Global| Aug 22 2016

Global| Aug 22 2016Belgian National Bank Consumer Index Is Flat in August

Summary

The Belgian National Bank index remains a quintessential euro area marker as its consumer index is flat in August at -4, at the same level as in July but up two ticks from its June reading and also up two ticks from its year-ago [...]

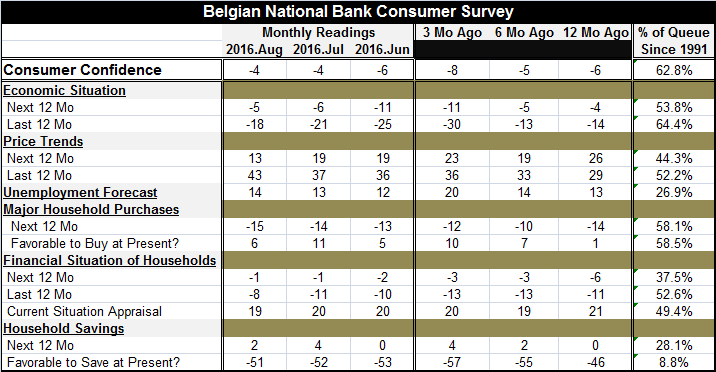

The Belgian National Bank index remains a quintessential euro area marker as its consumer index is flat in August at -4, at the same level as in July but up two ticks from its June reading and also up two ticks from its year-ago value. The Belgian index stands in the 62nd percentile of its historic range of values, leaving it more or less where the average European area index stands on most metrics. A low sixtieth percentile standing is above a median reading (which occurs at 50) but not by enough to be considered strong in any way. Yet, a low sixtieth percentile reading is solid enough to keep fears of economic decline at bay. It is the sort of lukewarm reading that has characterized much of the European recovery.

The Belgian National Bank index remains a quintessential euro area marker as its consumer index is flat in August at -4, at the same level as in July but up two ticks from its June reading and also up two ticks from its year-ago value. The Belgian index stands in the 62nd percentile of its historic range of values, leaving it more or less where the average European area index stands on most metrics. A low sixtieth percentile standing is above a median reading (which occurs at 50) but not by enough to be considered strong in any way. Yet, a low sixtieth percentile reading is solid enough to keep fears of economic decline at bay. It is the sort of lukewarm reading that has characterized much of the European recovery.

The economic situation expected over the next 12 months improved in August and that assessment has been getting sharply better over two months. Still, the historic standing of this metric is only in its 53rd percentile in August. The assessment of the economic situation over the last 12 months had also been improving rather rapidly and it had a relatively higher standing in it 64th percentile.

Price trends find that inflation over the next 12 months is expected to be weaker with a 44th percentile standing in August. Over the previous 12 months, inflation expectations had been building and in August they reached their 52nd percentile, a mid-range mark.

Expected unemployment conditions had ramped up three months ago but have since settled back to near their year-ago level and now show only minor elevation over the past two months. The queue standing of the expected measure is a relatively low 26th percentile, indicating that unemployment fear is lower only about 26% of the time.

The expected and current environments for consumer spending are slightly better than mid-range with both holding 58th percentile of queue standings. There is only a slight deterioration in train on expectations for the spending environment over the next 12 months.

The financial situation of the household has a weaker standing over the next 12 months than it had over the past 12 months; that's not a good sign. Yet, the impact on the expected spending environment has been small (see above). The ranking of that assessment over the next 12 months has a 37th percentile standing, compared to a 52nd percentile standing over the past 12 months. The current situation assessment comes in right at its 49th percentile, nearly on top of its historic median. There have been few changes in these gauges in recent months.

The household savings assessment has improved slightly over the past few months but is unchanged over the last year. The standing of the assessment is in the lower 28th percentile of its historic queue of data, indicating pressured prospects for saving. The current environment for saving is assessed as weaker only 8.8% of the time historically.

Belgium shows the stresses of the euro area. With overall measures that are largely mid-range and unimpressive and with job security not a real issue, there are still nagging areas of doubt lodged in the assessments of households' financial conditions and abilities to save. Belgium has been the epicenter of migrant terrorism as well, another factor that may be destabilizing perceptions of economic well-being.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief