Global| Oct 31 2017

Global| Oct 31 2017EMU GDP: Settles Into Growth Path

Summary

From the end of 2012, EMU year-on-year real GDP has been gradually accelerating. In Q2 2015, it reached a growth rate of 2.0%. Then it slipped slightly below 2% for the next four quarters. In 2017 the 2% growth rate was back and has [...]

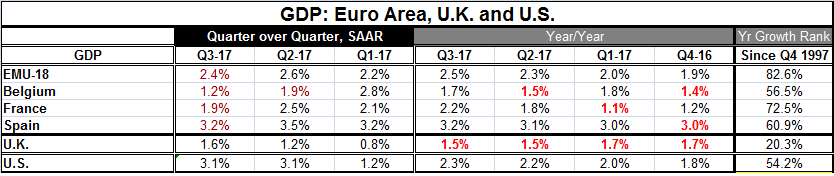

From the end of 2012, EMU year-on-year real GDP has been gradually accelerating. In Q2 2015, it reached a growth rate of 2.0%. Then it slipped slightly below 2% for the next four quarters. In 2017 the 2% growth rate was back and has stepped up to 2.3% in Q2 and 2.5% in Q3.

From the end of 2012, EMU year-on-year real GDP has been gradually accelerating. In Q2 2015, it reached a growth rate of 2.0%. Then it slipped slightly below 2% for the next four quarters. In 2017 the 2% growth rate was back and has stepped up to 2.3% in Q2 and 2.5% in Q3.

Of course, the headlines on this report speak of a quarter-to-quarter growth gain of just 0.6% compared to 0.7% last quarter. But the broader fact of greater important is that GDP is consistently churning out solid rates of growth and the quarterly fluctuations are not really what is the most significant. More importantly, the year-on-year pace has continued to show GDP advancing and that the pace has moved up and that puts the quarterly fluctuation in better perspective.

During this expansion push, EMU GDP growth has generally tailed U.S. growth. But now the two annual GDP growth rates are at parity over the last four quarters and EMU growth has actually surpassed the U.S. by small amounts over the past two quarters. That pattern, however, is reversed if we look at the annualized quarterly rates of growth with the U.S. putting in two quarters of 3.1% growth back-to-back as EMU quarterly growth rates have averaged 2.5%.

However, relative to their respective recent histories, it is the EMU that is stronger. The current EMU year-on-year growth rate of 2.5% ranks in the top 18% of all growth rates since 1997. For the U.S., the 2.3% year-on-year growth rate ranks only in its 54th percentile, a much lower and more moderate standing.

Not surprisingly, with this persistent growth, the EMU unemployment rate has continued to be whittled down. While there is still a great deal of disparity within the EMU, the EMU rate has sunk to 8.9%, its lowest level since January 2009. Germany is experiencing a post reunification low in its unemployment rate, but the EMU rate at 8.9% is still high compared to the U.S. rate of 4.2%. Despite all the excitement about improved EMU growth and prospects, the euro area still has long way to go.

As the ECB ponders policy, euro area inflation eased unexpectedly if only marginally, in September. The 'flash' HICP data from Eurostat showed Tuesday that inflation slowed to 1.4% in October from 1.5% in September. Economists had expected the inflation to remain stable at 1.5%. In any event, the ECB, like the Fed in the U.S., finds inflation below its target and not even gaining on it. Neither of the central banks will be happy about that. While many were flummoxed that the ECB did not move more aggressively to end its extra stimulus programs, it is after all a central bank with a single objective (inflation control!) and inflation continues to linger well below its objective as it has done for an extended period of time. Against that reality, the ECB actions seem more even handed than ham-handed. Maybe it's the critics who are ham-headed?

On balance, Europe has turned in some better economic numbers. There is more growth and growth is looking a bit more solid if only in the 2% to 2.5% corridor.

Inflation remains too low, underscoring that there is no jet-take-off in progress and room for the ECB to continue to demonstrate patience.

The unemployment rate continues to make progress, but its progress is very slow and the level of the unemployment rate is still very high.

As the ECB moves to peel off the various layers of stimulus, there are still banking issues in Europe, especially in Italy, that have not been resolved. Spain has just imposed direct rule on Catalan and snap elections are to be called; that situation remains touch-and-go.

Growth in the U.S. has got stronger, but that is strength with strings so it will bear watching as the hurricane effects play out over a broader period.

On the central bank front, the Bank of England may be on the verge of a rate hike this week. In the U.S., the Fed meets (no action expected), but a new Fed chair announcement is anticipated on Thursday. The Bank of Japan just met and affirmed its ongoing policy stance. So after the BOE meeting and the Fed chair announcement on Thursday, we should be in for an uneventful period of calm involving the key central banks. It's about time.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief