Global| Apr 12 2021

Global| Apr 12 2021EMU Retail Sales Jump, Regaining Some of the January Drop

Summary

February finds EU retail sales and motor vehicle registration rebounding after having logged even more severe drops in January. As a result, despite the substantial boost this month, retail sales and vehicle registrations are still [...]

February finds EU retail sales and motor vehicle registration rebounding after having logged even more severe drops in January. As a result, despite the substantial boost this month, retail sales and vehicle registrations are still lower on balance over the two months.

February finds EU retail sales and motor vehicle registration rebounding after having logged even more severe drops in January. As a result, despite the substantial boost this month, retail sales and vehicle registrations are still lower on balance over the two months.

The graph is the best way to visualize the path of retail sales and vehicle registrations that have bounced around with such vigor and erraticism that it becomes hard to figure out where they are on balance. To help ease the way through this labyrinth of ups and downs, the graphic plots the level of sales and the number of registrations rather than monthly or annual percentage changes.

The graph clearly shows the plummeting of sales and registrations when the virus struck and countermeasures were launched. It then shows a sharp rebound that stops short of its pre-covid-19 levels for vehicle registrations and then turns lower suffering another but not quite as severe drop in January 2021. Retail sales rebounded in the wake of the virus and the rebound carried on up to a fresh peak August – October then began process of multi-month unraveling falling to a new low in January that is the weakest reading since April 2020.

The EMU clearly shows a two stage economic hit from the virus with the first leg being the one that was in global synchrony in April 2020 and with the second related more to European specific issues although many countries globally have been hit by more than one wave of virus that impacted the economy as well.

Europe's most recent covid-19 wave has hit it hard. The United Kingdom (which has never been part of the common currency union and is no longer part of the EU) has just removed its recent lockdown allowing shopping and a return to greater conditions of freedom and normalcy. The reopening of England's shopping districts shows that they have drawn crowds on Monday, with ‘footfall' across all U.K. retail destinations jumping 218% compared to a week ago. This is according to data from Springboard (Source).

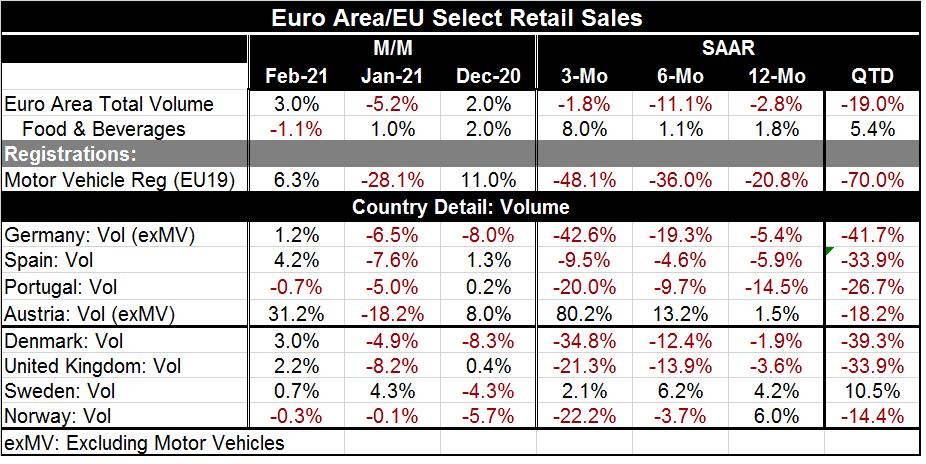

Despite the ups and downs of retail sales and vehicle registrations over the past year, the sequential growth calculations over 12 months, six months and three months show consistent declines. But that is more a function of the ‘luck of the draw' as far as the calculations themselves are concerned. Total retail volume losses are at -2.8% over 12 months expand to drop at a -11.1% annual rate over six months then diminish to a -1.8% annual rate over three months.

The bottom panel of the table shows retail sales volume patterns for some other early-reporting European countries. Among these eight countries, only Austria and Sweden show retail sales values expanding on all horizons. Again, let me caution that during this period sales have been erratic everywhere and the data this month are based on the growth rates from the selected touch points (three-month, six-month and 12-month in the past) and these may or may not be representative of true underlying trends. While that caveat is always true and it is one of the reasons that we present growth rates over various horizons, that approach is not fail-safe when data become volatile, as they have been.

Apart from Austria and Sweden, the other countries in the table show negative growth rates on just about every horizon. Among the eight countries in the table plus the euro area over all (bringing the total to nine entities), only Sweden shows sales volumes rising in the current quarter-to-date. Sweden shows sales rising at a double-digit rate while all other countries and the euro area show declines at a double-digit pace (QTD) in Q1 2021.

Europe has been battling the virus less effectively than the U.S. recently especially with regard to vaccinations. The clear exception in Europe is non-EU member the U.K. that has made great progress in vaccination and does so with the more virulent form of the virus in train. But much of Europe is lagging on its vaccination progress and that makes it more vulnerable to reinfection cycles and potentially to more stop-go economic policies.

Retail sales in the U.S. have been raining down strength in the wake of multi-level stimulus programs and a vaccination program that is making progress and going full bore, building on the base of Operation Warp Speed developed under the Trump administration. The shutting down of much of the U.S. service sector pushed relatively more purchases made as a result of income maintenance plans into the goods sector of the economy which allowed U.S.-based stimulus to leak out and help other economies such as those in Europe as well as Japan and China as U.S. imports have surged. The U.S. has been an important cog in keeping the global economy afloat. But as the U.S. service sector recovers and opens up relatively less of U.S. stimulus will be augmenting growth in Europe and in other economies across the globe. Europe will be forced to lean on its own recovery process.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief