digit annualized rates of export declines in France, the Netherlands, Finland, and Belgium. On that same three-month period, Portuguese exports are rising at a 15% annual rate while U.K. and German exports rise at abut a 6% annual rate. Trends also are mixed over six months while over 12 months exports still are rising in five of seven of these countries (Finland and Belgium are the exceptions).

In January, export trends among European countries have mixed trends. France, the U.K. and the Netherlands show export increases while Finland, Portugal and Belgium log declines. German exports are flat month-to-month in January. But viewed over three months, the tilt is to weakness with double-digit annualized rates of export declines in France, the Netherlands, Finland, and Belgium. On that same three-month period, Portuguese exports are rising at a 15% annual rate while U.K. and German exports rise at abut a 6% annual rate. Trends also are mixed over six months while over 12 months exports still are rising in five of seven of these countries (Finland and Belgium are the exceptions).

In Asia today, Singapore reported a recovery in exports for February after a decline over the previous three months; its nonoil domestic exports expanded by 4.9% year-on-year. In Japan, exports fell by 1.2% year-on-year in February. The Baltic dry goods index continues to point to weak global trade.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief