Global| Dec 03 2014

Global| Dec 03 2014EMU Total PMIs weaken...on trend

Summary

The manufacturing and services sectors for EMU are weakening and are staying on their recent trends as they do so. Conditions are weak and headed to get weaker. While there are many distortions in the global economy there are also [...]

The manufacturing and services sectors for EMU are weakening and are staying on their recent trends as they do so. Conditions are weak and headed to get weaker. While there are many distortions in the global economy there are also many things we can look at to try and find a consistent or coherent picture of what is really going on. We can look at PMI trends, oil price trends, stock market trends and currency trends to try to puzzle out what is really in train. When we make all these assessments, we see that there will be more weakness ahead. The PMI signals do not stand alone, far from it.

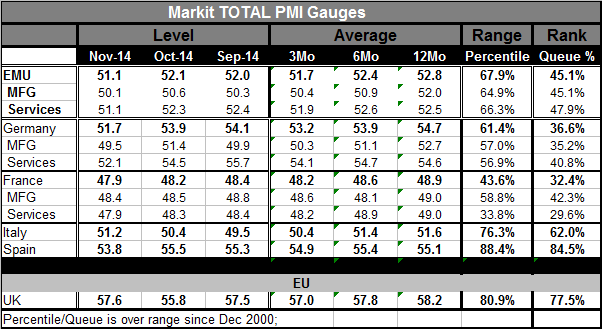

PMI Trends: First let's look at those PMI trends. In the table the overall private sector PMI values for EMU, Germany and France all show consistently deteriorating averages as we move from the 12 month average to the six month average to the 3 month average. In addition, each of these countries/entities current month's total PMI value is below its topical 3 month average. These are very clear signs of a deteriorating trend. Italy is a minor exception among the Big-3 economies as its sequential averages are declining but its current month's value is above its topical 3 month average. Spain alone has sequential averages that are improving but its current reading is below its 3 month average and has dropped sharply this month. In short there is not much here in the way of trends to create any optimism. For Germany, France and the EMU the sector by sector take on these same metrics is also weakness, even if the sector indices are not so monotonically clear in their decline. But the message is in fact delivered by each sector that there is no revival in train - anywhere.

The chart above shows the sector plots for the service sector, the new release that allows us to calculate the total PMIs today. The services reading in Germany is collapsing. France and the e-Zone are deteriorating. Italy has traced a jagged pattern and has rebounded this month- but it does not do so in the context of a rising trend, but rather in the context of ongoing sideways volatility.

The exchange rate: If we look at the euro exchange rate, it has fallen to a two year low. This is not a sign of health. As I have written before, this weakness is perverse since the EMU area, and Germany in particular, has a huge current account surplus. This currency rate fall will only make these surpluses even larger and exacerbate international imbalances in doing so (a bigger EMU surplus mean a bigger deficit somewhere else to compensate). So the EMU's 'need' for stimulus is being met by the euro's fall but the global economy is made worse off for it. Recall that global capital flows supporting large current account imbalances were behind the last financial crisis.

Oil market: Oil is not a variable specific to Europe but weak oil prices are a symptom of a fractious relationship in OPEC and of weaker global demand conditions. Demand weakness has created this situation that OEPC cannot sort out. China has slowed, Europe is slow, the U.S. is 'doing better' but is still not very solid; the BRICS are challenged. As a result energy demand is back on its heels just as new energy supplies are being brought to market.

There are plenty of two-way bets on how this works out. You can see that when the oil price is in the $65/bbl to $70/bbl range oil starts to find a bid. Some still bet we will see $40/bbl others think it's more likely that we see $100/bbl next.

The Fed calls the lower oil price impact on inflation 'temporary;' the IEA says there is a regime change and oil prices are going to stay lower. No one knows. But prices for now are in the "things are weak" camp.

Equity markets' message: Stock markets are doing okay in this environment. But the message there is tangled in an ugly mess of how the economy is doing, how it is expected to do and of expectations for continued near-zero interest rates. We need to dig deeper to see the true message. Stock indices have set records in the U.S. and Japan (A seven year high in Japan). The year to date rise in U.S. equities is solid. But the leadership in U.S. equities is not impressive. European markets have momentum problems. If you are reacting to news of all-time highs for indices learn to ignore that. It's momentum that matters and while momentum in the U.S has been restored, the best performing 10-S&P sectors are (1) health care, (2) Info-tech, (3) Utilities and (4) consumer staples. Only one of these sectors gives me any confidence as a leading sector. Healthcare is a regulation play. Utilities are a yield play and usually- along with consumer staples- a defensive pick. Consumer discretionary stocks, materials and industrial stocks are in the bottom four among the 10 S&P sectors. That's not a good sign. In Europe among eleven markets of the first EMU member counties (exclude Luxembourg, and add Greece) finds three of eleven are down from end 2013. Germany, France and Italy haves stock indices that are (as of late November) up by less than 6% year to date.

Summing up: One again, it's hard to extract good news from market behavior. It's even worse if we try to rationalize bond yields. Bond markets tell us that conditions are poor and/or that in Europe some huge monetary stimulus is expected. Maybe it will come. Maybe Mario Draghi can get his way and will deliver more stimulus. But it is far from clear that he has a way to get around the restrictions that bind the ECB's actions. The hard money members of the ECB seem as hard-headed as ever in opposition. All signs point to continued rough sledding ahead.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief