Global| Jun 13 2019

Global| Jun 13 2019EMU IP Continues to Erode

Summary

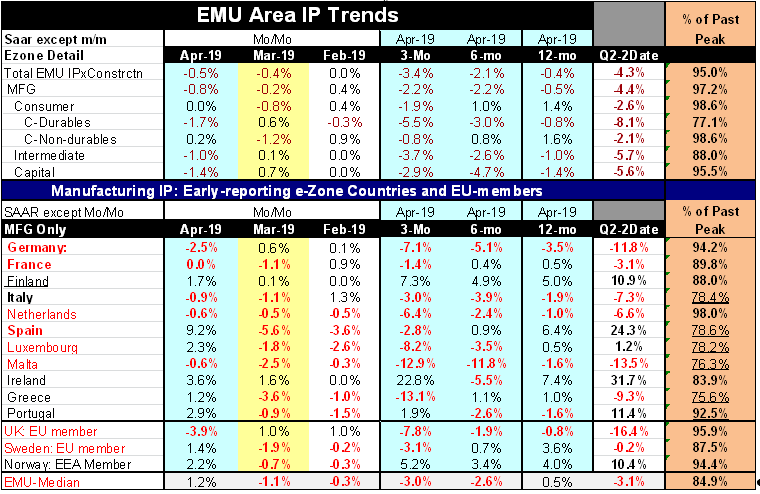

Sectors show some mixed consolidation after a long downward slide form early 2018. Weakness: In EMU Industrial production (IP) excluding construction (the headline series) has fallen for two months in a row and has not risen in three- [...]

Weakness: In EMU Industrial production (IP) excluding construction (the headline series) has fallen for two months in a row and has not risen in three-months. Month-to-month change in IP have been negative or flat in seven of the last eight months. That is quite a legacy of weakness. Manufacturing has seen two month-to-month increases in the last eight months against six declines.

EMU production clearly is weak.

Progressive weakness by sector There is sequential or progressive weakness from 12-months to 6-months to 3-months for the headline series, for manufacturing, for consumer goods overall, for consumer goods durables, for consumer goods nondurables and for intermediate goods. The sole exception is capital goods that in any event show declines on all horizons and show a deeper decline over three months (annualized) that over 12-months.

The manufacturing weakness is deep seated and broadly affects all sectors.

Quarter-to-date weakness The quarter-to-date declines are deep and their annualized drop also exceeds their year-over year drop for all categories. The percent of last peak calculations seem to show the most slack in consumer durables and in intermediate goods.

The manufacturing PMI diffusion index from Markit tracks IP (Yr/Yr percent changes) quite well on the way up and on the way down. While IP plunged and recouped and has weakened again the PMI gauge has continued to show straight-line ongoing weakness for EMU until this last month when it steadied.

Country by country weakness The data in the table by country are colored coded with the red countries in the table’s stub all being IP results showing trends as sequentially deteriorating 12-months to 6-months to 3-month. Among the 14 countries in the table, eight show sequential deterioration in progress. Finland and Norway come close to showing sequential acceleration, but no country really does that. The median for EMU shows sequential deterioration. Over three-months ten of 14 countries in the table log output declines. That compares to eight over six-months and 6 over 12-months. .

While there has been ongoing declines in IP and although weakness is widespread five countries in the table still have output at 90% or better of their past cycle peak. Four more are 84 percent of their past cycle peak or better and the rest of them are no weaker than 25% below their past cycle output peaks. The weak group includes Greece, Malta, Luxembourg, Spain and Italy. The strong group includes Norway, The UK, Portugal, The Netherlands and Germany. Looking at the relation to past peaks by sector consumer durables are the weakest at 77% of their past peak. That is something to watch since durables consumption/output is highly cyclical. However, capital goods output is still strong within 5% of its last cycle peak, despite the recent slowdown

On balance Europe remains in a slowing mode. The PMI data show a more worrisome profile that the IP data by itself. And while the results for the recent 3-months seem quite grim the performance in the most recent month is not despite the decline for IP overall (which is mostly on the back of weakness in Germany).

Europe is still trying to see how it has re-invented itself in the wake of European elections. The UK is selecting a new PM and looking to renegotiate a Brexit deal with a cast that is looking much more friendly at the prospect of a hard Brexit with Mr. Boris Johnson in the lead, in better physical shape, but still without a comb… no wonder the prospect of a disorderly exit does not seem to bother him.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief