Global| Jul 17 2017

Global| Jul 17 2017EMU Inflation As Expected: Flat in June and for How Long?

Summary

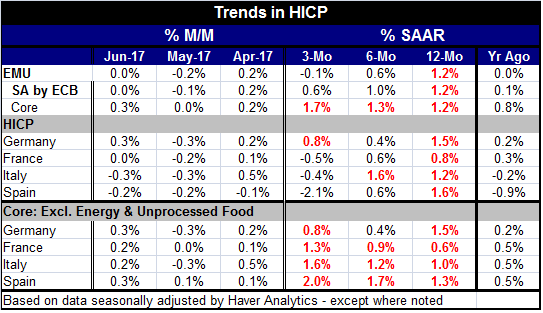

Inflation in the EMU has flared then flagged as the chart demonstrates. Inflation is currently in a cooling mode as oil prices stopped their push up and have actually reversed to show a multi-month period of softness and ongoing [...]

Inflation in the EMU has flared then flagged as the chart demonstrates. Inflation is currently in a cooling mode as oil prices stopped their push up and have actually reversed to show a multi-month period of softness and ongoing weakening.

Inflation in the EMU has flared then flagged as the chart demonstrates. Inflation is currently in a cooling mode as oil prices stopped their push up and have actually reversed to show a multi-month period of softness and ongoing weakening.

Still, core inflation is on a broader accelerating path, rising from a 1.2% gain over 12 months to log a gain at a rate of 1.3% over six months and to step that up to 1.7% over three months. ECB President Mario Draghi is now anticipated to attend the Fed's annual Jackson Hole symposium and to offer remarks suggesting a change in stance to a slightly less accommodate policy ahead. Is that the right course of action?

The core at a 1.7% pace over three months is closing in on the ECBs inflation goal of just less than 2% although its 1.2% 12-month climb, as well as the 1.2% 12-month pace for the headline, the latter of which is the formally targeted variable, both lag behind the ECB objective. And three-month growth rates are simply are too fickle to be the basis for policy although they do contain information. The new element that is present for the core that may be decisive is the rising momentum. Inflation trends in the U.S., for example, have backed off too, but they feature falling inflation momentum for the headline and the core and put the Fed in a tighter box on the question of pursuing a tighter policy - even though the Fed is doing just that, pursing tighter monetary policy. Central banks seem ready to disbelieve what is right in front of their eyes.

The table below features inflation in the original EMU member countries. Only Austria has inflation near 2% with a gain of 1.9%. The ECB target of just under 2% refers to the weighted HICP for all of the EMU. Finland, France Greece and Ireland still show year-on-year inflation less than 1% while the Netherlands and Portugal report inflation at 1%.

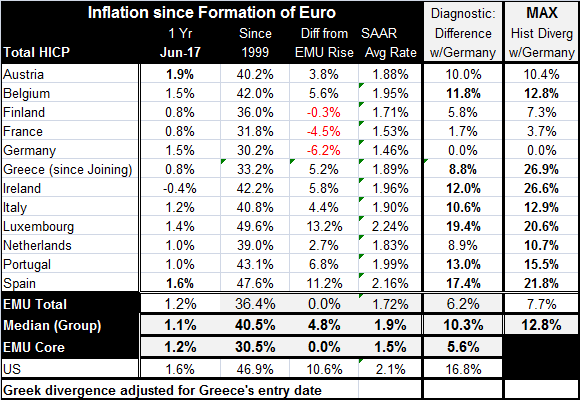

This table focuses on inflation performance among EMU members since the EMU region was formed. It shows that only three countries France, Finland and Germany have kept inflation below the EMU average mark consistently since the EMU was formed. The second to the last column to the right shows the deviation of prices at the national level with Germany, the region's low inflation country since the EMU was formed. The median deviation from Germany is 10.3%. That means that half the countries in the EMU have allowed their price level to rise by 10% more than the German price level has risen since the EMU was formed and that excessive rise represents a loss in competitiveness to Germany around the community. The loss ranges from a small 1.7% loss in France to a substantial 19.4% in Luxembourg and 17.4% in Spain.

While thinking of US inflation performance as having been good over this period, inflation in the U.S. has been only about as good as it has been in Spain, one of the worst inflation transgressors in the EMU. Of course, the U.S. is not stuck in the EMU region and its exchange is free to fluctuate to make up for competitiveness differences when they arise, unlike Spain.

We have come through a period of very low inflation. Previous to this, there had been a boom cycle in which debt accumulation had fueled growth. Now debt is being high in most countries and less of an option. Debt is being controlled and growth is coming mostly from areas that have a high savings rate and low wages. Japan has been grappling with deflation. Central bankers are convinced that the next great risk will be that of inflation again. But what if they are wrong? In fact, inflation has been hard to restart. The slow growth, lack of good jobs and low productivity in the West are a trap of sorts. World trade had been a game of ferreting out domestic demand and using it to boost output and GDP back home, but now there is no domestic demand strength to be found anywhere. The great hide and go seek game of international trade is no longer going to play that game because there is no demand to ferret out. That raises the question of where growth comes from. And it is fair to ask how developing economies will keep up their high rates of growth? If growth and demand do not emerge, how does inflation rise in the West? Are central bankers fighting the last battle? It's a point they are not considering. All central banks are looking for their economies to get rates back to normal with exception of the Bank of Japan that is fighting for is life to restore normalcy instead of assuming it. Is it the only one that sees the true risk?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief