Global| Jul 24 2015

Global| Jul 24 2015EMU PMIs Falter in July: What Else Did You Expect?

Summary

The services sector continues to lead in terms of the value of the PMI in the EMU, Germany and France. And that goes a long way to explaining why Europe's recovery is still so weak with no fire under it. In July 2015, the EMU overall [...]

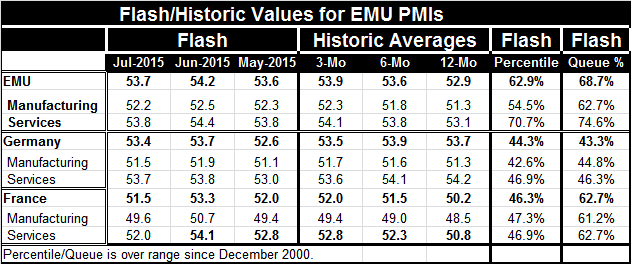

The services sector continues to lead in terms of the value of the PMI in the EMU, Germany and France. And that goes a long way to explaining why Europe's recovery is still so weak with no fire under it. In July 2015, the EMU overall PMI is below its previous three-month average and just a tick above its six-month average. Manufacturing is below its three-month average and slightly above its six-month average. Services are below their three-month average and tied with their six-month average.

The services sector continues to lead in terms of the value of the PMI in the EMU, Germany and France. And that goes a long way to explaining why Europe's recovery is still so weak with no fire under it. In July 2015, the EMU overall PMI is below its previous three-month average and just a tick above its six-month average. Manufacturing is below its three-month average and slightly above its six-month average. Services are below their three-month average and tied with their six-month average.

The EMU manufacturing sector stands in the 62nd percentile of its historic queue of data (it is higher 38% of the time). Services stand in the 74th percentile (higher about one-quarter of the time). The services sector clearly is leading, but there is not much momentum there. Germany and France, the two largest EMU member economies, are lagging the EMU in terms of their respective percentile standings of the manufacturing and services sectors.

The French manufacturing sector has a standing just slightly below that of manufacturing in all of the EMU while the German sector lags the EMU standing by some 18 percentage points - a huge margin. The EMU services sector, in its 74th percentile, compares to Germany's in its 46th percentile and France's in its 62nd percentile. The euro area is being carried by its other members, not by its largest members.

Of course, in terms of the raw diffusion score the German manufacturing sector is stronger than the French sector and the German services sector is stronger than the French sector (and nearly even with the EMU). But the percentile standings compare German sectors with their past not with other members. Germany may still be `doing well' by the depressed standards of the EMU; however, according to its own history, Germany is not doing so well.

Part of this is that Germany and all of the EMU trade a lot in the global economy and that the global economy is weak. Also the EMU countries trade a good deal with one another, too, and the zone itself remains weak. It's sort of a Catch-22. With fiscal austerity as the policy du jour in the EMU, there is not any kick-starting going on. And then there is the nasty problem of Greece, a country trying desperately to be liked that is doing what its peers order it to do. Nevertheless, ultimately, it is a country mired in so little growth and so much official debt, as well as new central bank debt to the ECB, that it is hard to see it climbing out of the morass it is in as long as it is in the euro area- that's not to say that a drachma launch would be a panacea or a picnic. Europe continues to stew over this, too, along with Greece.

The chart of the flash values of the EMU manufacturing and services sector PMIs shows the weakness in momentum. Manufacturing is below its recent cycle high; after a run at higher levels, it has fallen short and is losing momentum again. The services sector is choppy and holding to higher ground but not with much uptrend or conviction.

Europe simply continues to flounder. In other data released today, we see that China's manufacturing sector is weakening. China too is floundering. There is not much momentum in the global economy. The usual growth leaders are struggling and the IMF and the rest of the world economy are holding their breath waiting for a Fed rate hike. Meanwhile, global commodity prices and oil price are sliding. Where is the inflation risk? There is no cost push and no demand pull. Where's the beef? The Fed is well below its inflation target and the economy is still not very robust and yet the Fed is preparing to hike interest rates on mixed U.S. fundamentals. The rest of the world is nearly in shock because of it. Ah, but shocking policies in the U.S. are not alone.

The global economy remains in a tizzy and Europe is one of the main protagonists, but only one of them. China is trying to right an economy that it has micromanaged for far too long and does not seem to understand its new demands. Japan suffers the hangover of its past debt excess and tries to use tax hikes to catch up on a mountain of debt, by constantly smothering emerging growth with a new tax hike. The U.S. obsesses over monetary policy and all the excess reserves it has created and threatens rate hikes. The EU obsesses over debt levels and enforces austerity- a policy that makes things worse and does not always allow things to get better. There are growth villains everywhere. The result is that there are just different versions of contractive policy everywhere, but no one sees it that way. Blood-letting once had its adherents, too. No wonder global growth is so weak. It's by design.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief