Global| Apr 15 2013

Global| Apr 15 2013EMU Surplus Improves on Weak Imports

Summary

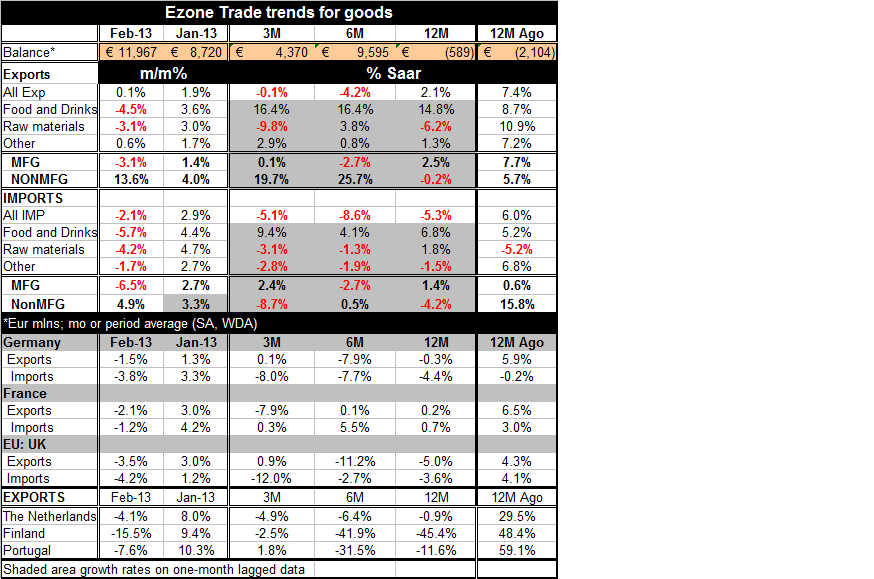

In the European monetary union for the month of February the merchandise trade balance improved sharply. Exports in the month edged higher rising by 0.1%. The driving factor for the trade improvement was the decline in imports. [...]

In the European monetary union for the month of February the merchandise trade balance improved sharply. Exports in the month edged higher rising by 0.1%. The driving factor for the trade improvement was the decline in imports. Imports fell by 2.1% in February and fell across all of the major import groups.

In the European monetary union for the month of February the merchandise trade balance improved sharply. Exports in the month edged higher rising by 0.1%. The driving factor for the trade improvement was the decline in imports. Imports fell by 2.1% in February and fell across all of the major import groups.

Trade in the Zone is weakening. Manufacturing imports and exports fell in February. Manufacturing exports fell by 3.1%, imports fell by an outsized 6.5%.

Year-over-year, exports are growing by 2.1% while imports are shrinking by 5.3%.

Looking at some of the individual countries, exports fell on the month for Germany, France, the UK, the Netherlands, Finland and Portugal. For the same group, exports rose over three months for three of them. Exports rose at a 1.8% pace for Portugal, at a 0.9% pace for the UK and at a thin 0.1% annual rate for Germany. Exports fell at a 2.5% pace for Finland, at 4.9% pace for the Netherlands and at a 7.9% pace for France. For the same group of countries exports are lower year-over-year with the exception of France, which shows a very narrow 0.2% rise over 12-months.

In February imports in Germany, the UK and France are all declining. Over 12 months German imports are down by 4.4%, UK imports are down by 3.6% and French imports are up by a thin 0.7%.

Export and import flows in the Eurozone show a great deal of weakness. Weakness is much worse for manufacturing products. There isn't much sense of domestic demand holding up based on evidence from trade flows.

Over the weekend concerns began to mount that Slovenia may have some additional problems but we are being told that Slovenia's problems are nothing like Cyprus. It's not a reassuring comparison.

In Germany to the special "wise men" that advise Angela Merkel are arguing that the countries of southern Europe actually have greater per capita wealth than in Germany and that those countries should implement wealth taxes to pay for their own economic difficulties. Advisors professors Lars Feld and Peter Bofinger claim that there's enough wealth in the private assets across the Mediterranean to cover their bailout costs. They argue that the rich must give up part of their wealth over the next 10 years.

With other news reports tracking the development of a German anti-eurozone party that is trying to get on the ballot in these elections, it's clear that the tone in the eurozone has turned to separatism. It's hard to see why the countries of the South would agree to a wealth tax to solve their debt problem when that would not solve their competitiveness problem leaving them to continue to stumble along at weak growth rates in the Eurozone paradigm.

This new tact from Germany, if it's a real policy move supported by the administration, seems to be another push intended to get the Mediterranean countries to make the jump out of the Eurozone. There is nothing in this new plan to help the circumstances of the Mediterranean countries. It's a plan that clearly would benefit Germany above all other EMU members. Bofinger commented on the Cyprus plan saying that taxing bank deposits was the wrong way to go, but his tact was to note that people can move their bank deposits to banks in the North. It doesn't appear that he had any problem with the idea of taxing bank deposits per se, he's more in favor of taxing wealth, to the extent that you can pin down a measure of wealth that can't be moved.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief