Global| Nov 05 2013

Global| Nov 05 2013EMU PPI Falls...But Is Gaining Traction

Summary

The EMU PPI has fallen year-over-year for two months in a row. The year-over-year change in the HICP, the EMU-wide gauge for the CPI, is decelerating for three consecutive months. The core-HICP has been in a general deceleration since [...]

The EMU PPI has fallen year-over-year for two months in a row. The year-over-year change in the HICP, the EMU-wide gauge for the CPI, is decelerating for three consecutive months. The core-HICP has been in a general deceleration since September 2011. These observations make it clear that prices do not have much lift in the eurozone. However, the deflation exhibited by the PPI- while disturbing in its own right- does not seem to be the best characterization of the eurozone's inflation situation.

The EMU PPI has fallen year-over-year for two months in a row. The year-over-year change in the HICP, the EMU-wide gauge for the CPI, is decelerating for three consecutive months. The core-HICP has been in a general deceleration since September 2011. These observations make it clear that prices do not have much lift in the eurozone. However, the deflation exhibited by the PPI- while disturbing in its own right- does not seem to be the best characterization of the eurozone's inflation situation.

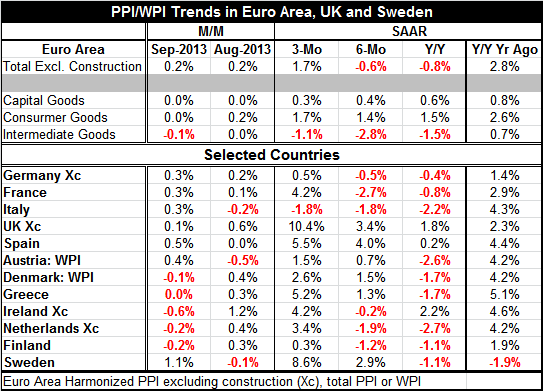

The chart on the components of the PPI makes this clear. In the case of the PPI both consumer goods and capital goods prices are advancing year-over-year albeit at a very slow pace. It is intermediate goods where prices are falling. Capital goods prices are up by 0.6% year-over-year. Consumer goods prices are up by 1.5% year-over-year, but intermediate goods prices are falling by 1.5% year-over year.

Still, the message is that prices are weak. And while countries desire stable prices (a euphemism for low and steady inflation in the real world), the difference between low and desirable inflation and inflation so low that it may be the entree to deflation is really hard to assess. Like beauty, the deflation threat may be in the eye of the beholder.

During a time when growth is still low, when private debt levels are high, when nations are still constricted by budgets that are being redressed for past excesses, when unemployment is high and widespread. low inflation is more likely to be feared as being `too-low.' It is not just the number that represents the inflation rate that matters but the context in which it occurs.

In the current situation of EMU there is a broad basis for concluding that inflation is low and that its pace is still abating. But if we look at the trends for the PPI within the current year we see an opposite development. Producer prices are falling by 0.8% at an annual rate over 12-months, but over six months they falling at a lesser pace of 0.6%, and over three months the pace is a positive 1.7%. Producer prices have their own local dynamic in which they are actually doing somewhat better. However, when we look at the components of the PPI, we see that most of the abatement in the trend to lower prices is from intermediate goods. Capital goods price trends are still eroding, and consumer goods price inflation is oscillating, but stable.

On balance we can expect EMU members to view these trends differently since each has a different context by which to evaluate the trend (different local growth metrics!) in addition to the old line differences in how inflation is viewed and historically has been managed at the country level. With the German economy growing better than the rest of EMU and given the deep seated fear of inflation in Germany, the Germans probably view price developments as just fine. Of the 10 EMU countries in the table, Germany is one of the eight with year-over-year prices falling. In Germany prices are falling by less than in the other seven EMU members where prices are falling (Sweden and the UK are not in the common currency area). Austria and the Netherlands are seeing the largest year-over-year drop in producer prices.

The biggest increase in PPI inflation trends from 12-months to three-months comes from Greece, the Netherlands, Spain and France. Germany, while having the smallest deflation among EMU members experiencing year-over-year price drops, also has the smallest increase in inflation on this horizon. Only Germany and Italy have inflation accelerations on this horizon of less than one percentage point.

We can further array the countries in the table to see how their PPI inflation ranks over 3-months versus 12-months. With 12-countries in the table Germany ranks fourth on its 12-month inflation level But its 3-month pace ranks it 10th. In fact only Germany, Ireland and Finland have inflation rate rankings over 12 months that are substantially higher than over 3-months. France and Italy also show some minor relative temperance while Spain's ranking is the same on the two horizons (it is with relatively high inflation, however). Sweden, the Netherlands and Greece show the biggest jump in their respective inflation rankings. These are countries where the negative inflation over 12-months is an anomaly and where inflation is steaming higher already despite what are in some cases relatively large year-over-year declines.

In these metrics we see another element in evaluating inflation. It is not just the pace that matters but its rate of change. In EMU my fear is that temporary and severe austerity pushed inflation down excessively in a few places where it is going to spring back rapidly. Only Germany and Italy do not change their pace of inflation much from 3-months to12-months. On the other hand the UK does not change its pace much either. Its PPI inflation ranks as second over 12-months and first over 3-months. It is also the country in Europe that is experiencing the best pick-up in growth. It is not in the common currency area.

This comparison on inflation levels and rankings and in changes in the pace over 12-months versus 3-months does not provide any results that are carved in stone as to implications for the future. Still, the various rankings tell us things about countries that we already knew and some we did not. Spain's inflation raking is high on both horizons but not as high as in the UK. Greece's inflation turns sharply higher over three-months. On the other hand the encouraging news is that Italy, a high inflation Mediterranean country, does not see its inflation rank jump from 12-months to three-months. But the reason for this may not be such a good one. Italy's inflation over three-months is still negative, the only case of that in this table.

When we look at the intra-year trends country by country, the risk of deflation no longer seems so great. There is no doubt that prices in the eurozone are and have been restrained over the past year. But there also seems to be an uneven rebounding in growth that is creating some uneven inflation performances. Remember that except for Sweden and the UK (the number one and two ranking inflation counties over three months) all these countries are in a zone with the same monetary policy.

It may be that the price restraint we have been seeing is about to become more lax. I would take this development as one that is pro-growth. were it to continue to develop. But I'm not sure it will continue. What I think we are seeing is that some countries are beginning to bounce back from an episode of severe restraint. But I do not think that Spain and Greece will be able to sustain this sort of turnaround. I worry about Italy still showing PPI deflation. I see Germany as the anchor for EMU-and maybe not in a good way. When you are trying to accelerate it's time to pull the anchor in - not drag it.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief