Global| Jul 30 2009

Global| Jul 30 2009EMU Recovery Continues

Summary

BETTER: The EU commission indices for EU and EMU continue to show substantial progress. The EU index rose to 75.0 from 71.1 while the EU index rose to 76.0 from 73.2. The better showing in the EMU rise implies a better rise in the [...]

BETTER:

The EU commission indices for EU and EMU continue to show substantial

progress. The EU index rose to 75.0 from 71.1 while the EU index rose

to 76.0 from 73.2. The better showing in the EMU rise implies a better

rise in the month by non EMU members of EU. On a mo/mo basis the UK

index did rise sharply by 7.3% compared to Spain’s 5.3%, the best among

large EMU nations.

BETTER:

The EU commission indices for EU and EMU continue to show substantial

progress. The EU index rose to 75.0 from 71.1 while the EU index rose

to 76.0 from 73.2. The better showing in the EMU rise implies a better

rise in the month by non EMU members of EU. On a mo/mo basis the UK

index did rise sharply by 7.3% compared to Spain’s 5.3%, the best among

large EMU nations.

…but still low: Overall the EU and EMU indices are standing the bottom

26% to 21% of their respective ranges. That is still a very low

reading. But the UK has bounced some 31% from its lowest level on this

overall index and Italy has risen by 25%. The least rebound by a major

EU/EMU economy is the 11.9% rises from its low reading posted by

Germany. Germany also has the lowest ranked sentiment index among large

EU/EMU economies (even though it is third highest by raw score).

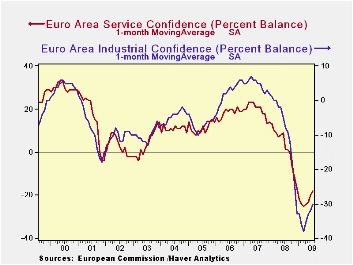

INDUSTRY: EU industry readings are only in the 19th percentile of their range like services. But unfortunately the worst reading on its components are from the selling prices expectation that is in the bottom 7% of its historic range and from orders that are in the bottom 3% of their range (both overall orders and export orders). The production trend is in the 23rd percentile of its range and production expectations are in the 35th percentile or their range - despite the weaker reading in orders. Employment is a sort of neutral 17.8 percentile reading which is the same as for EMU industry confidence overall. So we can’t say for industry that the problem is jobs, it’s just demand.

SERVICE: Services Confidence in EMU stands at it 12.1% percentile lower than for EU overall (19.0%). The weakest reading for services is from current employment which is as low a reading as it ever has seen. Current demand is the next lowest in the bottom 10 percentile of its range. The business climate in services ranks in the 12th percentile overall. Expected demand and expected employment are more upbeat but still in only the 15th percentile of their respective ranges. Despite some monthly improvement employment in this sector is weak and expectations while improving are still very weak. The weakest service sector by the relative measure of the position of the index in its range is France followed closely by Spain; the strongest is the UK.

RETAILING: Retailing ranks in the 28th percentile of its range in EMU, making it relatively less strong than in EU (35th percentile). The present situation is rated as in the 26th percentile; the expected business situation is at a higher raw reading but a lower position in its range at the 23rd range percentile. Employment expectations are a weak 8% reading. The Italy has the highest retail range reading in the 46th range percentile compared to the UK in the 42nd percentile while Spain is at a 28 percentile reading, worst reading for a large EMU country.

CONSUMER CONFIDENCE: Consumer confidence ranks about the same as the retailing reading, in the 29th percentile of its EMU range (below the 32.4 percentile for EU). Spain and Italy have the highest relative consumer rankings at or above a 50 percentile range reading; the UK reading is at the 42nd percentile. Germany stands the lowest among large EMU nations at the 16th percentile. EU consumers rate the past 12-months as in the bottom 5% of all readings historically. While the next 12-months reading posted a much, much higher 48th percentile reading.

SUMMING UP: The consumer confidence results

epitomize the EU/EMU results. Current conditions have improved from

their worst. Yet the quantitative measures that look forward are not

yet very strong. Still expectations for the future are advancing

strongly in Europe. There seems to be a much more ‘hard to pin down’

blanket optimism about the future that is in existence.

| EU Sectors and Country level Overall Sentiment | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| EU | Jul-09 | Jun-09 | May-09 | Apr-09 | Percentile | Rank | Max | Min | Range | Mean | By Queue rank% | R-SQ w/Overall |

| Overall | 75 | 71.1 | 67.9 | 64 | 26.3 | 242 | 116 | 60 | 56 | 100 | 3.6% | 1.00 |

| Industrial | -30 | -33 | -34 | -36 | 19.6 | 244 | 7 | -39 | 46 | -7 | 2.8% | 0.90 |

| Consumer Confid | -21 | -23 | -26 | -28 | 32.4 | 224 | 2 | -32 | 34 | -11 | 10.8% | 0.86 |

| Retail | -14 | -17 | -17 | -21 | 35.5 | 232 | 6 | -25 | 31 | -5 | 7.6% | 0.66 |

| Construction | -37 | -37 | -39 | -38 | 10.9 | 232 | 4 | -42 | 46 | -16 | 7.6% | 0.47 |

| Services | -19 | -23 | -26 | -30 | 19.0 | 242 | 32 | -31 | 63 | 11 | 3.6% | 0.75 |

| % m/m | Jul-09 | Based on Level | Level | |||||||||

| EMU | 3.8% | 4.3% | 4.3% | 76.0 | 21.7 | 236 | 117 | 65 | 53 | 100 | 6.0% | 0.95 |

| Germany | 4.1% | 4.3% | 1.5% | 80.8 | 17.6 | 235 | 121 | 72 | 49 | 100 | 6.4% | 0.70 |

| France | 0.4% | 4.4% | 3.9% | 81.2 | 19.8 | 236 | 119 | 72 | 47 | 100 | 6.0% | 0.84 |

| Italy | 4.4% | 1.4% | 7.3% | 83.7 | 30.1 | 228 | 122 | 67 | 55 | 100 | 9.2% | 0.83 |

| Spain | 5.2% | 2.0% | 2.1% | 79.0 | 24.7 | 230 | 117 | 67 | 50 | 100 | 8.4% | 0.73 |

| Memo:UK | 7.3% | 4.1% | 7.8% | 73.8 | 24.5 | 242 | 128 | 56 | 72 | 100 | 3.6% | 0.59 |

| Since April 1988 | 251 | -Count | Services: | 251 | -Count | |||||||

| Sentiment is an index, sector readings are net balance diffusion measures | ||||||||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief