Global| May 21 2015

Global| May 21 2015EMU Private Sector Weakens Risks Linger

Summary

The EMU PMI gauge from Markit fell to 53.4 in May from 53.9 in April, confounding expectations that Europe's recovery would take root and strengthen. Despite the weak euro exchange rate and ongoing and soon-to be-stepped up QE by the [...]

The EMU PMI gauge from Markit fell to 53.4 in May from 53.9 in April, confounding expectations that Europe's recovery would take root and strengthen. Despite the weak euro exchange rate and ongoing and soon-to be-stepped up QE by the ECB, the EMU recovery is still on shaky ground.

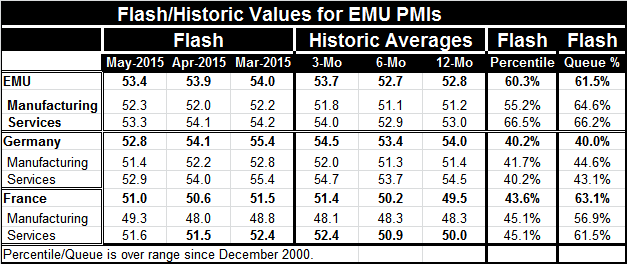

The EMU PMI gauge from Markit fell to 53.4 in May from 53.9 in April, confounding expectations that Europe's recovery would take root and strengthen. Despite the weak euro exchange rate and ongoing and soon-to be-stepped up QE by the ECB, the EMU recovery is still on shaky ground.

As of May, the overall EMU gauge sits only in its 61st queue percentile. That means it has been higher about 39% of the time and lower 61% of the time. That is a positive balance but not an impressive one.

EMU: weakness in balance: The EMU manufacturing gauge rose to 52.3 in May from 52 in April. The EMU services gauge backtracked to 53.3 from 54.1. While the services queue standing is higher than the counterpart standing for manufacturing, the two gauges' standings are now quite close, positioned in their respective mid-60th percentiles. Initially (see graph) services shot up and helped to pull the private sector gauge higher, but recently the services gauge has been weakening and now it is manufacturing with the steadier rise, albeit at an extremely slow pace. Europe's recovery is now more balanced but still quite weak.

Germany and France: one better, one worse: We get early sector data only for member countries Germany and France. Germany's raw private score is higher than that for France, but France has the higher queue standing. What this means is that relatively more businesses are expanding in Germany than in France. But Germany is used to this sort of strength. When we compare current German performance to the past, we find that it is lacking. French performance is relatively stronger than its past. The raw PMI data are absolute measures of strength while the queue percentile standings are relative gauges. Both have their uses. What we see is that Germany is not doing well when evaluated by its past performance and only sits in the 40th percentile of its queue standing. But France, while only at a diffusion score of 51, has a queue standing in the 63rd percentile. While France is weaker than Germany, its performance relative to history is superior.

Balanced growth in Germany but weakening: When we drill down to the sectors we find both German manufacturing and services stepped back in May; the services sector lost 1.1 points while manufacturing lost 0.8 points. The queue standings for manufacturing and services in Germany are now quite similar.

France: still led by services but helped this month by manufacturing: For France, manufacturing continues to decline in absolute terms, but its index made the greater gain in May rising by 1.3 points while services gained only 0.1 points. The French services sector sits in its 61st percentile compared to manufacturing in its 56th percentile. The services sector in France still exerts the greater pull.

The plight of EMU and Greece: While the ECB is stepping up the pace for QE, at least near term, and the euro exchange rate remains weak, the EMU continues to show uneven growth. Regional disparities are an added problem with Greece as an extreme example of the problems that divergence can bring. Greece is fast approaching its cross roads and the rhetoric is not yet reassuring. Greece continues to support this notion of `redlines,' representing cuts it will not make. The EU continues to want more from Greece, but Greece promises less. Recent commentary by German Finance Minister Wolfgang Schauble continues to assert that he thinks Greece may yet choose to default. The Germans have always had a hard line on this, but it is now clear that Greece's unilateral demand for more slack combined with its asserting that it would not do somethings to which is previously had agreed has set the EU's teeth on edge. Nothing has been done to smooth over this disagreement. Greece did not approach the EU carefully; it approached aggressively, demanding changes as if they were a right; Greece's new government, once emboldened by a strong election victory, has been backtracking ever since. The poisoned atmosphere of the Greece-EU talks has made it difficult to recoup to have reasonable discussions. According to Schauble, by stepping away from austerity at the turnoff the year, Greece has lost all credibility with Europe. There is not much time left to bridge this gap.

End game/circle game: For the moment, the EMU region is slowing. It's not for lack of effort from the ECB. And yet there is further risk possible depending on how talks with Greece work out. A failure to find a way to funnel new monies to Greece would certainly have bad repercussions for the EMU nations as well as for Greece itself. Still, Greece must earn any slack it gets or an element of `moral hazard' would be injected in the process. Whatever the deal is with Greece we have not heard the last of it since its debt load is still unsustainable and THAT is not even on the table.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief