Global| Feb 02 2021

Global| Feb 02 2021EMU GDP Growth Rates Cluster

Summary

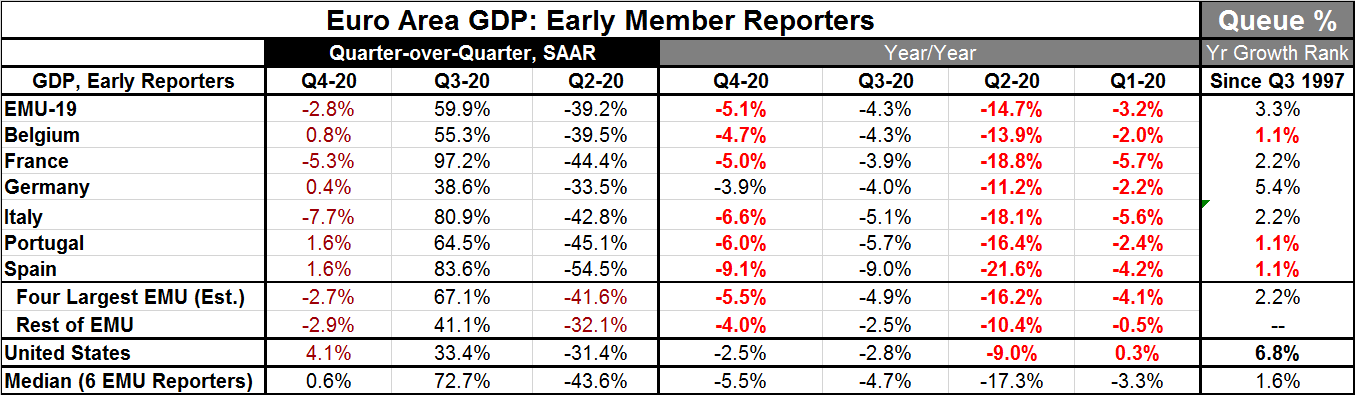

The EMU region has just released its GDP growth rate which fell by 2.8% (saar) in Q4. Of the six early EMU reporters in the table, only two, Italy and France, showed GDP declines in Q4. This, however, is an odd quarter as it is the [...]

The EMU region has just released its GDP growth rate which fell by 2.8% (saar) in Q4. Of the six early EMU reporters in the table, only two, Italy and France, showed GDP declines in Q4. This, however, is an odd quarter as it is the first close-to-usual quarter after seeing two quarters of raucous GDP rates of growth.

The EMU region has just released its GDP growth rate which fell by 2.8% (saar) in Q4. Of the six early EMU reporters in the table, only two, Italy and France, showed GDP declines in Q4. This, however, is an odd quarter as it is the first close-to-usual quarter after seeing two quarters of raucous GDP rates of growth.

The Virus Imprints GDP Growth Patterns

We see everywhere in the EMU, and globally as well, countries that had GDP pummeled in Q2 as the virus spread and efforts were made to contain it. Then GDP spurted gain back gaining much of the lost ground almost immediately but failed to gain it all back in Q3. So Q4 brings a little more differentiation as some countries continue the rebound and some suffer further declines as the particulars of the virus have differed from country to country and as infection cycles take on differing characters. However, the graphic plots year-on-year GDP results. On that basis, we can see how similar the reaction to the virus has been in terms of the impact on GDP. Similarities continue to dominate the data for now.

If we carve the EMU up into the top four economies vs. the rest, we find in Q4 those two groups have nearly identical annualized rates of growth. The virus is homogenizing what economics are facing to a large extent. As recovery progresses, it is likely that more differences in national rates of growth will arise. But for now, growth rates have been tightly clustered.

Vaccine Confidence and the Future

Of course, getting these economies back in gear will depend on the virus and on the progress with vaccinations. It will not just be about vaccination speed but also about how attitudes shift and how much confidence and trust people have as the vaccination process rolls forward as well as government policies and central bank efforts. If people are wary, they won't be participating in the economy very robustly even with widespread vaccination and government support.

The State of Virus

The virus currently is spreading and doing so unevenly.

• Spain's cases remain high although there is some evidence of infections and deaths turning the corner and becoming less widespread.

• Germany is keeping its lockdown in place through mid-month, but it is clearly showing reduced infections and deaths compared to its recent peaks. Germany is concerned that the more aggressive new strain from the U.K. may be taking over and could push the spread faster, so it is taking a conservative approach to opening back up.

• France is past its daily infect peak of 88,790 reached in early-November. But compared to a subsequent low point in early-December, infections are on a mild but clearly rising gradient since then in France. The deaths curve in France mimics these trends swooning to a low in early-January then mildly picking up again.

• In Italy, the spread has been reduced but still runs at a pace that is high compared to any period before late-October of last year. The death curve in Italy is also off its peak but still running at a relatively high pace. It's possible that the death rate is in the process of falling fast, but the data are too fresh to be reliable and it seems less likely since infections have not paved the way for such a shift in deaths.

• Portugal is having resurgence in infections and looking at its greatest spread so far. In Portugal, the death curve is rising sharply to a clear new high. Portugal is in trouble.

• In contrast, Belgium shows very low and very stable rates of infection after seeing the spread peak in late-October. Deaths in Belgium continue to decline. They are still high relative to June-September results, but there is a clear sense of progress having been made.

As the virus has spread somewhat more irregularly through Europe, we would expect to see a more diversified pattern of growth rates in Europe as well.

The Road Ahead

The EU has settled its differences with AstraZeneca, but the upshot is that it will wind up with fewer vaccine resources than it had expected. That will make the challenge of vaccinating everyone in the EU a more difficult task. But we are finding that planning to deliver a vaccine and actually delivering a vaccine have their own particular differences. The best laid plans can go awry – and they are. The good news is that vaccine resistance seems to be wearing down. And if that continues, it will make the process of vaccinating everyone in these prioritized queues more efficient. Right now distribution is stopped in the Northeastern United States because of an intense snow storm. The challenges just keep on coming, but healthcare workers are fighting back.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief