Global| Jun 11 2019

Global| Jun 11 2019Economy Watchers Index Slips

Summary

Japan’s economy watchers index weakened in May after the current index showed some rebound in April. At a level of 44.1 the economy watchers current index was last weaker in June of 2016. The index has decelerated over 3-months [...]

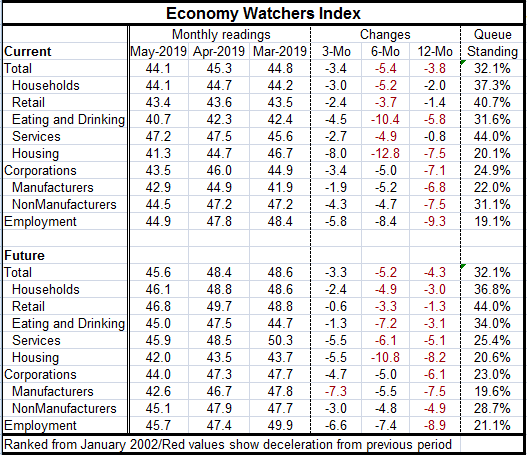

Japan’s economy watchers index weakened in May after the current index showed some rebound in April. At a level of 44.1 the economy watchers current index was last weaker in June of 2016. The index has decelerated over 3-months 6-months and 12-months.

Japan’s economy watchers index weakened in May after the current index showed some rebound in April. At a level of 44.1 the economy watchers current index was last weaker in June of 2016. The index has decelerated over 3-months 6-months and 12-months.

The Future index also fell on the month. It is also at its weakest point since June of 2016. The future index falls on all horizons from 3-months, from 6-months and year-over-year.

In the current index the weakest diffusion reading in May is for eating and drinking places with a diffusion reading of 40.7, its weakest performance since May of 2016. However, the biggest decline over the past 12-months is for the diffusion index for employment that fell by 9.3 diffusion points to stand at 44.9 in May.

The Current Index The diffusion readings also are ranked over a period from January of 2002 to date. The current headline has a 32 percentile standing putting it just into the lower one third of all readings since January of 2002. The strongest current reading on this time line is for services that show a 44.0 percentile standing still below that sector’s median for the period. The weakest value assigns to current employment with its 19 percentile standing in the lower one fifth of tis distribution. There are four readings in the bottom 25 percentile of their historic queues of value. That marks a lot of weakness against not strength at all in the current index or any of its components.

The Future Index At a reading of 35.6 the Future index also has a standing in the 32nd percentile of its historic queue of values. The weakest future component is housing with a 42.0 diffusion reading. The largest drop in diffusion over the past 12-months is for expected employment with an 8.9 point drop. The weakest component standing is for the expectation of manufacturers with a rank standing at its 19th percentile. Five components have a standing in their 25th percentile or lower. The strongest future reading is the 44th percentile standing, that one is for retail.

Momentum Over 12-months all the future components and seven of ten current diffusion indices show weaker reading than they had 12-months ago. Over six months the Future index showed deterioration in 6 of 10 diffusion measures, the same count as for the current survey. And while all diffusion readings show negative changes over six months only the future expectation for manufacturing shows a larger drop over three-months than it has seen over six months. However, if we annualize the drops over 3-months compared to six months there are larger drops over three months than over six months in 15 out of 20 of the current and future observations. Japan’s weakness remains in play.

Summing up On balance Japan’s economy is still weak. A revised first quarter GDP report today did lift Q1 growth to a +0.6% gain from a +0.5% gain but that is fine tuning the estimate and does not change the outlook in a meaningful way. Of course, with China, Japan’s largest trade partner, and the US locked in a trade war some additional fallout for Japan is still likely. There is unlikely to be a positive benefit from this trade war for Japan. Fortunately, Trump and Xi are still expected to be talking but the prospects for relief from the trade war are simply unknown.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief