Global| Apr 02 2004

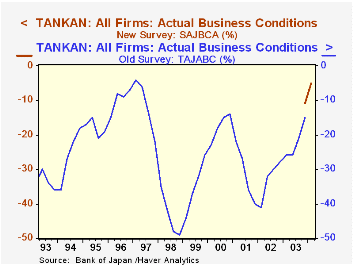

Global| Apr 02 2004BoJ Restructures TANKAN Survey to Match "New Economy"; March Results Better than Companies Expected

Summary

The Bank of Japan (BoJ) has reorganized the key TANKAN survey, its widely followed quarterly measure of business sentiment. In the initial report, issued yesterday, April 1, the new Business Conditions reading for March is -5, [...]

The Bank of Japan (BoJ) has reorganized the key TANKAN survey, its widely followed quarterly measure of business sentiment. In the initial report, issued yesterday, April 1, the new Business Conditions reading for March is -5, compared with -11 in December. On the old survey basis, December was -15. Due to changes in the selection and grouping criteria for companies in the sample, the new data are not comparable with the old. To the extent possible, December data were reaggregated according to the structure of the new survey, so there is one historical period for comparison with actual results and with a forecast for the current period.

The BoJ made three major changes in the sample composition. Like many other countries, it reorganized the industry divisions. Similar to the US shift from "SIC" to "NAICS", Japan is moving to the "Japan Standard Industrial Classification". This captures more of the new kinds of industries that have emerged during the recent technology boom; for example, "information services" and "communication", once subsumed in a broad "services" sector, are now shown separately. Secondly, the BoJ applied the results of a business census taken in 2001 to select firms for sampling. Third, it switched the method of designating businesses by size. Formerly this was judged on the basis of number of employees, but now capitalization is the criterion. This recognizes that some companies might utilize a small number of employees who actually operate a large business, such as a holding company. These changes together are thought by the BoJ to capture better the newer, more vibrant segments of the Japanese economy, which may have experienced better performance in recent years than the former industries and companies in the survey. They believe that the former survey results may have been biased downward due to its concentration on older, now less relevant industries and companies. Additionally, some concepts in the survey were redefined.

In terms of the survey results themselves, the following table indicates that business fortunes appear quite segregated by business size. Small firms are generally struggling, medium firms believe they abide in a mixed environment, and large firms are experiencing net positive performance. At the same time all major groups of companies performed better in the first quarter than they expected to. That is, the March "actual" is more positive or less negative than the December "forecast" value. Since there is no more history, it is not possible to judge whether this underestimation is a random circumstance or a habitual conservatism. Whichever would apply, large firms expanded on balance in the first quarter in both manufacturing and non-manufacturing sectors, and medium-sized manufacturing firms shifted into positive territory. Even small manufacturing companies had minimal erosion in the latest period, and they expect that to continue during the spring.

| Business Conditions: % Favorable minus % Unfavorable | December 2003 March 2004||||

|---|---|---|---|---|

| Actual | Forecast for March | Actual | Forecast for June | |

| All Firms | -11 | -12 | -5 | -6 |

| Large Firms* | 4 | 5 | 9 | 9 |

| Manufacturing | 7 | 6 | 12 | 12 |

| Non-manufacturing | 0 | 4 | 5 | 7 |

| Medium-sized Firms** | -8 | -9 | -2 | -2 |

| Manufacturing | -3 | -4 | 5 | 1 |

| Non-manufacturing | -12 | -11 | -7 | -6 |

| Small Firms*** | -19 | -20 | -13 | -15 |

| Manufacturing | -10 | -11 | -3 | -3 |

| Non-manufacturing | -25 | -27 | -20 | -21 |

Carol Stone, CBE

AuthorMore in Author Profile »Carol Stone, CBE came to Haver Analytics in 2003 following more than 35 years as a financial market economist at major Wall Street financial institutions, most especially Merrill Lynch and Nomura Securities. She had broad experience in analysis and forecasting of flow-of-funds accounts, the federal budget and Federal Reserve operations. At Nomura Securities, among other duties, she developed various indicator forecasting tools and edited a daily global publication produced in London and New York for readers in Tokyo. At Haver Analytics, Carol was a member of the Research Department, aiding database managers with research and documentation efforts, as well as posting commentary on select economic reports. In addition, she conducted Ways-of-the-World, a blog on economic issues for an Episcopal-Church-affiliated website, The Geranium Farm. During her career, Carol served as an officer of the Money Marketeers and the Downtown Economists Club. She had a PhD from NYU's Stern School of Business. She lived in Brooklyn, New York, and had a weekend home on Long Island.

More Economy in Brief