Global| Feb 10 2014

Global| Feb 10 2014EMU Nations' IP Is On Upswing; Is It Really?

Summary

In December we identify nine key members of the European Monetary Union and find that industrial output is falling. The overall euro area measure is not yet available. In December we find four output declines among these nine [...]

In December we identify nine key members of the European Monetary Union and find that industrial output is falling. The overall euro area measure is not yet available.

In December we identify nine key members of the European Monetary Union and find that industrial output is falling. The overall euro area measure is not yet available.

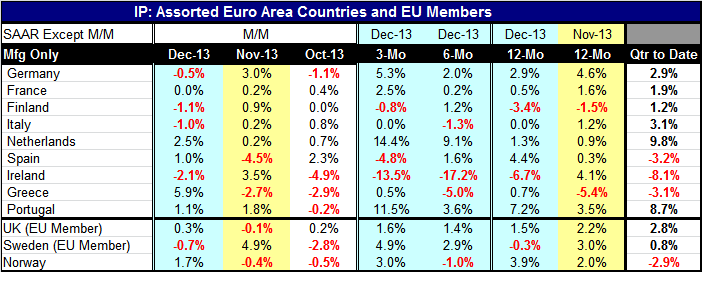

In December we find four output declines among these nine countries, only two declines in November and four declines in October. The gainers are consistently outnumbering the losers over various horizons. Over three months there are only three of nine net declines, over six months, again three of nine show declines, while year-over-year only two EMU members showed declines. And that's the same as it was in November.

On balance the euro area is showing that its members are improving, not just the euro zone aggregate. The clear exception is Ireland with industrial output lower at a 6.7% pace over 12 months and dropping at an accelerated pace of 17% over six months and still-ensnared by a negative 13% growth rate over three months. Finland shows declined over three months and a year-over-year decline of 3.4% with a modest 1.2% rate of increase over six months sandwiched in between. Finland's economy is waffling while Italy shows flat performance over three months, flat performance over 12 months and has output declining at a 13% annual rate over six months. Greece is finally showing some improvement but it's up only 0.7% year-over-year, growing at a 0.5% annual rate over three months and is still down by that 5% at an annual rate over six months. Conditions in the euro zone remain irregular.

Europeans not in the EMU single currency area are performing about same as the countries in EMU right now. The UK shows a single drop in industrial production in November. Sweden posts declines in December and October with a large gain sandwiched in between. Norway shows two straight months of declines but with December rising by 1.7%. Still, the non-EMU currency members demonstrate growth for the most part. Norway is the exception where output is declining at a 2.9% annual rate in the fourth quarter. Sweden's industrial output is increasing at the 0.8% annual rate in the quarter with the UK up at a solid 2.8% annual rate.

Among the monetary union members, three showed declines in output in the fourth quarter. They are led by Ireland falling at 8.1% annual rate followed by Spain at a 3.2% annual rate drop and Greece at a 3.1% annual rate drop. Several EMU members are quite strong in the quarter: the Netherlands posted 9.8% annual rate increase and Portugal posted an 8.7% annual rate increase. Italy's output advances at a 3.1% annual rate in the fourth quarter; Germany's is 2.9%. After that there are increases at a 1.9% annual rate in France and at a 1.2% annual rate in Finland.

The data are overwhelmingly positive; the trends are overwhelmingly improving. But the strength remains underwhelming. In France, for example, the Bank of France just cut its guidance for growth. The BoF now expects 0.2% growth in the first quarter, down from its previous estimate of 0.5%.

EMU trends still have pluses and minuses. The Latvian growth rate in the fourth quarter slowed. Portugal, however, is logging trade progress in posting solid export growth amid tempered import growth. Norway's inflation rate is creeping up.

Halfway around the world, Japan's economy watchers index, which is a gauge of its services sector, backtracked to 54.7 in January from 55.7 in December. This is a diffusion gauge. Japan posted its largest current account deficit in December. Imports in Japan soared; they are augmented by the imports of energy products. Japan's long-held strategy of using a nuclear power has been going to a shutdown phase after its shocking experience with the tsunami and the nuclear reactors in Fukushima. Meanwhile, the People's Bank of China is promising all sorts of support to its beleaguered economy that continues to undershoot expectations.

The reading in the Markit survey of emerging markets shows some backtracking for the world's developing economies that are still having a hard time getting growth in gear. Their collective PMI reading fell to 51.4 from 51.6. These are diffusion indices, too, which still point to growth (with the breakeven mark at a level of 50), but clearly growth in the emerging economies is not doing too much better than `unchanged.'

The European industrial production report and other data released today are no reason for pessimism, but they are reasons for realism. While there are continuing problems with growth in Europe and scattered disturbances among global developing-economy markets, much of this has to do with changes in expectations. Some of it has to do with countries that had been walking on thin ice for a while and then finally fell through. There is an angle through which you can blame the Federal Reserve and its tapering operation. Tapering- especially its step up- came as a shock to some, especially from the impact on market rates. You can blame Fed communication strategies that continue to seem to promise more than the Fed actually intends to deliver.

Since Fed policies are conditional - upon as yet unknown data - it is hard to know what the Fed's alleged guidance really means. While the Fed always makes it known that it is data-dependent, it also tries to push the snake-oil idea that there is guidance, too. For those who find these concepts murky or entangled, I'd say it's like advertising cigarettes. You advertise like crazy even with a big cancer disclaimer on the box. So what's the real message? Smoke them or not?

As an example, the unemployment rate has climbed down to the precipice of its consultation level, as it resides at 6.6% with consultation scheduled at 6.5%. As we have closed in on the 6.5% level, the Fed has been gesticulating wildly to get our attention to let us know that no policy action will be automatically forthcoming when 6.5% is breached. However, markets remain wary that the Fed had picked that 6.5% figure out and that once unemployment in the US is below that metric, policy itself will be on thin ice. Once below 6.5% the conditions necessary for the Fed to pull out or to reverse further stimulus will become more likely to be met or more easily met. So there is a perfectly reasonable and justifiable impact in markets for the expectations for interest rates to shift with ramifications for the flow of credit to the more risky markets based on `Fed guidance'. All this is in a world where many still are struggling.

The world remains a very interrelated place. The continuing problems and slow growth in Europe generate their repercussions as its weakness has some impact on its exchange rate which in turn transmits influences other markets. Stress tests and pending capital requirements of the European Central Bank continue to hang over the heads of the banks in Europe- and therefore overhang growth prospects. The ongoing pledge is to remain a backstop for European growth. Notwithstanding, markets are wary of what the ECB policy does next.

We may be transitioning from the end-game of worrying about the slippage of growth or the onset of deflation to the policy gambit of how to keep balanced growth going once you turn the corner. Still, the differences between these two regimes are quite subtle and there's no telling how or when or what data will shift central bank concerns to the next stage or engage them in backsliding. Markets remain wary.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief