Global| Jun 04 2019

Global| Jun 04 2019EMU HICP Gets Even Weaker As Unemployment Rate Hits New Cycle Low!

Summary

The chart may remind you, as it does me, of the groundhog that looks out and sees his shadow retreating to his burrow for another few weeks of winter weather. Is inflation making another major retreat? Waiting for inflation to [...]

The chart may remind you, as it does me, of the groundhog that looks out and sees his shadow retreating to his burrow for another few weeks of winter weather. Is inflation making another major retreat?

The chart may remind you, as it does me, of the groundhog that looks out and sees his shadow retreating to his burrow for another few weeks of winter weather. Is inflation making another major retreat?

Waiting for inflation to recover… to demonstrate 'mean reversion,' to go 'back to normal' is almost as frustrating as waiting for Godot. However, Samuel Beckett does not sit on the FOMC and regardless of the waiting and the implicit message from the Poisson distribution (that message would be that if you have waited a very long time for something to happen and it has not happened rather than to expect the 'overdue' event to occur shortly, you should make 'other plans' since the event still may not occur for a very long time). Fed members to a man and woman ALL BELIEVE inflation is going to come and they generally expect it sooner rather than later. In Europe it is much the same with some interesting added complications since countries in the monetary union are having different experiences. In Japan, they have waited so long they are trying to 'friend' Godot on the internet. Some in Japan still think inflation can be coaxed, cajoled or jolted back into existence; others think that the BOJ should throw in the towel and accept a lower inflation objective. A least the BOJ has avoided deflation.

Interestingly, inflation is one of the most studied and least understood events in economics. Almost everyone can tell what inflation does; almost no one can tell you what inflation is. It depends on what you mean by the word 'is' as Bill Clinton once said.

An inflation story

In 2015 ironically just before the FOMC proclaimed that it was certain inflation would rise to its 2% target in the medium term and used that as a pretext to begin hiking the Fed funds rate with inflation running well below the Fed's objective, a paper presented at the Kansas City Fed symposium in Jackson Hole, Wyoming in June of that year had proclaimed that no economic model of inflation was robust. The symposium paper concluded that no economic model really worked in all circumstances. The major inflation predictors each had their spheres of influence, but nothing worked universally. Undeterred by that paper, the Fed pressed ahead into the great unknown and into to further policy embarrassment.

Global monetary nothingness

We are seeing the results of this paper from 2015, long forgotten, often ignored, as country after country fails to get inflation going regardless of its beliefs. It's as though central bankers think they have been throwing matches into a puddle of gasoline without even getting a flame or smoke. Still, they are reluctant to continue (pssst…maybe it's a puddle of WATER!). Record low unemployment, as well as 'as much monetary stimulus as the skeptics could stand' (and more than what many wanted!) has had little effect. Monetary stimulus is rampant globally among the major monetary center countries and still no inflation.New lows on unemployment rates and still no inflation. Hmmm...Aliens?

Where's Waldo? Where's fiscal policy?

The fiscal stimulus situation is more complicated to define since globally debt to GDP ratios are high but in many places for that very reason fiscal stimulus has not been used for quite a while. Japans debt-to-GDP has handcuffed Japan for a long time placing a greater burden for results on monetary policy. In the EMU, Germany took the financial crisis as an opportunity to reinvigorate the EU Commission's zeal and set it to its task of enforcing the Maastricht rules so that the aftermath of the global recession and financial meltdown also bought some horrific fiscal austerity to parts of Europe. Italy is still reeling from that, and in fact, that austerity was responsible for shackling Italy's GDP development. Italy's real GDP is below its level of 10 years ago undoubtedly a main reason that Italy's massive debt-to-GDP ratio has not gotten better. Yet, the EU Commission- hilariously (unless you are in Italy, of course) is now going to discipline Italy for the debt ratio excess that evolved from EU Commission-imposed austerity on Italy. You can't make this stuff up.

What inflation 'is'

So everyone knows that inflation is when economy-wide prices are rising. We call the year-over-year gain in our selected price gauge the inflation rate (HICP for the EMU, PCE for the U.S., the Bank of Canada references a bundle of inflation measures, and so on). But it is also well-recognized that rogue elements can push an overall price gauge up and obscure the message about what inflation 'is.' That sentence is a nod to the notion that inflation is not just what inflation 'was' but what it 'will be.' Inflation has this multidimensional time aspect to it. Looking at year-on-year price changes tells more what inflation 'was' than what it 'is.' But we all realize that compounding one month's change to an annualized rate and calling that inflation would be foolish. And then there is matter of what people expect in the future. Economics has come to look more and more on expectations as important. Expectations are important for actions because few economic decisions involve doing things instantaneously. When firms invest in equipment or construct new buildings they are planning for the future and for that they need expectations of what the future will be. Inflation is an important part of that picture. To handle issues of price instability, most countries look at measures excluding food and energy; there are also several versions of a trimmed mean inflation calculation that exclude volatile elements. As you can, see economists are trying to deal with this issue, but it is difficult because inflation essentially is a multidimensional variable.

Setting that aside, there is still trouble in trying to get plain old fashioned year-over-year inflation up. And economists are confused about what to do. Of course, INDIVIDUAL economists are not confused. Every science has its ideologues. But policymakers have a lot of economists among them are wary that they may need to do more as well as that they may have done too much. This dilemma defines them well. Obviously, if 'strong action' is called for, this group will not be doing because of their equivocal mindset.

Europe in May

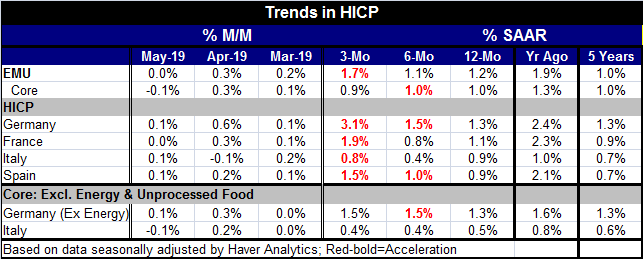

Flowers are blooming and birds are singing, but central bankers are in a state of lament in Europe. This month inflation has fallen to 1.2% EMU-wide and 1.0% for the core rate. And while the discussion about inflation dynamics may make it sound like some meteor hit and shifted all the laws of economics, Europe's data show that this isn't true. Germany, the persistently strongest EMU economy with a record low rate of unemployment, is producing inflation. Year-on-year the German HICP is up by 1.3%; over three months its annual rate of increase is 3.1%. But the ex-energy German pace over 12 months is 1.3% against a compounded three-month core rate of 1.5%. Naturally Germany is about the most inflation hating nation on the planet and it has what seems to be the worst inflation among major money center economies. Even so, German inflation is still tame and undernourished only flaring over three months on the back of oil. Note that over the last five years among the four largest EMU economics, Germany has had the highest rate of inflation while Italy and Spain have had the lowest. This is not your mother's Germany…

Decision time

Policymakers need to figure out what is going on in order to make policy. They can't make policy very well if they are afraid to take one step forward and reluctant to take on step back. But that is where they are. Policy has not identified deflation and low growth or inflation as the greater risk; yet, no one thinks this is the 'sweet spot.' Internationalization and various technology breakthroughs are responsible for the new economy. They are not going away. If the Fed and ECB are wary of keeping rates too low because of financial excesses, they should ask for new macro-prudential powers. But bankers need to figure things out instead of walking evermore on eggshells. Tentative policymaking will only lead to disaster.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief