Global| Apr 04 2016

Global| Apr 04 2016EMU PPI Is Very Broadly Weaker

Summary

Deflation in PPI prices is very widespread with few exceptions. The pace is getting more deeply into negative territory across the original 11 EMU member countries. Prices are falling period-to-period in all 44 of the country level [...]

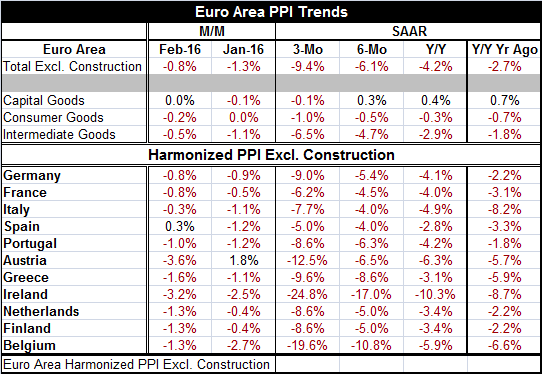

Deflation in PPI prices is very widespread with few exceptions. The pace is getting more deeply into negative territory across the original 11 EMU member countries. Prices are falling period-to-period in all 44 of the country level horizons from three-month to six-month to 12- month to one year ago. That is impressive consistency. Prices are decelerating in 25 of the 30 comparisons of each countries' pace of inflation with the longer one (i.e., three-month compared to six-month, six-month compared with year-over-year, and year-over-year compared with year-ago). The smallest year-over-year PPI drop is Spain at -2.8%; its pace of decline has stepped up to -5% annualized pace over three months. The biggest year-on-year drop is Ireland at -10.3%; that, too, has stepped up to a -24.8% pace over three months. While the ECB had adopted programs to try to reflate growth and prices, it has been fighting a losing battle over the PPI. The HICP is also showing declines, albeit not as deep as these. Oil and commodity price weakness still are driving price trends globally to the consternation of central banks with inflation targets.

Deflation in PPI prices is very widespread with few exceptions. The pace is getting more deeply into negative territory across the original 11 EMU member countries. Prices are falling period-to-period in all 44 of the country level horizons from three-month to six-month to 12- month to one year ago. That is impressive consistency. Prices are decelerating in 25 of the 30 comparisons of each countries' pace of inflation with the longer one (i.e., three-month compared to six-month, six-month compared with year-over-year, and year-over-year compared with year-ago). The smallest year-over-year PPI drop is Spain at -2.8%; its pace of decline has stepped up to -5% annualized pace over three months. The biggest year-on-year drop is Ireland at -10.3%; that, too, has stepped up to a -24.8% pace over three months. While the ECB had adopted programs to try to reflate growth and prices, it has been fighting a losing battle over the PPI. The HICP is also showing declines, albeit not as deep as these. Oil and commodity price weakness still are driving price trends globally to the consternation of central banks with inflation targets.

The overall EMU PPI shows declines and deceleration for 12-month to six-month to three-month. Its components show clear deceleration progressions, but capital goods prices have resisted, falling until just over the last three-month period. Consumer goods prices (at the PPI level) show declines and deceleration, but it is intermediate goods where energy and commodity prices reside that are pushing the trends much lower with the most vigor.

Today in markets, oil prices on world markets marked a one-month low. Prices had gone through a period of rebound as a greater-OPEC meeting was planned and it was thought that there might be a deal to restrict output between key OPEC and non-OPEC members in mid-April. But Iran has steadfastly refused to join any such deal since it is just coming out from under economic sanctions and trying to rebuild its output and earn foreign exchange. Just last week, the Saudis finally admitted that without Iran on board they would not be part of an output capping scheme. Getting Iran on board has never been in the mix. So markets are finally learning to face the music again. The greater OPEC meeting is still scheduled, but expectations have been scaled back.

Still, all hope is not lost. There is ongoing improvement in the EMU unemployment rate which just ticked down from 10.4% in January to 10.3% in February, its lowest level since August 2011. Despite that, the overall EMU unemployment rate stands in the 58th percentile of its queue of values since early 1992. That result is driven by Germany which still has the lowest unemployment rate it has seen since German reunification. Austria, Italy and Luxembourg still report unemployment rates that have been higher on that timeline less than 10% of the time. While the overall progress for EMU unemployment rates is there and it's relatively widespread in February (7 of 11 of the original EMU members show February unemployment rate drops). Unemployment rates across Europe still largely are elevated. Apart for Germany whose rate is at a cycle low, only Ireland has an unemployment rate below its recent median.

The European `experiment' continues to be under pressure. Today Germany reported a financial surplus for 2015 as its budget situation is pristine while other EMU members have struggled with austerity to meet the now enforceable Maastricht rules. With oil and commodity prices are so weak that prices across EMU are weak. Perhaps one avenue for less downward pressure on commodity prices is the dollar which should see less upward pressure as the Fed has backed well away from its former `four rate hike' guidance. But the problem for the dollar is still relative as the U.S. is doing relatively better than most other countries. That could bring upward pressures back to the dollar after the completion of the trade that reacts to the recent Fed policy shift. The global economy is still weak, oil is still in surplus and policy options are still poor. It's like a kindergarten game of chutes and ladders where there are many chutes and false ladders. Policy has had hard time taking a step forward that stick.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief