Global| Aug 29 2008

Global| Aug 29 2008EMU Indices Continue to Lose Ground

Summary

This Month - The European Commission’s monthly indices show that the area continued to lose ground as economic sentiment slipped from 88.8 in July to 86.9 in August. All main sector gauges fell in the month save consumer confidence [...]

This Month - The European Commission’s monthly indices show

that the area continued to lose ground as economic sentiment slipped

from 88.8 in July to 86.9 in August. All main sector gauges fell in the

month save consumer confidence which advanced one thin point but

remained negative overall and weak in its historic range.

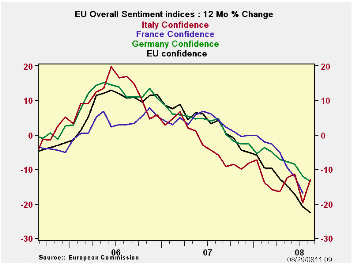

Assessing the levels of the various indicators - The EU

sentiment gauge stands in the 31st percentile of its range in August

2008. The gage for EMU is slightly stronger in its 35.8th percentile.

France did not report on time this month and that often seem to be the

case for France when things are deteriorating. Reporting later does not

make things better. Germany and Italy have overall sentiment gauges

that lie in about the 35th percentile of their respective historic

ranges. Spain is in the bottom 8 percentile of its range. The UK, an EU

member, drags down the average with a heavy weight as its gauge stands

in the bottom 19 percent of its historic range.

Assessing the sectors this month: In August the retail index

fell especially hard, dropping by 4 points. This compares to a three

point drop for the industrial sector. Services backtracked by only one

point, but that sector is the relative weakest in the 13th percentile

of its historic range. Retailing is in the 22nd percentile of its

historic range and consumer confidence with its one-point rise stands

in the 27th percentile of its range. Construction at a deeply negative

-18 is still in the 51st percentile of its historic range while MFG at

a -10 is at the 50th percentile the dead middle of its range.

EMU inflation, the EU Commission survey and more - There is a

lot of concern about inflation in EMU at the moment. The day also saw

the release of the EMU July HICP. That preliminary reading showed

inflation has notched down to 3.8% from 4% - a move in the right

direction but still distant from the 2% ECB ceiling for inflation. In

the EU Commission survey there was some evidence that inflation

expectations were adjusting in a positive direction. For industrial

selling prices, expectations fell by three months to a +17 level and

stand in the 75th percentile of their historic range- still high. For

consumers, expected price trends in the next 12-months broke sharply

lower dropping by 8 points on the month to stand at +22 in the 57th

percentile of their historic range. In construction prices expectations

stood at a +4 down in the month and down sharply from +111 in June but

still held in the 63rd percentile of their range. All in all actual

inflation did edge lower in the month of July and expectations are

moving in the right direction, lower, in August. The ECB can breathe

somewhat of a sigh of relief. The bad inflation news on the day came

form Germany where more first half wage agreements showed signs of

edging over 4%. So it was not a perfect day but it was a good day for

inflation-watchers.

| EU Sectors and Country level Overall Sentiment | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| EU | Aug 08 |

Jul 08 |

Jun 08 |

May 08 |

%tile | Rank | Max | Min | Range | Mean | R-SQ w/Overall |

| Overall | 86.9 | 88.8 | 94.5 | 97.1 | 31.8 | 230 | 116 | 73 | 43 | 101 | 1.00 |

| Industrial | -10 | -7 | -4 | -3 | 50.0 | 156 | 7 | -27 | 34 | -6 | 0.86 |

| Consumer Confidence | -19 | -20 | -17 | -14 | 27.6 | 225 | 2 | -27 | 29 | -10 | 0.83 |

| Retail | -15 | -11 | -5 | -3 | 22.2 | 239 | 6 | -21 | 27 | -5 | 0.49 |

| Construction | -18 | -17 | -14 | -11 | 51.1 | 157 | 5 | -42 | 47 | -15 | 0.42 |

| Services | -1 | 0 | 7 | 6 | 13.2 | 130 | 32 | -6 | 38 | 17 | 0.80 |

| % m/m | Aug 08 |

Based on Level | Level | ||||||||

| EMU | -0.8% | -5.6% | -2.9% | 88.8 | 35.8 | 226 | 117 | 73 | 44 | 101 | 0.93 |

| Germany | -2.7% | -4.1% | -1.5% | 94.7 | 37.9 | 182 | 121 | 79 | 42 | 101 | 0.64 |

| France | N/A | -4.6% | -3.0% | N/A | N/A | N/A | N/A | N/A | N/A | N/A | N/A |

| Italy | 4.8% | -10.1% | -0.1% | 89.5 | 35.7 | 224 | 122 | 71 | 51 | 101 | 0.80 |

| Spain | -4.3% | 1.6% | -7.8% | 71.0 | 8.4 | 243 | 118 | 67 | 51 | 100 | 0.60 |

| Memo:UK | -6.1% | -7.8% | 2.3% | 80.3 | 19.0 | 235 | 130 | 69 | 61 | 101 | 0.42 |

| Since 1990 except Services (Oct 1996) 247 | -Count | Services: | 142 | -Count | |||||||

| Sentiment is an index, sector readings are net balance diffusion measures | |||||||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief