Global| Mar 09 2017

Global| Mar 09 2017Bank of France Business Indicator Continues to Move Strongly Higher

Summary

Index traces out pattern of strength The Bank of France business indicator moved up to 103.9 in February from 101.7 in January. The index extends its tendency since early 2016 to show ongoing business sector improvement. In the wake [...]

Index traces out pattern of strength

Index traces out pattern of strength

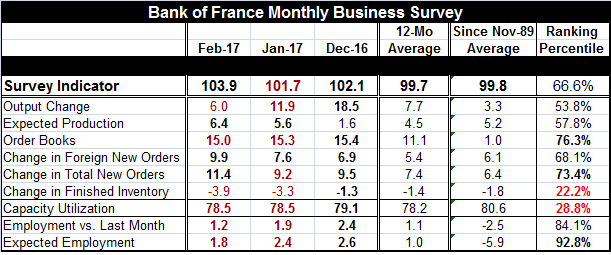

The Bank of France business indicator moved up to 103.9 in February from 101.7 in January. The index extends its tendency since early 2016 to show ongoing business sector improvement.

In the wake of this report, the Bank of France has upped is outlook for growth. The French economy is now forecast to grow slightly more than previously projected in the first quarter. Gross domestic product is expected to gain 0.4% in the first quarter, an upward revision from the Bank's previous estimate of 0.3%.

The index is up on the month on the strength of a gain in expected production and in new foreign orders and total new orders. Expected production rose to an index reading of 6.4 in February, up from 5.6 in January. The change in new foreign orders rose to 9.9 in February from 7.6 in January. Foreign orders have a 68.1 percentile queue standing in their historic ranking of responses while expected production has a more moderate 57.8 queue percentile standing. Total new orders rose to an 11.4 reading in February from 9.2 in January, sending the percentile standing for total new orders to a 73.4 percentile standing. These gains were enough to boost the headline to a 66.6 percentile standing in February, a reasonably good borderline top one-third standing for business all-around.

The monthly survey also produced some weakening readings. The output change reading slipped to 6 in February from 11.9 in January and 18.5 in December. It still holds a positive queue standing at the 53.8 percentile, but that is a more modest reading and outlook than in recent months. The total order book standing edged slightly lower to 15.0 in February from 15.3 in January. Still, the order book reading remains relatively firm at its 76.3 queue percentile standing. The change in the finished inventory metric logged a larger negative value in February. But that is a harder-to-read signal. A deeper inventory drawdown could be a positive event, signaling the need to rebuild inventories (we are not seeing that very strongly in the output change component but 'expected production' is still advancing.).

The two employment metrics in the table are unambiguously weaker; each is lower in February than in January and for each January also slipped relative to December. Still, the employment readings have the highest queue standings in the table at the 84.1 percentile for employment last month and a 92.8 percentile standing for expected employment. Both of these employment metrics slipped in February, but each is at a relatively high-water mark and these are important readings indicating how businesses view future business prospects. Order back log readings and employment standings tend to be highly correlated. And employment prospects are crucial for workers and for the knock-on impact such readings will have on consumer confidence.

French industry obviously still has some issues. Election issues swirl around it. There are the controversies involving ECB policy. And while the EMU and French PMI readings have been solid-to-strong, other indicators for Europe continue to be somewhat more uneven. The French business survey is on the whole positive and positive enough to get a forecast hike out of the BoF. But some aspects of the survey are clearly losing momentum. Solid growth prospects are not money in the bank here, but so far so good. France is making progress.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief