Global| May 17 2013

Global| May 17 2013e-Zone Car Sales Show Some Life, EU Car Sales Show Even More

Summary

Automobile registrations are improving their rising trend for the European Union in April despite s small set back in the month. They are off by1.4% after a sharp gain of 7.2% in March. Over three months EU registrations are up at an [...]

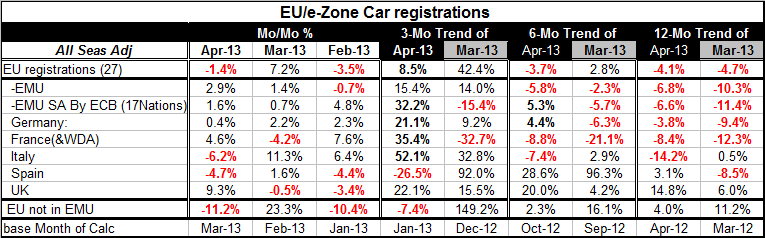

Automobile registrations are improving their rising trend for the European Union in April despite s small set back in the month. They are off by1.4% after a sharp gain of 7.2% in March. Over three months EU registrations are up at an 8.5% annual rate. Over six-months they show a 3.7% annual rate drop. Registrations are still down by 4.1% over 12 months. Year-over-year sales were last stronger than this in June 2012 when they fell by 2.8% year-over-year. In fact, we have to go back to November 2011 to find the next sales decline year-over-year that is smaller than this month's -4.1%. September 2011 marked the end of increases in year-over-year auto registrations in the European Union (27 countries).

Automobile registrations are improving their rising trend for the European Union in April despite s small set back in the month. They are off by1.4% after a sharp gain of 7.2% in March. Over three months EU registrations are up at an 8.5% annual rate. Over six-months they show a 3.7% annual rate drop. Registrations are still down by 4.1% over 12 months. Year-over-year sales were last stronger than this in June 2012 when they fell by 2.8% year-over-year. In fact, we have to go back to November 2011 to find the next sales decline year-over-year that is smaller than this month's -4.1%. September 2011 marked the end of increases in year-over-year auto registrations in the European Union (27 countries).

Comparing the performance of sales in the EU versus the European Monetary Union we see clearly that the EU registration figures have done much better.

The line located at the bottom of the table is for the countries that are members of the European Union but not the Monetary Union. It shows that sales there are up 4% year-over-year, as well as up to a 2.3% pace over six months; they are surging at a 22% annual rate over three months. EU-nonEMU registrations fell by 11% in April compared to March, after surging by 23% in March.

We can also look to see where auto registrations have done the best job of recovering their past cycle peak .For the entire EU the answer is that current registrations are about 72% of their past cycle peak, while in EMU registrations are back to 69% of their past cycle peak. In the countries that are in the European Union but not the monetary union registrations have recovered to 73% of their past cycle peak. By comparison German registrations are at 71% of their past cycle peak, Spain's are only back to 40% of their past cycle peak but in the UK registrations are back to 94% of their cycle peak.

Car 'sales' are only one indicator of health in the euro-Zone. But, retail sales in the Zone mostly continue to slumber. Returning to the auto metric, recent news reports are suggesting the Fiat which had previously gained a large stake in the US automaker, Chrysler, is planning to purchase the rest of that stake and is even pondering moving its headquarters to the United States. Fiat currently is headquartered in Italy in the city Turin. Back in 2004 the proportion of Fiat sales in Italy hovered around 90% but in 2012 the proportion has dropped to 24% (Italy's Nightmare). The car market in Europe has deteriorated so much at least for Fiat that it comes to identify much more with its sales in North America than its sales in Europe, despite his obvious European roots.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief