Global| Jun 21 2019

Global| Jun 21 2019EMU Sector Bifurcation Continues

Summary

There is an old song with a verse about the rich getting richer and the poor getting poorer. The EMU manufacturing and services sectors seem to be following that script. Services are continuing to move higher boosting the composite [...]

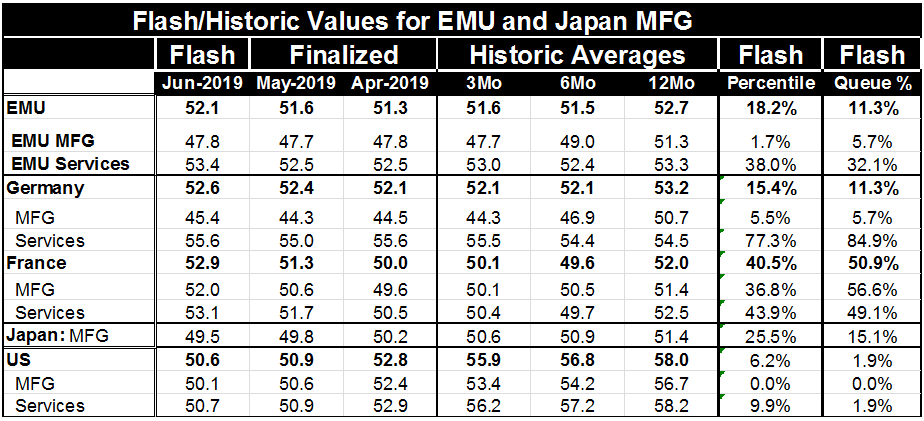

There is an old song with a verse about the rich getting richer and the poor getting poorer. The EMU manufacturing and services sectors seem to be following that script. Services are continuing to move higher boosting the composite private sector index. But manufacturing remains weak, below the PMI level of 50, still in a contracting mode despite a one-tick improvement in its PMI reading for June.

There is an old song with a verse about the rich getting richer and the poor getting poorer. The EMU manufacturing and services sectors seem to be following that script. Services are continuing to move higher boosting the composite private sector index. But manufacturing remains weak, below the PMI level of 50, still in a contracting mode despite a one-tick improvement in its PMI reading for June.

However, even with the rebound in services EMU is not doing well. The composite has a five year ranking in its 11th percentile. Manufacturing has a 5.7 percentile standing. And the strengthening service sector at a 32 percentile standing is still stuck in the lower third ot its recent queue of values.

Various political trends intrude French President Emmanuel Macron today snipped at Jens Weidmann the head of the Bundesbank for being such a Johnny-come-lately to the approval of the ECB bond buying process. There is a competition to replace Mr. Draghi and clearly Macron does not see it as the right time to install a rules-bound German to the top ECB position with growth still so lacking even with inflation so baldy undershooting.

There are further problems in the EU as well as new leadership needs to be chosen. Here again Macron was active again opposing Angela Merkel’s choice. None of the proposed candidates to head the EU could gain a majority of votes. So the in the wake of European elections the EU is having a hard time getting its leaders and new members in parliament to agree to new leadership.

At the same time the Prime Minister election process proceeds in the UK with Boris Johnson the clear leading candidate in a field whittled down to two. Donald Tusk has once again stated his position that the EU’s Brexit position has been made clear. It is not clear at all what Boris Johnson will be able to do with the Brexit process if he does emerge victorious and become the new UK Prime Minister. Tusk said that a new British prime minister may enliven Brexit but will not change the EU. The EU Commission did decide it would not reopen for negotiation the terms of the UK exit which is already established in a withdrawal agreement between the two parties.

Between the rules-setting portion of the EU and monetary policy-making portion of the EMU there is still a lot in flux in Europe. The unfinished business with the UK simply adds another bit of unknown to an already hard to define process.

Back to economic trends This month the German economy showed small improvement in its two PMI gauges but manufacturing continues to contract. The manufacturing sector grades out with a 5.7 percentile standing, the same as for EMU as a whole but the German service sector has a very robust 84.9 percentile standing on a measure that is nonetheless only one point above its 12-month average. The German composite logs an 11 percentile standing.

France’s sectors are positioned very differently with a composite ranking at its 50.9 percentile and with a manufacturing sector that has a higher percentile standing than that for services. The French manufacturing sector has a diffusion reading of 52 up solidly from 50.6 in May and that lift brings its percentile standing up to its 56.6 percentile. Services that also improve on the month have a percentile standing at their 49.1 percentile level, a touch below their median.

Elsewhere Japan’s MFG PMI slipped in value and continues to show sector contraction.

In the US manufacturing slipped and achieved expansion by the thinnest of margins while the service sector also eroded and closed in on a reading close to stagnation. The US MFG reading is the lowest on this 5-year time line with manufacturing at its 1.9 percentile standing, also very low.

On balance the sector readings from Markit are not reassuring except in so far as the unraveling is not worse. If the trade war worsens we would expect deteriorated results in manufacturing. But for now the good news is that the service sector has been able to endure and improve even in the face of deteriorating conditions in manufacturing. However, a number of important ‘administrative issues’ remain in both the UK and in the EU that could yet affect how events unfold quite apart from any external influences. The UK will also be looking for a new head of the BOE soon.

The global setting The PMI results for the US in June seem to show some slight but further deterioration. US regional manufacturing surveys have already been carving out that lower ground. Meanwhile geopolitical events heated up this week with Iran shooting down a US drone and with both sides arguing about where that drone was when it was shot down. For now cooler heads have prevailed and US President Donald Trump who claims the drone was in international airspace says it was shot down in error. He also said the response the US had would not have been proportional to what Iran had done accounting for his decision to stay any retaliation for now. However, the air space is being treated as if it is a theater of war as commercial aircraft are changing their routes to avoid certain portions of Iranian airspace. Meanwhile the G20 is ready to meet as are the US and China and soon we will have some real answers on trade progress.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief