Global| Jun 04 2008

Global| Jun 04 2008EMU Retail Spending and Plans Continue to Roll Over

Summary

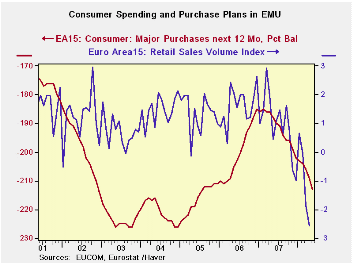

Euro Area retail sales are weak in April just as they were in March and in February. It’s no surprise then that one month into the new quarter Retail sales volumes are falling at a 7.6% annual rate, led by an 8.3% volume drop in [...]

Euro Area retail sales are weak in April just as they were in

March and in February. It’s no surprise then that one month into the

new quarter Retail sales volumes are falling at a 7.6% annual rate, led

by an 8.3% volume drop in nonfood items.

The sequential growth rates for the main aggregates (total,

food and nonfood) show clearly accelerating weakness in retail sales.

It is not hard to see why the OECD cut its forecasts in its new

projections released on Wednesday.

The consumer, his sentiment and his spending habits, are under

clear pressure. Europe’s industrial measures have been held aloft by

strength in capital spending, but it’s time to wonder what is keeping

that aloft. In Japan, a country as well plugged into the overseas

growth markets as any, cap-ex spending turned weak again in the recent

government survey.

Europe seems to have even harder times ahead, made harder

still by and an inflexible ECB over what are actually moderate

inflation pressures during very unusual times with steeply spiking oil

prices. The Fed has not exactly been a fountain of ease but it has done

a lot more for the US economy than that one-trick pony known as the ECB

has done for Europe. Spare the rate, spoil their fate.

| Euro Area (13) Retail Sales Volume | ||||||

|---|---|---|---|---|---|---|

| Apr-08 | Mar-08 | Feb-08 | 3-Mo | 6-MO | 12-Mo | |

| Euro 13 Total | -0.6% | -0.9% | -0.2% | -6.8% | -3.5% | -2.6% |

| Food | -1.0% | -0.3% | 0.1% | -4.7% | -4.3% | -3.4% |

| Non food | -0.5% | -1.2% | -0.4% | -8.2% | -3.0% | -2.0% |

| Textiles | #N/A | -5.0% | 1.1% | -8.5% | -11.4% | -5.0% |

| HH Goods | #N/A | -1.2% | -0.2% | -4.3% | -3.6% | -2.9% |

| Books news, etc | #N/A | -1.5% | -0.2% | 1.8% | 0.2% | -0.3% |

| Pharmaceuticals | #N/A | -0.3% | 0.4% | 2.0% | 1.9% | 2.8% |

| Other NonSpec | #N/A | -1.2% | 0.2% | -1.1% | -1.9% | -2.0% |

| Mail Order | #N/A | -1.3% | -1.1% | -8.2% | -0.8% | 0.1% |

| Non-Food Country Detail Volume | ||||||

| Germany | -4.2% | -1.4% | 1.1% | -16.7% | -4.9% | -4.2% |

| France | #N/A | -1.1% | 0.0% | #N/A | #N/A | #N/A |

| Italy (Total; Value) | #N/A | -0.5% | 0.2% | -0.7% | -0.2% | -0.5% |

| UK(EU) | -1.6% | -0.1% | 1.8% | 0.4% | 4.3% | 4.8% |

| Shaded areas calculated on a one-month lag due to lagging data | ||||||

| The EA 13 countries are Austria, Belgium, Finland, France, Germany, | ||||||

| Greece, Ireland, Italy, Luxembourg, the Netherlands, Portugal, Slovenia | ||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief