Global| Jan 13 2021

Global| Jan 13 2021EMU IP Makes Second Strong Monthly Gain in a Row; Enjoy It While You Can...

Summary

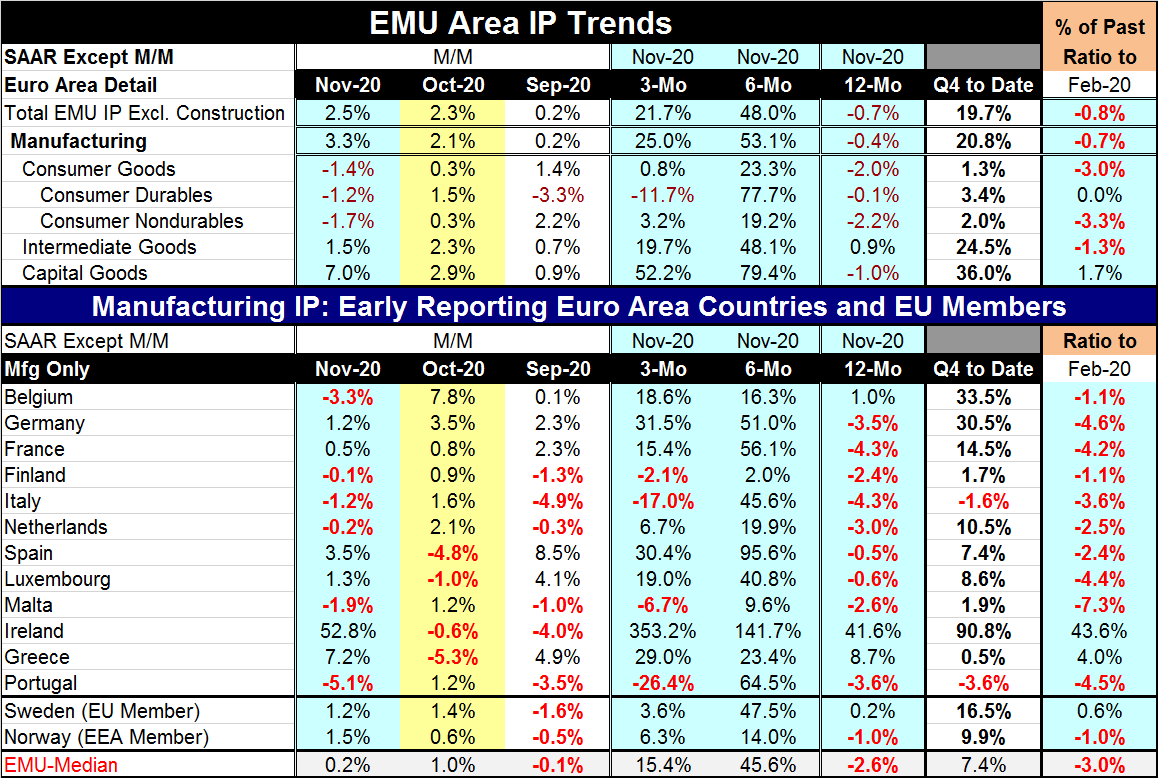

EMU industrial production rose by 2.5% in November, accelerating slightly from the 2.3% gain in October. Both months are a considerable step-up from the 0.2% gain in September. The past two-month gains put IP on a path to rise [...]

EMU industrial production rose by 2.5% in November, accelerating slightly from the 2.3% gain in October. Both months are a considerable step-up from the 0.2% gain in September. The past two-month gains put IP on a path to rise strongly in Q4. The QTD (quarter-to-date) result for Q4 shows growth surging at a 19.7% annualized rate and at a pace of 20.8% for manufacturing. These are impressive results. Still, today France with output rising at a 14.5% annualized rate in Q4-to-date reported out a drop in Q4 GDP of 4%.

EMU industrial production rose by 2.5% in November, accelerating slightly from the 2.3% gain in October. Both months are a considerable step-up from the 0.2% gain in September. The past two-month gains put IP on a path to rise strongly in Q4. The QTD (quarter-to-date) result for Q4 shows growth surging at a 19.7% annualized rate and at a pace of 20.8% for manufacturing. These are impressive results. Still, today France with output rising at a 14.5% annualized rate in Q4-to-date reported out a drop in Q4 GDP of 4%.

In November consumer output contracted in the euro area, falling by 1.4%. Output gains were made on the back of a 1.5% rise in intermediate goods output and a 7.0% surge in capital goods output. Capital goods output is rising at a 36% annualized pace in the four quarter on a QTD basis.

Strong trends

Sequential growth rates tell the same story. Consumer goods output is only creeping ahead over three months after rising strongly over six months. Consumer durable goods output is falling over the recent three months after surging over six months. Intermediate goods and capital goods show very strong growth over three months; still, that is a slowdown from their even stronger six-month growth rates. All manufacturing components show output declines over 12 months except intermediate goods.

Growth by EMU members

Country level data for 12-EMU members now show manufacturing sector output declines in six EMU member countries in November compared to gains in the other six. Output increased in three of the four largest economics with a decline in Italy being the exception. This compares to only four countries logging declines in October and six posting declines in September.

Over three months, however, output increased in all but four members (Finland, Italy, Malta and Portugal). All EMU members showed manufacturing output gains over six months and nine showed declines over 12 months. The countries with output gains over 12 months are Belgium, Ireland and Greece. Ireland, of course, has posted a highly unusual 52.8% increase in output (month-to-month) in November helping to drive that result. Irish officials chalk the gain up to revisions in seasonal adjustment factors in the wake of Covid-19, but that is an unsatisfying explanation. Correcting 'bad' seasonal factors should bring output increases back into alignment with trend not thrust them out to show historically enormous rates of increase. Ireland, that has long reported volatile IP data, remains a question mark.

Comparisons to pre-Covid-19

Looking at output gains since February, just before the Covid-19 disruptions began across Europe, only two of the 12 EMU members show output higher than their respective February levels as of November. The two exceptions are Ireland and Greece. For most of the EMU, output continues to lag its pre-Covid-19 level showing not just that output has not gained back what it lost but underlining that there has been no net growth over the period. The largest EMU economics seem to have suffered the worst declines (Germany, France, Italy and Spain average a decline of 3.7% compared to February), but Malta has the largest shortfall from February (-7.3%) and Luxembourg and Portugal also had large shortfalls.

The virus still lurks

However, the virus was gaining ground during this time and December may show a bigger impact from the virus- certainly January will. In any event, manufacturing weathers the storm with Covid-19 better than the services sector and the PMI data underline this. But if services are disrupted enough, there will be a blow-back impact on manufacturing as well. In 'real time' in January 2021, a period several months in the statistical future of this report, the virus is spreading even more. It is creating havoc in the U.K. China has shuttered 11 million people to contain the spread and has just announced some broader lockdowns as well. Japan has imposed and may enlarge its area for the state of emergency it has declared for Tokyo. Despite back-to-back months of strong data, there is still a reckoning ahead. And while the vaccine is being deployed the virus, a new, faster-spreading variant, seems to be one-step ahead of the inoculations for now. We expect the vaccines to catch up, but for now the spread is on.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief