Global| Oct 11 2004

Global| Oct 11 2004Consumer Credit Usage Weak But Total Liabilities Strong

by:Tom Moeller

|in:Economy in Brief

Summary

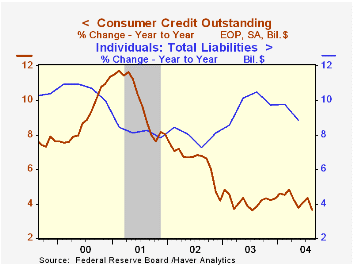

Consumer credit outstanding fell $2.4B in August following an $11.2B spike in July. Year-to-year growth in consumer credit of roughly 4% was depressed as individuals shifted borrowing to lower interest rate, home equity lines of [...]

Consumer credit outstanding fell $2.4B in August following an $11.2B spike in July. Year-to-year growth in consumer credit of roughly 4% was depressed as individuals shifted borrowing to lower interest rate, home equity lines of credit.

In August, revolving credit outstanding fell $3.4B (1.8% y/y) and usage of nonrevolving credit was up a modest $0.9B (4.8% y/y). Total consumer credit accounts for just 15% of total credit owed by individuals.

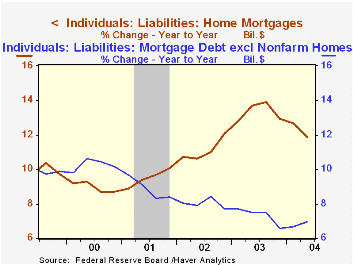

According to the Federal Reserve's broader Flow of Funds Accounts, total credit owed by individuals surged 8.8% y/y through 2Q04. The strength was driven by 11.9% growth in mortgage debt on nonfarm homes (55% of individuals' total liabilities) and also by 7.0% growth in mortgage debt excl. homes (12% of individuals' total). "Other liabilities" rose 7.8% y/y and are 16% of individuals' liabilities.

The ratio of individuals' assets to liabilities was 2.27 in 2Q versus 2.31 last year and a peak of 3.38 in 1999. Since 1999, assets rose at a 1.6% annual rate while liabilities surged at a 9.2% annual rate per year.

| Consumer Credit Outstanding | Aug | July | Y/Y | 2003 | 2002 | 2001 |

|---|---|---|---|---|---|---|

| Total | $-2.4B | $11.2B | 3.7% | 4.3% | 4.2% | 8.0% |

| Revolving | $-3.4B | $5.6B | 1.8% | 2.1% | 1.4% | 6.6% |

| Nonrevolving | $0.9B | $5.7B | 4.8% | 5.6% | 5.9% | 9.0% |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief