Global| Aug 03 2017

Global| Aug 03 2017EMU Retail Sales Show Acceleration

Summary

Euro area retail sales volume rose for the second month running in June, gaining 0.5% month-to-month in the wake of a 0.4% month-to-month rise in May. Total euro area retail sales volume is up at a 3.5% pace over three months, just a [...]

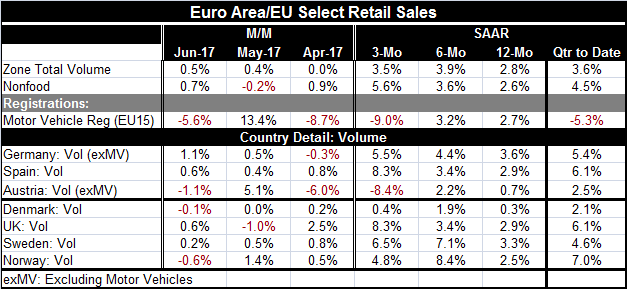

Euro area retail sales volume rose for the second month running in June, gaining 0.5% month-to-month in the wake of a 0.4% month-to-month rise in May. Total euro area retail sales volume is up at a 3.5% pace over three months, just a tad slower than its 3.9% gain over six months and well ahead of its 2.8% pace over 12 months. Excluding food, retail sales volume does not have consecutive monthly gains, but the sequential growth rates on that basis show clear sales acceleration with a strong 5.6% pace over three months compared to 2.6% over 12 months.

Euro area retail sales volume rose for the second month running in June, gaining 0.5% month-to-month in the wake of a 0.4% month-to-month rise in May. Total euro area retail sales volume is up at a 3.5% pace over three months, just a tad slower than its 3.9% gain over six months and well ahead of its 2.8% pace over 12 months. Excluding food, retail sales volume does not have consecutive monthly gains, but the sequential growth rates on that basis show clear sales acceleration with a strong 5.6% pace over three months compared to 2.6% over 12 months.

Solid retail gains in Q2

With second quarter data now complete, retail sales volume is up at a 3.6% annual rate in Q2 while ex-food volumes are up at a stronger 4.5% pace.

Motor vehicles

Motor vehicle registrations in the EU are slower on this same timeline. Registrations fell by 5.6% in June but are still up by 2.7% over 12 months.

Europe generally is doing well

Seven representative European economics (see Table) show sales volumes rising in four of them in June after sales rose in five of them in May (unchanged sales in Denmark in May). Among this grouping, all countries saw sales gains over three months except Austria. And all of them show increases over six months and over 12 months. Growth rates for retail sales volumes are accelerating from 12 months to six months to three months for EMU members Germany and Spain. They are also accelerating for the U.K. despite that economy's recent difficulties.

BOE keeps policy steady on another split vote

At today's Bank of England policy meeting, the Monetary Policy Committee held steady again on another split vote. But the BOE warned of faster future rate hikes than the market has been expecting. It also warned that depending on monetary policy actions inflation could overshoot its target of 2% for the next three years. BOE Governor Mark Carney warned about the effects over the uncertainty regarding Brexit.

Brexit uncertainty will get worse before it gets better

Brexit will continue to loom as an issue for both the U.K. and Europe. So far, the U.K. is seeing mostly adverse consequences and we have mostly fielded stories of how the EU is benefiting as UK-based financial firms in particular are moving at least some operations to other EU members in preparation for Brexit and its likely new restrictions on UK-based operations.

Composite PMI readings

Today's reports also fielded some fresh PMI observations on services and for composite PMIs where those reports are extant. The euro area showed an unchanged services sector to go with its somewhat weaker manufacturing reading and a lower composite reading for July. The German and French composite PMI readings were lower, Germany on weaker manufacturing and services and France on weaker services, despite an uptick in manufacturing. The gauge for Italy rose on the back of a 10-year high reading for its services sector. Spain's composite stepped back on weaker manufacturing and weaker services. Still, the readings across the EMU are uniformly high for its largest economies in both manufacturing and services with the odd exception that the German services sector has a reading substantially below its median of the last five and one-half years. In comparison, the U.K. composite reading improved in July, but it has a standing below its historic median although the PMI gauge itself is comfortably signaling ongoing expansion.

Policy in EMU

The step down for PMI readings in the EMU is not surprising given that there has been such a substantial recovery in place. GDP growth actually ticked up in the EMU in Q2. Growth is not the fly in the ointment for Europe. For policy, the issue is whether inflation will move back up to target and how the ECB will deal with below-target inflation if it does not, in an environment where growth seems to be more even-keeling. There is also a substantial recovery and ongoing improvement across the EMU for unemployment rates from cycle highs reached in the recession.

Got Inflation? Policy changes...anyone?

For now only the U.K. has an inflation 'problem,' at least in the classical sense. The U.K.'s dilemma is one of its own making as its jolt of post Brexit-vote stimulus unseated the pound sterling and that has affected inflation adversely through rising import prices more than it has stimulated growth. For now the BOE is playing its own version of the waiting game that is also being played by the ECB and the Federal Reserve, to some extent. Inflation is undershooting central bank targets in major money centers globally as the U.S., the EMU and Japan all are below target and with inflation momentum against them to boot. Oil prices, however, could change that. For now it is a time for sorting out and watching to see if central banks are going to alter their posture despite low inflation because growth seems somewhat more reliable even though it is not really any faster. Today the BOE noted that rates would probably rise faster in the future than the market had been thinking. The ECB is ready to revisit its policy options in September. The Federal Reeve has put balance sheet shrinking at the top of its policy list and will start to do that soon while it apparently will hold off the next rate hike until December. The Bank of Japan is simply holding policy steady with stimulus while Prime Minister Abe has just shuffled his cabinet in an effort to regain his popularity and control.

Shaking the tectonic geopolitical plates

The geopolitical situation, however, is worsening- heating up. The U.S. did step up sanctions on Russia as Congress passed legislation that will also take the President out of the driver's seat of control. The latest bill has upset the Germans who are afraid it interferes with their ability to maintain Russian pipelines which are the main source of their energy delivery. There is (for once!) bipartisan support in the U.S. for the President who is getting ready to take an aggressive trade stance against China. Meanwhile, U.S. NAFTA negotiations also are pending. There has been some stepped up border activities around the Baltics and Ukraine. North Korea continues to advance its missile tests; Iran and the U.S. also have a dispute about whether Iran's own testing has been a violation of their agreement. Venezuela appears lost to democracy. The U.S. State Department has issued a travel ban to North Korea. There have been naval encounters in the Persian Gulf. So while the monetary policy side is uncertain and marking time and the macro economy seems to be more stable, the geopolitical background has certainly picked up the slack when it comes to instability. And that is without mentioning the domestic political issues playing out within the U.S. political system. And don't worry; I am not leaving out Europe because it will always have Brexit and ongoing snits over NATO.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief