Global| Dec 13 2018

Global| Dec 13 2018EMU Inflation Falls Back into Place

Summary

The ECB targets inflation of just under 2%. The ECB claims (without any proof that I am sure of…) that inflation that is below but close to 2% allows the economy to reap maximum benefits. This month the HICP is up at 2% or 1.96% if we [...]

Then What? The Role of Trade...

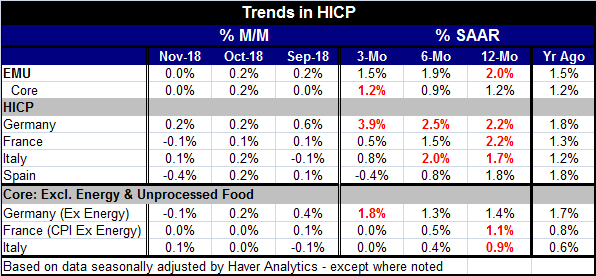

The ECB targets inflation of just under 2%. The ECB claims (without any proof that I am sure of…) that inflation that is below but close to 2% allows the economy to reap maximum benefits. This month the HICP is up at 2% or 1.96% if we split hairs and carry more decimal places. And splitting hairs drops the HICP back down into the ECBs' sweet spot.

The ECB targets inflation of just under 2%. The ECB claims (without any proof that I am sure of…) that inflation that is below but close to 2% allows the economy to reap maximum benefits. This month the HICP is up at 2% or 1.96% if we split hairs and carry more decimal places. And splitting hairs drops the HICP back down into the ECBs' sweet spot.

Headline inflation had been ‘too high' for four months running. Prior to that, from June 2018 through February 2013, it had been constantly ‘too low' much farther below 2% than ‘just a bit.' The core rate on the other hand has been running at a pace below 2% since January 2009. The core (the HICP excluding energy and unprocessed foods) has no official standing. But with the economy having underperformed and with Mario Draghi as the ECB head, the bank has been emphasizing the core gauge over the headline rate especially since oil prices have been gyrating and have been the main reason that headline inflation has come close to or exceeded its mandated profile in its recent oscillations.

Still, the ECB has its stalwarts. There is a important cadre of board members that views inflation as relative to target on the headline gauge month-to-month with no institutional memory of the past.

Germany continues to overshoot the ECB's global gauge of 2% although the German ex-energy rate is still running below 2%. The German headline pace is accelerating from 12-months to six-months to three-months although the ex-energy profile is not as clear cut at that. Of course, German inflation is simply inflation in Germany and has no official policy standing at the ECB.

Bon voyage ECB

Needless to say, a split view on policy continues under the surface at the ECB, with inflation hawks looking to a return of policy to normalcy. The ECB did take that step today by agreeing to end its program of QE. The ECB will end this program in December in line with what it had tentatively agreed to previously. The ECB joins the Fed on is voyage to normalcy.

It does so in an environment in which headline inflation is back in line and has been consistently well contained over the past five years, in an environment with falling global oil prices and at a time when growth in the euro area has been withering.

The ECB has no growth mandate and only has an inflation mandate. With the special QE program ended, the ECB can look ahead to normalizing its functioning and eventually to raising interest rates back to more normal levels...conditions permitting.

Yesterday European industrial production rose after a sharp drop prompting headlines saying that European growth is back on track. I think that assessment is premature.

The Markit indexes for manufacturing and services for the EMU are still weak and withering. Trade conflicts endure and that is a major element of risk to any outlook.

What activity on the trade front means for growth

China's recent grab of a former Canadian diplomat and its action to probe a second Canadian for security violations are ample evidence that China is not and may never be Free Trader simply because it cannot be trusted to separate political from economic matters. For China, everything is political. Free trade works best in an environment with capitalism and freedom… while China is a communist country. China seems to treat its corporate executives as though they are important party members first.

China owns companies. It directs bank lending. It has a national policy to steal and transfer technology. It does not recognize trademarks. It grabbed the South China Sea and thumbed its nose at the World Court when it said essentially ‘give it back.' How does one trade ‘freely' with an entity like that that does not respect the rule of law? China also controls its exchange rate, another clear free trade no-no.

The risk of a trade war remains high. I would judge the probability of emerging from this episode with anything that even mimics free trade as being extremely low. People who thought we were ‘close enough to free trade before' probably think that baseball with 2 strikes and you're out and a walk on three balls is close enough to being real baseball too. In fact, I have no idea what a trade system would like or how it might imitate free trade given all the issues involved in integrating China as ‘trusted' partner is such a process.

Having said that, I will say also I am not sure what that means for the future. China and other Asian counties have co-opted the international trading system to become the low cost suppliers to the world fulfilling demand in the West and achieving the nirvana of export-led growth. They keep costs down in part by controlling their exchanger rates- something that is forbidden if there is real free trade. Of course, free trade is not really ever about having specialist consumer and producer countries. And when that happens, the sustainability of the trading system built on such a shaky base is called into question. No country can run deficits forever. Still, a system like that might endure for a substantial period of time before it blew itself up, especially if the persistent deficit country were rich enough to start. You can compare such a trading system to a hot air balloon with a slow leak. It will keep you up for a while and you may or may not have enough hot air to get to your destination depending on the size of the hole.

For now globally inflation – what little there is- is being stuffed back in the tube by falling oil prices. The Fed continues to shrink its balance sheet and may slow the procession of rates to their historic norms. The ECB is stopping its QE program. The BOE is still in a wait and see mode over Brexit where the odds increasingly are dicey and looking slanted toward a ‘bad' outcome.

While I am one of the few who is ‘happy' that the U.S. is finally pressuring China and others over unfair trade and trying to right unfair trade deals, there is a lot in the arena of international trade and finance that is broken and in dire need for fixing. Little enough of it is on the agenda. Chief among the broken parts is the exchange rate system. There is no surveillance of exchange rates and all too many countries (AKA governments) guide their rates according to some official policy goal. As long as that happens, Free Trade will remain elusive. That means the gains expected from Free Trade will not flow.

China is just too big and still has too many parts of it that are undeveloped to allow it to continue to develop as it has in the past. The cost of lost of jobs in the U.S. and elsewhere has been too high and already has become economically and politically destabilizing in the West. China must become a better consumer nation and must cut its relentless pursuit of domination through trade. Trade is supposed to be mutually beneficial –not warfare. Even the most cursory glimpse of trade patterns show that it is not and has not been that.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief