Global| Mar 12 2014

Global| Mar 12 2014EMU IP Drop Belies Widespread Strength

Summary

Industrial production in the European Monetary Union made a surprising decline in January. Yet, it only ticked down by 0.1% but that does mark two consecutive declines. Looking at manufacturing, we see a rebound of 0.3% in January [...]

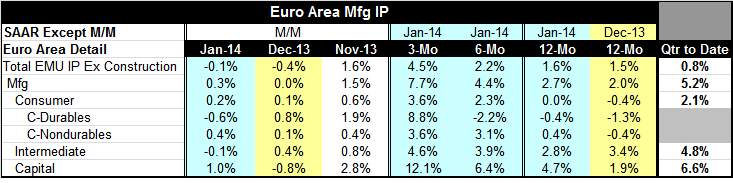

Industrial production in the European Monetary Union made a surprising decline in January. Yet, it only ticked down by 0.1% but that does mark two consecutive declines. Looking at manufacturing, we see a rebound of 0.3% in January after a flat performance in December. Viewed more broadly over longer periods of time, output not only is continuing to expand but to accelerate.

Industrial production in the European Monetary Union made a surprising decline in January. Yet, it only ticked down by 0.1% but that does mark two consecutive declines. Looking at manufacturing, we see a rebound of 0.3% in January after a flat performance in December. Viewed more broadly over longer periods of time, output not only is continuing to expand but to accelerate.

The setback to production in January is due to weakness in the output of energy goods. Overall trends show substantial strength in output and continuing strength and resilience in manufacturing.

Manufacturing output rose by 0.3% in January with consumer goods up by 0.2%. Intermediate goods output fell by 0.1% while capital goods output rose by a strong 1% on the month.

Looking at manufacturing more broadly, we see that manufacturing is expanding by 2.7% over 12 months, at a 4.4% pace over six months and at a 7.7% pace over three months. These are strong and accelerating rates of growth. Despite the two months setback in overall industrial production, manufacturing appears to be not just unaffected but oblivious.

Turning to the sectors, we see that consumer goods output has been flat over 12 months, is expanding at a 2.3% annual rate over six months and is up to a 3.6% pace over the most recent three months. Intermediate goods output has accelerated from a 2.8% growth rate over 12 months to 3.9% over six months to 4.6% over three months. Capital goods output is rising 4.7% over 12 months and a 6.4% pace over six months and at a 12.1% pace over the most recent three months.

The message from the manufacturing sector is that there's a great deal of strength in manufacturing across all sectors. The headline drop in industrial production of the last two months is aberrant.

This conclusion is further bolstered by the available detail on EMU member countries where 7 of 9 countries show manufacturing output up in the recent month with 5 of 9 up in December and with 6 of 9 up in November. The breadth of output increases clearly favors continued expansion.

If we look at sectors relative to the past cycle peaks, we find manufacturing output is about 97% of its past cycle peak of output. By sectors capital goods is the closest to being at full capacity; it's at 98.7% of its past peak of output. Intermediate goods output stands at 94.4% of its past peak. Consumer goods production is at 96% of its past peak. While there's been a substantial recovery in output from its lows, output is not back to its past cycle peak in any the main sectors.

Viewed by country, only Germany is anywhere close to being near capacity. It's manufacturing output is 99.2% of its past cycle peak. The next best EMU members in terms of the level of output compared to its past peak are the Netherlands and Portugal, each of them at better than 93% of their past cycle peaks. However, there also are countries like Spain that is only at 68% of its past cycle peak and Greece that is only about 70% of its past cycle peak.

On balance, the headline drop in production was somewhat worrisome because it was unexpected. However, the clear thrust in output is for continuing increases for manufacturing across manufacturing sectors and across the countries in the Monetary Union. The headline setback was an anomaly or at least premature. Europe's recovery seems to be gaining pace just as the US pace is tailing off.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.