Global| Jan 31 2019

Global| Jan 31 2019China's MFG PMI Continues to Contract as EMU Weakens; China's MFG Does Not Worsen in January

Summary

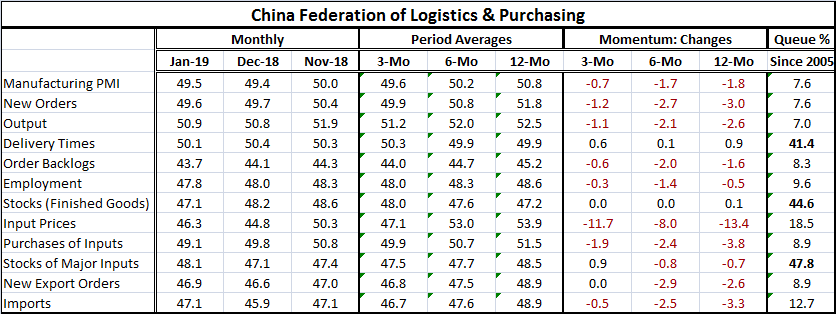

The China manufacturing PMI continues to be weak; it signals contraction in January albeit at a pace ever so slightly improved compared to December. It marks the first back-to-back PMI readings below 50 since January-February of 2016. [...]

The China manufacturing PMI continues to be weak; it signals contraction in January albeit at a pace ever so slightly improved compared to December. It marks the first back-to-back PMI readings below 50 since January-February of 2016.

The China manufacturing PMI continues to be weak; it signals contraction in January albeit at a pace ever so slightly improved compared to December. It marks the first back-to-back PMI readings below 50 since January-February of 2016.

In addition, the levels of the PMI readings and components are universally low and for the most part extremely low. Delivery speeds, stocks of goods and stocks of major inputs are all below their medians with standings in their 40th percentile decile. At that, these readings are among the strongest components in the survey. Among the rest of the components, only input prices and imports have queue percentile standing readings above their respective 10th percentile standing (input prices, 18.5%; imports, 12.7%).

The headline PMI has a standing in its 7.6 percentile, the same as for new orders; output has a standing in its 7th percentile. These are very weak sectors.

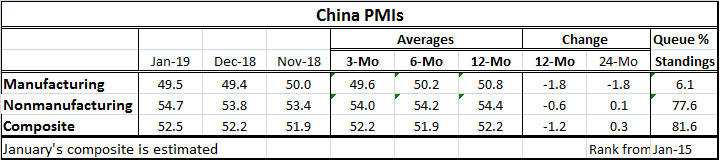

On a shorter timeline, we also have the nonmanufacturing PMI for China. The nonmanufacturing headline moved higher in January and stands in the 77.6 percentile of its historic queue of data. This compares to a 6.1 percentile standing for manufacturing on the timeline back to January 2015. The strength and the advance in the nonmanufacturing PMI is very helpful with manufacturing on the ropes.

Both the manufacturing and the nonmanufacturing gauges are lower on balance over 12 months. Nonmanufacturing has fallen by 0.6 points on that basis and manufacturing has fallen by 1.8 points. Over 24 months, the change in the manufacturing index is the same at -1.8 and nonmanufacturing is a thin tick higher.

While both sectors have been in the grip of deterioration, nonmanufacturing has managed to improve for two months in a row.

China's weakness comes at a difficult time since there is global weakness on top of this.

China's Manufacturing and Nonmanufacturing Situation

In the euro area and Europe broadly, there is retail sales weakness in December. Fresh results for Germany show a sharp decline in retail sales volume there in December. Of the seven early reporters of retail sales volume, six of them show December declines and five show declines over three months. Three of these reporters show declines over six months and three show declines over 12 months. Germany, Denmark, the U.K., and Norway show progressive deterioration in their respective rates of growth from 12-months to six-months to three-months. And four of six countries show declines in retail sales in Q4 2018 (QTD).

The table below shows the early EMU GDP result plus the results for four early EMU reports: Belgium, France, Italy, and Spain. Among these numbers, none shows a pick-up in growth in Q4 2018. In fact, all show deterioration except for Spain where the growth rate is level with Q3. And for Q3, Q2 and Q1, the year-on-year growth rates deteriorate across the board for these countries with Q3 2018 growth in Belgium as the only exception. So out of 20 growth rates (rates for five countries spanning four quarters), there is only one quarter of GDP acceleration in the mix. Year-over-year growth rates are clearly slowing - and slowing on a broad timeline across in Europe.

Meanwhile, Back as the Ranch...

In the U.S., the Fed yesterday gave a nod to deteriorating conditions as it jettisoned its tightening plans for the first time since end-2015. The Fed now claims to be truly neutral and wholly data dependent. But since 2015, it has been hiking rates while inflation has remained below its objective –and well below its first established objective. The Fed set an inflation objective of 2% on the PCE headline in 2012 and it continues to fall short of it; it is now cumulatively four percentage points below the path it originally set for the PCE index in January 2012.

The Fed has been hiking rates since 2015, an act that has clearly contributed to missing its inflation targets while all the time assuring us it was doing this because inflation was on track to be at 2% in the medium term. Just to walk you back on that, the Fed assumed something was true and took actions that actually prevented that assumption from coming true and that assumption was that the Fed would hit its price target. But suddenly, the Fed has stopped these shenanigans and is once again apparently worried about hitting its inflation target or at least using it as an excuse for a new policy gambit. Why?

We see a good deal of weakness in the Fed regional PMI indexes for manufacturing as well as for regional services and there is new weakness in the Chicago PMI (a mixed sector survey). U.S. growth has been a stalwart internationally and now it is fading and may be entirely slipping away in part because the Fed held to its tightening path too long and failed to see the lagged effects of its tightening catching up to it because it was looking ahead and chasing perceived neutrality with the Fed funds rate. We do not yet know that weak growth is in store for the U.S. growth, but there is some evidence of slowing in hand – and enough not to ignore it. We can keep our fingers crossed that signals are being exacerbated by weakness now being reversed in the wake of the government shutdown.

One if by Land, Two if by Sea

But the U.S. treasury yield curve is flat and remains very flat even after these new very market friendly actions by the Fed. Market signals are not yet clear and are not yet friendly. Fed funds futures had begun to look for a Fed rate cut ahead immediately after the Fed announced its policy decision of last December. What now? In addition, there is some evidence of some growing banking problems in Europe. Two large German banks may be force to merge by midyear. Italian banks have been shaky for a while and now Italy has two consecutive quarters of negative GDP growth. You do not want to see protracted weakness and banking sector problems bloom in the same garden. We still need to be vigilant and watch markets to see their signals. China's and Europe's weakness is real. As for the U.S., we do not know yet. This could be a new gripping series on Netflix- stay tuned.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief