Global| Mar 18 2013

Global| Mar 18 2013E-Zone Trade Surplus Shrinks, Will Europe Shrink Too? Does Cyprus Matter?

Summary

Trade trends for EMU - The EMU trade surplus shrank in January as imports rose sharply month-to-month and as exports posted some growth as well. While exports are showing some sign of revival, the three-month rate of growth is only [...]

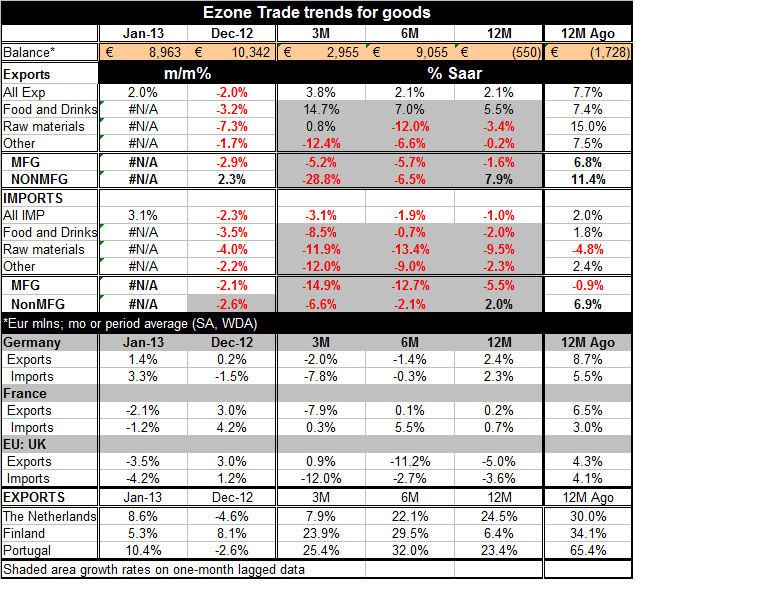

Trade trends for EMU - The EMU trade surplus shrank in January as imports rose sharply month-to-month and as exports posted some growth as well. While exports are showing some sign of revival, the three-month rate of growth is only 3.8% annualized compared to 2.1% (annualized) over both 6-months and 12-months. And these are only nominal numbers. Moreover, the export bump of 2% m/m only offsets the 2% decline from one month ago.

Trade trends for EMU - The EMU trade surplus shrank in January as imports rose sharply month-to-month and as exports posted some growth as well. While exports are showing some sign of revival, the three-month rate of growth is only 3.8% annualized compared to 2.1% (annualized) over both 6-months and 12-months. And these are only nominal numbers. Moreover, the export bump of 2% m/m only offsets the 2% decline from one month ago.

The chart makes it clear that the export and import trends are not turning although their pace of deterioration may be slowing for the year-over-year calculations.

But, for imports, the sequential growth calculations from 12-months and in are weakening. Over three-months the drop is at a 3.1% pace over 6-months imports are down at a 1.9% pace and over 12-months the rate of decline is at 1%. That is getting progressively worse.

Trade and growth and beyond - Activity in the Zone is continuing to contract and that is playing out in the import trends if not in the monthly numbers each and every month. Italy, which reported its own trade figures today, reports that exports to fellow European Union nations rose by 2.6 percent Year-on-year; exports to non-EU countries climbed 17.6 percent. That rather underscores the weakness of demand in the EU. The value of Italian imports, meanwhile, decreased 1.8 percent year-on-year in January underscoring the weakness of demand in Italy. . Compared to December, Italian imports moved up 0.4 percent. Imports from the European Union rose 2.4 percent from a year earlier, while arrivals from countries outside the EU fell by 5.6 percent. Italian demand is weak.

But the news-du-jour is much more focused on the policies of the EU and its treatment of its troubled members. Today Portugal was given a longer period to reach its austerity targets. But Cyprus, long under the threat of bankruptcy, was to be 'helped' with an advance of 10bln Euros to be supplemented by an EU-requested 'plan' to place a two tier tax on its BANK DEPOSITS.

There are many different angles from which to understand this proposal foisted on Cyprus by other European monetary union members. But now that the Cyprus Parliament is postponing its vote we are hearing from participants at the EU summit that are distancing themselves from the decision. The ECB claims that it was not in favor of raising taxes on deposits below the level of about 125.000 Euros. We know that coming into the meeting one of the German positions was that Cyprus was too small to matter. Since when is principle not an issue if a union member is small? And that is the point on which the European Union has just skewered itself.

Cyprus is not too small to matter if it becomes a case that reveals the way that the European power structure will deal with a fellow member. Although the tax that is being placed (proposed, actually) on bank deposits is a two-tiered tax with a much higher rate on deposits over 100,000 Euros, the fact is that there is still a significant tax on smaller deposits. This tax seems to be a violation of the principle that the deposits are protected by deposit insurance. Protected from 'what' one might wonder? The answer, of course, is 'bankruptcy,' not government confiscation. This is a tax that will fall on all sorts of economic transactors and in all sorts of economic transactions. Pity the poor firm that just augmented its bank account before the tax calculation date in order to meet its weekly or monthly payroll- or more cruelly, one that moved funds into its demand deposit account to make a tax payment!. Pity the poor couple buying a home that has just sold stock to place liquid funds in a checking account to secure the purchase of a home...more than 100K Euros? That's nearly a 10% tax. To the extent that bank deposits represent wealth, this tax can be viewed as a kind of wealth tax that Prime Minister Hollande tried unsuccessfully to implement in France. For the situation in Cyprus it is much stickier than that.

Black-market money looking to be laundered is believed to have moved in from Russia. It's reported that Russians have about $31 billion in deposits in Cyprus. The nearly 10% tax on large deposits will raise approximately $3 billion from Russian sources. However the European Community apparently did not want to target only these high value deposits because they were afraid that Russia would complain that it was being targeted. This allegedly is the reason for placing a two-tiered tax on all deposits. However, recall that this is not a tax yet this is a proposal that is waiting for consideration in parliament where the vote on this proposal is being postponed.

Cyprus's banks were thrown into this tizzy largely over the problems in Greece. Cypriot banks took their lumps in Greece along with all other banks. Like Greece, Cypriot banks have had deposit inflows from the ECB on their target-2 balances. Cyprus would seem to have more bargaining power than what has been revealed by the (still pending) imposition of this tax. While Cyprus has been developing as a banking-center in the region and has ambitions to be more of a banking center in the future, this deposit tax is precisely the kind of thing that will kill any ambitions that Cypriot banks may have to becoming more of a financial center. The plea that this is a one-time deal is not going to impress anyone.

The European Community shows very little sign of sophistication or understanding of banking issues. While the Community claims to want the United Kingdom to remain part of the European Community the Community itself has pushed ahead with plans for a financial transactions tax that would be devastating to the financial center in London. And now this heavy-handed approach on Cyprus underscores either the willingness to devastate Cyprus's financial sector or the lack of understanding that this policy will have the same effect.

This is exactly the kind of policy interference that will cause Cyprus to rethink whether it is better positioned inside or outside the European Union. It is a small country. That the Union would ride roughshod over it maybe makes it a club to which Cyprus will no longer wish to belong. Access to Europe's larger market and the shelter of being in its currency area may not be worth paying the price that the broader European Community doesn't care if its policies wreak havoc on poor Cyprus whose GDP is only one quarter of one percentage point of that of the entire European system.

So we can add Cyprus to that list of countries that may have a clearer and more pressing plan for their future than simply remaining in the European monetary Union and doing what they are told. Italy clearly has had enough of euro-austerity and it's hard to see how Europe puts Italy's toothpaste back in its austerity-tube. While the Community has tried to rehabilitate its image by extending the deadline for Portugal to meet its austerity guidelines this past weekend, the clear message we get is that Germany is running the show. The operative doctrine is based upon the premise that pain prevents future transgressions. That has been the operative European policy response for some time. While tough-love often makes for good monetary policy there is also something to be said for sophistication and enlightened self-interest. At the end of the day these policies from the European Union are being heavily influenced by German demands and do not seem to be sustainable.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief