Global| Aug 22 2017

Global| Aug 22 2017EMU Trade Surplus Bounces to Six-Month High

Summary

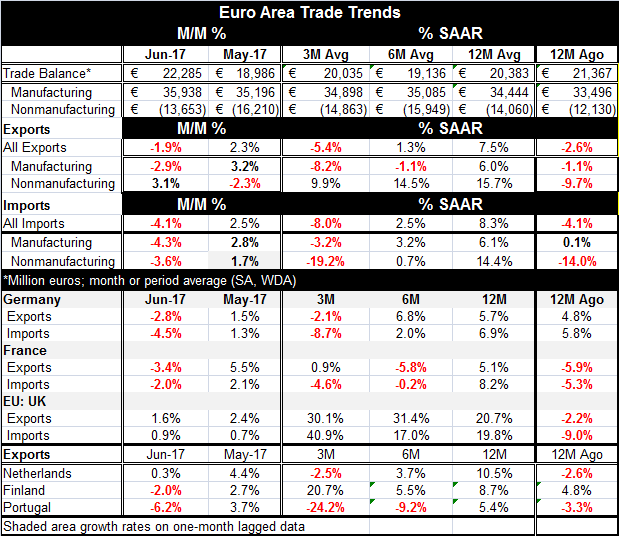

A sharp drop in imports pushed the EMU trade surplus to a six-month high. The trade surplus rose to 22.3 billion euros in June from 19.0 billion euros in May, to its strongest point since logging a surplus of 23.0 billion euros in [...]

A sharp drop in imports pushed the EMU trade surplus to a six-month high. The trade surplus rose to 22.3 billion euros in June from 19.0 billion euros in May, to its strongest point since logging a surplus of 23.0 billion euros in December of last year. It is the ninth highest surplus on record and not the direction in which the United States wants to see the European surplus moving. EMU import growth had ramped up, but now that process has unraveled.

A sharp drop in imports pushed the EMU trade surplus to a six-month high. The trade surplus rose to 22.3 billion euros in June from 19.0 billion euros in May, to its strongest point since logging a surplus of 23.0 billion euros in December of last year. It is the ninth highest surplus on record and not the direction in which the United States wants to see the European surplus moving. EMU import growth had ramped up, but now that process has unraveled.

The surplus on manufactured goods got larger by about 800 million euros in June while the deficit on nonmanufacturing was reduced by about 2.6 billion euros. Most of the surplus' gain came outside of the manufacturing area and oil was a substantial contributor to this result as oil prices have been easing on this horizon. But the surplus on manufacturing also rose.

On the month, manufactured goods exports fell as the exports of nonmanufactures rose. The relatively larger gain in nonmanufactures exports did not overcome the smaller rise in manufactured goods which applied to a larger flow of goods trade; thus, overall exports fell by 1.9% on the month. For imports, both manufactures and nonmanufactures imports fell. Both manufacturing and nonmanufacturing import flows fell sharply, nonmanufactures by 3.6% and manufactures by 4.3% as total imports fell by 4.1% month-to-month.

Sequential growth rates from 12-month to six-month to three-month find exports decelerating for both manufacturing and nonmanufacturing flows. Overall imports are also decelerating on decelerations of both manufacturing and nonmanufacturing flows. However, these flows are not likely to stay in this configuration since all flows except nonmanufacturing exports are showing declines over three months and that result is certain to be reversed soon as the EMU economy clearly is not in recession. What we are seeing is some realignment of growth rates to a more sustainable speed.

Country level data show mixed trends. But for the EMU, Germany and France, nominal imports are growing faster than nominal exports over 12 months. For the U.K., the two flows are at nearly the same speed.

France, Germany, Finland and Portugal join EMU overall exports showing declines in the month. The U.K. and he Netherlands show exports higher.

While weaker imports - imports of nonmanufactures- seem to be the main driving force for the EMU trade balance this month, the surplus on manufacturing also is advancing. The EMU and Germany already have a high current account to GDP ratio. While Angela Merkel has said that the German surplus was on a declining path, since she made that statement there has been a revival in the German and EMU surpluses. This month EMU has logged one of its highest surpluses on record obviously supported by a large underlying surplus on trade in Germany. Something is going to have to give. The Trump administration is now on its war-path over trade as it has engaged China and started its negotiations with NAFTA members in North America. Soon its attention will turn to Europe and the entrenched surplus on the trade accounts there.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief