Global| Apr 14 2006

Global| Apr 14 2006Commercial Paper Shows Rapid Growth: Consumer-Credit-Backed Paper and Foreign Issuers Increase Their Share in [...]

Summary

This past week, the Federal Reserve Board published significant revisions to its data on commercial paper outstandings. The total amount of paper issued by all businesses is little changed, but several categories were reorganized or [...]

This past week, the Federal Reserve Board published significant revisions to its data on commercial paper outstandings. The total amount of paper issued by all businesses is little changed, but several categories were reorganized or redefined. These changes give a much better description of this source of short-term corporate finance. The new data begin in 2001. The history for some series, including the total, has been linked, as explained below. The monthly data we discuss here are contained in Haver's main USECON database. The "old" data are still available in our storage place for old data, USARC06. Current weekly data reside in our basic WEEKLY database. The old pre-revision weekly data are not archived.

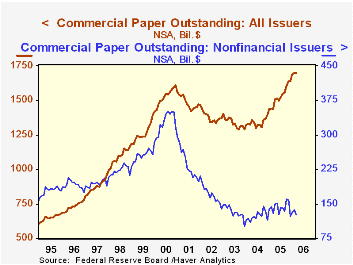

The commercial paper market historically was best known as an alternative market funding source for nonfinancial corporations, at times when bank loans were seen as too expensive or possibly not available due to tight monetary policy. Finance companies, especially those affiliated with major auto companies and well-known consumer-credit lenders have also long issued paper. In recent years, usage of commercial paper has changed. In the mid-1990s, nonfinancial corporate issues were nearly 30% of total paper outstanding. This share began to drop precipitously just before the recession of 2001 and has stabilized but not recovered. In the March data, the nonfinancial segment constituted a mere 7.8% of the total, the lowest ever in the 37-year history of the data. These data were little revised in the Fed's new reorganization, and we have connected them directly to the former series.

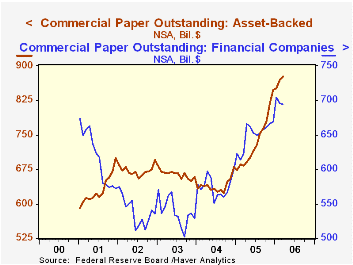

Financial companies have also altered their approach to the market. Some paper is backed by companies' general financial resources. Other commercial paper is backed by specific loans, including automobile and credit card debt. In the reorganization of the data, the Fed has pulled out this so-called "asset-backed" paper into a completely separate category. See in the second graph how rapidly that has expanded, particularly in just the past year. It grew 25% across 2005, and in the following three months has accelerated further to 28.3% growth in March over the year-ago month.

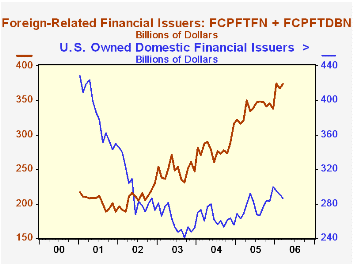

Conventional finance company paper also continues to grow. Users, according to the Fed's flow-of-funds data (in Haver's FFUNDS database) include bank holding companies and so-called funding corporations, popularly known as hedge funds. Foreign issues have stepped up notably as well. This latter development is evident directly from the commercial paper data. In the third graph, we added foreign issuers and domestic issues for which the parent company is foreign. This sum has been climbing steeply, while domestic paper from U.S.-owned firms has risen only modestly since 2003 and remains well below its pre-recession level.

Note that all of these financial series, while titled similarly as before the Fed's new revisions, look very different. Probably the separation of all the asset-backed paper is a main reason. Also, some paper is now classified as backed by letters-of-credit, heretofore a minuscule item, but which now stands at about $30 billion. The Fed has additionally been more exacting, pulling out items where an issuer's domicile or industry is not clearly identified. So several series have been added which are titled "other".

| Seasonally Adj, Bil.$ | Mar 2006 | Feb 2006 | Dec 2005 | Dec 2004 | Dec 2003 | Dec 2002 |

|---|---|---|---|---|---|---|

| Total | 1,705.1 | 1,687.5 | 1,631.0 | 1,375.7 | 1,260.7 | 1,341.2 |

| Nonfinancial Companies | 134.2 | 134.6 | 132.2 | 119.7 | 104.0 | 147.7 |

| Financial Companies | 692.5 | 690.9 | 667.3 | 595.2 | 519.7 | 522.9 |

| Asset-Backed | 878.2 | 861.9 | 831.3 | 660.7 | 637.0 | 670.7 |

| Memo: Financial + Asset-Backed | 1,570.7 | 1,552.8 | 1,499.0 | 1,256.0 | 1,156.8 | 1,194.0 |

| Old "Financial Companies" | 1,578.7 | 1,559.8 | 1,513.7 | 1,268.2 | 1,160.3 | 1,193.5 |

Carol Stone, CBE

AuthorMore in Author Profile »Carol Stone, CBE came to Haver Analytics in 2003 following more than 35 years as a financial market economist at major Wall Street financial institutions, most especially Merrill Lynch and Nomura Securities. She had broad experience in analysis and forecasting of flow-of-funds accounts, the federal budget and Federal Reserve operations. At Nomura Securities, among other duties, she developed various indicator forecasting tools and edited a daily global publication produced in London and New York for readers in Tokyo. At Haver Analytics, Carol was a member of the Research Department, aiding database managers with research and documentation efforts, as well as posting commentary on select economic reports. In addition, she conducted Ways-of-the-World, a blog on economic issues for an Episcopal-Church-affiliated website, The Geranium Farm. During her career, Carol served as an officer of the Money Marketeers and the Downtown Economists Club. She had a PhD from NYU's Stern School of Business. She lived in Brooklyn, New York, and had a weekend home on Long Island.