Global| Sep 29 2005

Global| Sep 29 2005China Foreign Direct Investment: Strong but Uneven Gains, Heavy Reliance on Special "Foreign Investment Enterprises"

Summary

Further data were reported today on foreign direct investment in China for 2004. These data covered the total value of foreign investment contracts, including direct investment and "others", which covers leasing and other types of [...]

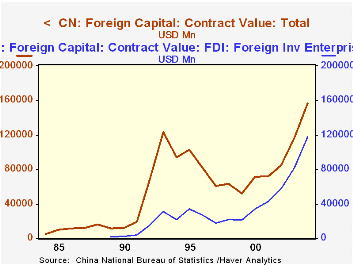

Further data were reported today on foreign direct investment in China for 2004. These data covered the total value of foreign investment contracts, including direct investment and "others", which covers leasing and other types of financing. The grand total of foreign investment contracts was $156.6 billion, 34% more than in 2003. A special vehicle, "foreign investment enterprises", is the main Chinese counterparty in these transactions. The data for these began in 1989 with $1.7 billion in committed inflows; last year they brought in $117.3 billion. The more familiar "joint venture" ownership vehicle, a partnership between a Chinese and a foreign firm, accounted for $27.6 billion in 2004.

These figures come from contracts for new projects. The flows of actual funding, so-called "capital utilized" are lower as the projects are actually accomplished. In 2004, the total amount of capital utilized was $64.1 billion, up from $56.1 billion in 2003.

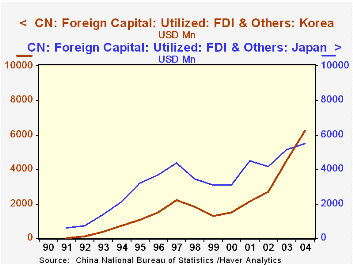

As we examined these data, the geographic origins of these funds and ownership interests drew our attention. Hong Kong entities are by far the largest providers of foreign capital for China, with $20.8 billion last year, about 32% of capital utilized. Other Asian interests are well represented, including Japan with $5.5 billion and Korea, $6.3 billion. Notably, last year was the first in which Korean inflows were larger than those from Japan. Western investors were less involved (though perhaps some Hong Kong capital represents a flow-through of Western money). German investors, for instance, have averaged just about $1 billion in Chinese FDI annually in recent years, and the UK, about $800 million. Nine major European countries together invested $3.8 billion last year, compared with $3.9 billion for the US. As seen in the table below, US funding has actually declined recently; it had been $5.4 billion in 2002.

General interest in China is growing, of course. Separate figures on the value of contracts year-to-date show that new contracts for standard FDI projects (excluding the "other" financing categories) are up in the first half of this year by 19% from the first half of 2004. At the same time, this is slower than 30%-40% growth of the prior couple of years. And the flow of capital utilized was actually a bit smaller in the first half of this year than last. In part, this reflects normal volatility in what are by nature uneven, "lumpy" flows. Even so, the impression of a continuously mushrooming volume of outside funding going into China is not quite an accurate one.

| Billions of US$ | 2005 | 2004 | 2003 | 2002 | 2001 |

|---|---|---|---|---|---|

| Total Foreign Capital: Value of Contracts |

156.6 | 116.9 | 84.8 | 72.0 | 71.1 |

| Foreign Capital Utilized | 64.1 | 56.1 | 55.0 | 49.7 | 59.4 |

| Capital Utilized from Hong Kong | 20.8 | 19.5 | 17.9 | 17.9 | 16.7 |

| Japan | 5.5 | 5.1 | 4.2 | 4.5 | 3.1 |

| Korea | 6.3 | 4.5 | 2.7 | 2.2 | 1.5 |

| Germany | 1.1 | 0.9 | 0.9 | 1.2 | 1.0 |

| U.S. | 3.9 | 4.4 | 5.4 | 4.5 | 4.4 |

Carol Stone, CBE

AuthorMore in Author Profile »Carol Stone, CBE came to Haver Analytics in 2003 following more than 35 years as a financial market economist at major Wall Street financial institutions, most especially Merrill Lynch and Nomura Securities. She had broad experience in analysis and forecasting of flow-of-funds accounts, the federal budget and Federal Reserve operations. At Nomura Securities, among other duties, she developed various indicator forecasting tools and edited a daily global publication produced in London and New York for readers in Tokyo. At Haver Analytics, Carol was a member of the Research Department, aiding database managers with research and documentation efforts, as well as posting commentary on select economic reports. In addition, she conducted Ways-of-the-World, a blog on economic issues for an Episcopal-Church-affiliated website, The Geranium Farm. During her career, Carol served as an officer of the Money Marketeers and the Downtown Economists Club. She had a PhD from NYU's Stern School of Business. She lived in Brooklyn, New York, and had a weekend home on Long Island.

More Economy in Brief