Global| Sep 11 2014

Global| Sep 11 2014EMU Inflation Creeps Lower

Summary

Inflation in the euro area continues to snake lower. Among the early reporters of inflation data, Spain has the lowest year-over-year inflation at -0.5%, followed by Greece and Italy each at -0.2%. Germany is a high inflation country [...]

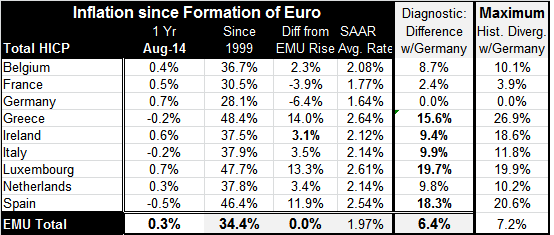

Inflation in the euro area continues to snake lower. Among the early reporters of inflation data, Spain has the lowest year-over-year inflation at -0.5%, followed by Greece and Italy each at -0.2%. Germany is a high inflation country with its year-over-year HICP at 0.7%, the same as Luxembourg. Gone are the days when German inflation is always the lowest. Still, the German price level has risen the least among all members since the European Monetary Union was formed: 28.1%. Now, austerity, and the focus on reining in budget deficits, is causing stringent economic policies to prevail throughout the euro area, crimping both growth and inflation.

Inflation in the euro area continues to snake lower. Among the early reporters of inflation data, Spain has the lowest year-over-year inflation at -0.5%, followed by Greece and Italy each at -0.2%. Germany is a high inflation country with its year-over-year HICP at 0.7%, the same as Luxembourg. Gone are the days when German inflation is always the lowest. Still, the German price level has risen the least among all members since the European Monetary Union was formed: 28.1%. Now, austerity, and the focus on reining in budget deficits, is causing stringent economic policies to prevail throughout the euro area, crimping both growth and inflation.

The chart shows that historically Italy has had the highest inflation rate and Germany, the lowest among the three countries plotted in the chart. But over the past year, German inflation is the highest and Italian inflation has been the lowest.

These shifts indicate some powerful economic forces at work behind the scenes. It's not surprising that with the rest of the euro area pressing inflation lower, growth has been underperforming. We can turn to the table and see why countries have been willing to undertake such draconian anti-inflation policies.

At the far right of this table, we show the maximum divergence between the respective price levels of the countries listed in the stub to the left with Germany, the traditional low inflation country. These measures go back to the beginning of the formation of the euro area. You can see that Greece has had a divergence with Germany of nearly 27%! But since the policy of austerity has been imposed, Greece has reduced the German price advantage to 15.6%. This is the most dramatic change of any country in the table. Spain, which also has had a substantial divergence with Germany- its highest was 20.6% - has reduced its divergence to 18.3%, a much smaller degree of progress, but still significant. You can look up and down the line and compare the progress made in other countries by comparing the last two columns in the table: maximum divergence vs. current divergence.

Because inflation has been more rampant outside of Germany, among countries in the euro area, in the wake of the economic crisis, countries that had lost competitiveness to higher inflation have worked to reduce their competitiveness disadvantage. This is been done largely through a policy of deflation and recession which has been extremely painful. Greece, which has suffered the most pain, has also made the most progress. Overall, Greece is still some 15% behind Germany in terms of competitiveness compared to where it was when it joined the euro area.

These metrics are most important if the EMU countries intend to compete in the same industries. To the extent that they have different advantages, these price differences may not be so important. Greece, for example, is not a manufacturing economy and gains many of its resources from its tourism industry. Still, the main objective for Greece has been to gain control of its fiscal deficit so it can pay its own way. Overall, countries with loose government finances have also been countries with largest inflation problems.

Mario Draghi's policies at the European Central Bank are aimed to increase lending across the euro area. However Europe's banks are weak and must take care where they lend. This stumbling block could greatly undermine Draghi's program.

On balance, inflation data this month tells us that European inflation is still on a downward trajectory at a time when lower inflation has become no virtue. After years of having fought high inflation, it's quite strange to write those words. But that is the circumstance of Europe. As you can see from the table, Germany, a relatively healthy economy, continues to have the highest inflation rate among the early inflation reporters in the euro area. Luxembourg matches it at 0.7%, but Luxembourg is a financial center and price competitiveness is not particularly crucial there. If we measure the ECB's progress by the turning around of inflation's trend, we would have to judge the policy, the rhetoric and the attempt to shift expectations, as not yet effective.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief