Global| Jan 06 2010

Global| Jan 06 2010EMU Orders Take A Step Back

Summary

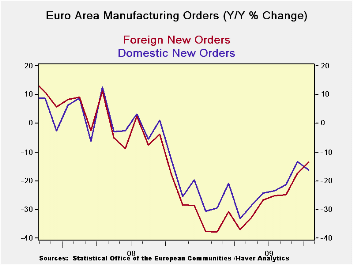

Total orders in the EMU area have fallen m/m in October after six straight months of increasing. The Yr/Yr drop in orders is a still substantial 15.2%. Foreign orders Yr/Yr are off by 13.4% while domestic orders are off by 16.1%. Over [...]

Total orders in the EMU area have fallen m/m in October after six straight months of increasing. The Yr/Yr drop in orders is a still substantial 15.2%. Foreign orders Yr/Yr are off by 13.4% while domestic orders are off by 16.1%. Over three months the Zone’s domestic orders are much weaker, falling at a 15.6% pace compared to foreign orders that are off by just 3.5%. Over six months domestic orders and foreign orders are up, and foreign orders are up on that span at a 20% annual rate.

Country detail shows that Germany leads the EMU parade among large economies. Its orders are still up by 3.5% over three months despite a dip in October. Still all large EU countries are showing a fall off in orders growth over three months compared to six months.

In a December report released today the Markit services indices showed that despite this MFG order weakness in October the services sector in EMU continued to improve though year-end. The EMU services sector diffusion index from Markit moved up to 53.63 in Dec. from 53.04 in Nov. While down on the month France shows the most strength in the service sector among large EMU members

Still, the MFG sector is the cyclical one and orders data, though lagging, show that some softening was occurring in October. The more up-to-date market MFG diffusion surveys show us that MFG progress has continued though year end but has slowed. EMU is being pulled along by demand from outside of the region. Export orders continue to be the driving the EMU expansion. Yet, the EMU currency, the euro, continues to be high-valued, even if off peak, giving reason to wonder how long the e-zone will be able to continue to be pulled ahead by its external sector.

| Euro Area and UK Industrial Orders & Sales Trends | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| Saar except m/m | % m/m | Oct 09 |

Oct 09 |

Oct 09 |

Oct 08 |

Oct 07 |

Qtr-2 Date |

||

| Euro Area Detail | Oct 09 |

Sep 09 |

Aug 09 |

3Mo | 6mo | 12mo | 12mo | 12mo | Saar |

| MFG Sales | 0.3% | -0.8% | 2.0% | 6.0% | 4.8% | -14.2% | -3.0% | 6.4% | 2.4% |

| Intermediate | -7.1% | 6.7% | -3.3% | -15.6% | 8.6% | -16.1% | -3.6% | 8.6% | 9.2% |

| MFG Orders | |||||||||

| Total Orders | -2.2% | 1.7% | 0.5% | -0.4% | 18.3% | -12.2% | -15.2% | 8.1% | -5.8% |

| E-13 Domestic MFG orders | -7.1% | 6.7% | -3.3% | -15.6% | 8.6% | -16.1% | -12.6% | 8.8% | -22.3% |

| E-13 Foreign MFG orders | -2.6% | 7.2% | -5.1% | -3.5% | 20.1% | -13.4% | -17.6% | 14.8% | 1.4% |

| Countries: | Oct 09 |

Sep 09 |

Aug 09 |

3Mo | 6mo | 12mo | 12mo | 12mo | Qtr-2 Date |

| Germany: | -2.6% | 1.5% | 2.5% | 5.5% | 25.0% | -12.6% | -17.3% | 11.3% | -4.7% |

| France: | -9.2% | 4.9% | 2.7% | -8.5% | 5.7% | -9.8% | -16.8% | 5.7% | -28.6% |

| Italy | 0.3% | 5.5% | -8.7% | -12.6% | 5.9% | -15.4% | -14.6% | 5.6% | 5.2% |

| UK(EU) | 11.4% | 1.6% | -11.7% | -0.1% | 45.3% | 1.0% | -9.0% | 4.9% | 57.4% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief