Global| Nov 12 2014

Global| Nov 12 2014EMU IP Springs to Life Even with a Stake in Its Heart

Summary

The chart depicting sector trends in the European Monetary Union for industrial production shows a withering pattern for all three main sectors: consumer goods, intermediate goods and capital goods as of September. However, overall [...]

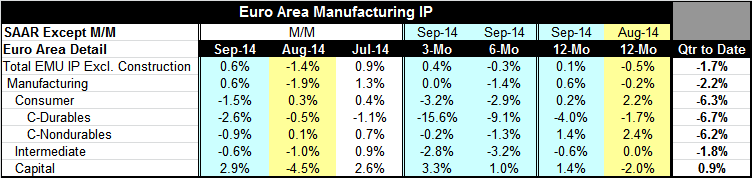

The chart depicting sector trends in the European Monetary Union for industrial production shows a withering pattern for all three main sectors: consumer goods, intermediate goods and capital goods as of September. However, overall industrial production excluding construction rebounded in September to rise by 0.6% after a 1.4% decline in August. It's a strange result with weakness in so many of the underlying member nations, but September was a bit of a rebound month across the community as August had showed declines in nine of 10 key EMU members. Some experienced a rebound in September.

The chart depicting sector trends in the European Monetary Union for industrial production shows a withering pattern for all three main sectors: consumer goods, intermediate goods and capital goods as of September. However, overall industrial production excluding construction rebounded in September to rise by 0.6% after a 1.4% decline in August. It's a strange result with weakness in so many of the underlying member nations, but September was a bit of a rebound month across the community as August had showed declines in nine of 10 key EMU members. Some experienced a rebound in September.

Even with the rebound in September, the pattern for industrial production (ex-construction) is not particularly healthy. Industrial production on this basis is up by 0.1% over 12 months, down at a 0.3% pace over six months and rising over three months at a 0.4% annual rate. Without making too much of the plus- and minus-signs in the small growth rates, it's pretty clear that industrial production has been pretty flat during this whole time span. However, in the quarter to date, which is now for the completed third quarter, EMU industrial production excluding construction is falling at a 1.7% annual rate.

The sectors tell somewhat surprising story in September. The consumer sector is down by 1.5%, output of intermediate goods is down by 0.6% while capital goods output is rising by 2.9%. Despite the depressed state of the global economy and of Europe in general, from 12 months to six months to three months, capital goods output has been expanding. Consumer goods output is declining with increasingly large negative rates; that decline is led by consumer durable goods, while nondurables switch to negative growth rates over three months and six months but do not show an accelerating pattern of decline. Intermediate goods show negative growth rates throughout and while they do not show a continuously accelerating rate of decline, the negative growth rates over three months and six months are both substantial negative numbers. Capital goods alone show consistent increases over 12 months, six months and three months. Oddly, that sector is closer to showing a pattern of acceleration except for deceleration from 12 months to six months. Over the recent three months, capital goods output is growing at a substantial 3.3% annual rate and that's surprising.

The story for industrial production is not so much told by the story of September. September clearly is a month in which there was some respite from severe downward pressure in August. The three-month growth rates and the momentum for growth quite clearly do not paint a positive picture. And if the global economy is going to continue to stay week it will be surprising indeed if capital goods output continues to hold up in such an environment. On the other hand, we've already seen a significant weakening in consumer durable goods output, which is declining at a 15.6% annual rate over three months and is down by 4% year-over-year. Consumer nondurables, which are less volatile, are showing minor negative growth rates over three months and six months. Intermediate goods seem to be taking their trend from the consumer sector, since they have substantial negative growth rates over both three and six months which contrast with the positive and increasing growth rates from the capital goods sector.

Of course, Europe is going to be helped by the continuing weakness in the euro exchange rate; given European Central Bank policy, that trend appears likely to stay in place. On the other hand, competitiveness doesn't help much if global demand is weak. And global demand is weak.

Moreover, there is now news of some reintroduction of military conflict in Ukraine in the wake of Russia having resupplied the rebel regions within Ukraine (just in time for Veterans Day). Heightened tensions and increased military action in the area are not going to help Europe to recover. However, in the recent summit, the Europeans and the Western alliance in general did not step up sanctions against Russia. On the other hand, it's becoming clearer that the existing sanctions are taking a significant toll despite Russia's attempt to pretend as though that's not the case.

The international energy agency today may have surprised a lot of people with its warning about the scarcity of oil supplies as it noted that while there are new supplies of energy coming on stream from activities such as fracking there continue to be hostilities in the Middle East and much of the world's oil production occurs in the region that is still under intense military threats of one sort or another. And we are yet to be certain that Russia is going to stand by its arrangements to supply Europe with energy on a timely basis or Ukraine, for that matter. Russia has not been good on telling the truth so we need to be skeptical about assessing its promises.

There is substantial evidence that economic conditions have slowed somewhat in Japan. The stepup in activity by the Bank of Japan is still to rent to have mush impact. There's evidence that the U.K. has backed off from its previously strong growth rates although the country clearly is still growing. Europe continues to struggle as you can see from the industrial production report; we continue to get plus and minus months when we look at industrial output.

In the U.S., while job growth seems to have steadied, the ongoing slippage in oil prices could become a problem for its nascent energy sector. The rising dollar will take something out of the export sector and also increase import penetration in an economy where the consumer has continued to struggle. However, falling oil prices have two effects: (1) the negative effect on production which in the U.S. is probably the smaller one, and (2) the positive effect on consumption which will be the dominant one and that is somewhat reassuring. However, that only takes us through the period of falling oil prices and it's too soon to tell whether the multiplier effect from weak oil prices could actually jumpstart a faster growth rate in the U.S.

With Republicans gaining an upper hand in the Senate, it's not clear exactly how the political tradeoffs will work out in U.S. politics. With the initial comments from the Republican leadership being more hostile than conciliatory, we should not depend too much on an improved political background.

In summary, there are question marks in every country around the world including China. Equity markets don't so much reflect the risk because the bond yields so low that the equity market is still the best game in town. Do not consider them harbingers. Investors still are concerned about earnings and with growth slowing everywhere, the environment is not supportive. We will continue to make our assessments day by day noting that right now: (1) economic momentum globally is generally negative while (2) dropping oil prices and (3) significant exchange rate changes provided varying incentives depending on the market, (4) we are going to have to watch to see how those incentives change and (5) how economic conditions interact with the changing political and geopolitical landscape which has a considerable bit of flux in a number of countries at the local level as well as at the overarching geopolitical level.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief