Global| Jan 11 2018

Global| Jan 11 2018EMU IP Gains on a Strong Capital Goods Sector

Summary

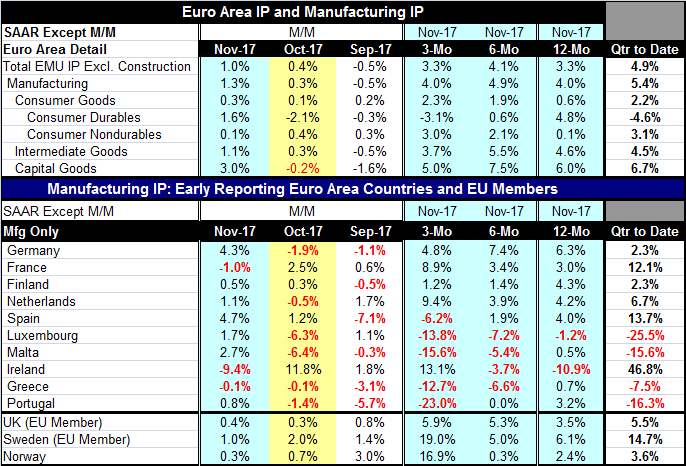

Industrial output rose smartly in the EMU, gaining 1% in November after a 0.4% increase in October and a 0.5% decrease in September. Sequential growth rates for overall and manufacturing output show variation but also reveal [...]

Industrial output rose smartly in the EMU, gaining 1% in November after a 0.4% increase in October and a 0.5% decrease in September. Sequential growth rates for overall and manufacturing output show variation but also reveal essentially flat trends, with three-month growth also at the same pace as 12-month growth.

Industrial output rose smartly in the EMU, gaining 1% in November after a 0.4% increase in October and a 0.5% decrease in September. Sequential growth rates for overall and manufacturing output show variation but also reveal essentially flat trends, with three-month growth also at the same pace as 12-month growth.

IP by Sector

In terms of sequential growth rates across the main sectors (consumer goods, intermediate goods and capital goods), only consumer goods shows ongoing acceleration in output trends. But consumer goods output also has the weakest 12-month gain at 0.6%. Capital goods have growth rates for output of 5% or better on all horizons so there is sustained strength but not ongoing acceleration. Intermediate goods output also shows sustained strength on slightly weaker growth rates than those for capital goods, but still solid and strong growth rates.

Manufacturing IP by Country

Of the 10 early reporters of manufacturing output among the earliest EMU members, only three report IP declines in November. Those three are France, Ireland and Greece. Greece shows three consecutive months of declining output. Germany, Malta and Portugal each reverse a two-month slide in output with a gain in November.

Sequentially, only Luxembourg has declines over all horizons (three-month, six-month and 12-month). But, Spain has a decline over three months that is part of a decelerating pattern of growth. Malta has declines over three months and six months that are part of pattern of decelerating growth. Greece has the same trend conditions as Malta. Portugal has a sizeable drop in output over three months that is part of a decelerating pattern, like Spain. That makes five countries on a decelerating trend.

On the upside, France shows a pattern of accelerating IP growth despite its drop in output in November. Ireland, despite a huge drop of 9.4% in November, shows an accelerating trend in output from 12 months to six months to three months on what have been some wild monthly oscillations. Apart from EMU members, only the U.K. shows steady output acceleration although both Sweden and Norway show large gains in growth over three months after a fairly steady performance over six months and 12 months.

IP Gains Overall

On the whole, the IP data do not strongly signal any sort of rebound or acceleration. The sector chart shows the year-on-year growth rates have two sectors strong and one having a weakening trend (consumer goods). However, within the year, 12 months of data show that the consumer sector is actually digging itself out to stronger growth. Still, IP data simply do not show the ebullience of PMI data.

GDP Growth and Prospects

Today Germany reported its strongest pace of GDP growth in eight years. Impressive as that sounds, it was only a growth rate of 2.2%. France also reported a pick-up in quarterly growth to 0.6% from 0.5%. That's more in the 2.5% range. Italian retail sales 'spurted' by 1.1% but only after sales had fallen by 1% the previous month. While enthusiasm for Europe has been growing, there also is a need to temper it. The ceiling for growth in Europe is still pretty low. It's good to get growth rates with a 2% 'handle' instead of a 1% 'handle,' but that is not going to drive global growth very far or very hard. Some step up in optimism is warranted. But some introspection about the future is still required.

The Path for Central Bank Policy

Central bankers may have to be more careful than they realize to keep 'normal' growth rates in gear. Remember that we are setting these growth rates as interest rates have languished at low levels. It is still hard to say how much a rise in rates will set back growth. The future is not predetermined. It is a creature of policy and it influences policy and will be itself influenced by policy. We are now progressing into a more interesting part of the business cycle where we are not walking downhill or uphill any more so progress is not clearly being persistently aided or impeded. Instead, it's more like walking on ice. Some think the ice is thick and want to step boldly. Some think it is thin and want to progress with caution. The performance of global stock and bond markets gives us two gauges to watch as central bankers step out on the ice and make their moves. I would counsel caution. Global debt loads would seem to still be impediments to ramped up growth or inflation. Moreover, Asian economies still look to depend on the export-led growth model. Until they are willing to bring new demand to the table (and not just new supply), I think we will continue to look at crimped growth prospects.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief