Global| May 25 2007

Global| May 25 2007Bank Loan Delinquencies & Charge-Offs Increase in Q1, But Remain Lower than During Last Recession; Great Variation [...]

Summary

The Federal Reserve released commercial bank "loan performance" data for Q1 2007 late yesterday, May 24. This information includes the dollar amounts of delinquent loans and loan charge-offs, which are taken as percentages of bank [...]

The Federal Reserve released commercial bank "loan performance" data for Q1 2007 late yesterday, May 24. This information includes the dollar amounts of delinquent loans and loan charge-offs, which are taken as percentages of bank assets outstanding to produce delinquency and charge-off rates. Both kinds of rates are published with seasonal adjustment and the charge-off rates are annualized.

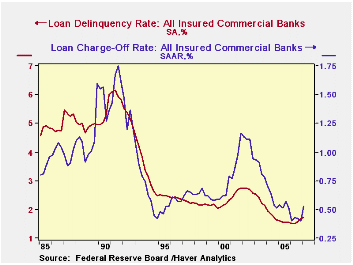

The overall delinquency rate for Q1 was 1.72%, up 0.03% from Q4's 1.69%. These are somewhat high compared with the last couple of years, but the period from 2000 to 2004 averaged 2.30%, that is, higher still. The latter time span included the recession following the tech boom/bust cycle. The charge-off rate in Q1 was 0.53%. As with delinquencies, this is higher than the most recent periods, but noticeably lower than the 0.82% average of 2000-2004. Delinquencies are loans overdue by 30 days or more; these remain active loans and continue to accrue interest. Charge-offs are loans removed from the books as uncollectible.

We illustrate the behavior of a few major types of bank loans. Total consumer loan delinquencies were just under 3% of the total amount of those loans, and as with total loans, larger than most recent quarters, but less than earlier times. In the second graph, we see that credit card debt, included within total consumer loans, has about a percentage point higher delinquency rate presently; this too has been higher in the past, both absolutely and relative to the total consumer loan amount.

The behavior of residential real estate credit highlights the secured nature of these loans. As widely publicized, the delinquency rate is rising. The new data here show that slightly more than 2% of banks' residential mortgages were delinquent in Q1, the largest proportion since Q3 2002. As with other loans, these delinquencies also remain lower than most prior periods, although the steep rise from just 1.62% in Q2 last year is discomforting. As to charge-offs, they are much different because they are "net"; the bank forecloses on the house and then sells it, recouping a good part of its loan value. So the amount it must charge off is really quite modest, as seen in the third graph. In looking at the graph, recall that the charge-off rates are annualized, so 0.16% in Q1 is really 0.04% at a quarterly rate. In other measures of mortgage quality, such as those from the Mortgage Bankers' Association, we focus on the foreclosure itself, so those rates are much higher than the net charge-off rate.

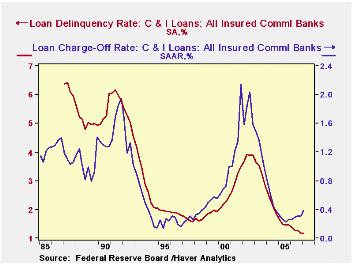

Business loans are seen to behave differently still. Delinquency rates in this sector are still going down, and Q1, at 1.18%, is the lowest in the 20-year history of the delinquency data. Charge-offs came at a 0.39% annual rate in Q1, also among the lowest for this series. These rates have ranged from 0.14% in Q2 1995 to 2.04% in Q3 2002. This latter would be quite severe: in that quarter 0.51% of business loans outstanding were deemed total losses. The US economy was coming out of a shallow recession, so the cyclical sensitivity of business credit is readily apparent.

| Commercial Banks, SA | Q1 2007 | Q4 2006 | Q3 2006 | Q1 2006 | 2006 | 2005 | Avg 2000 -2004 |

|---|---|---|---|---|---|---|---|

| Delinquency Rate: Total | 1.72 | 1.69 | 1.58 | 1.50 | 1.57 | 1.57 | 2.30 |

| Consumer Loans | 2.96 | 2.96 | 2.95 | 2.79 | 2.90 | 2.81 | 3.40 |

| Residential Real Estate | 2.04 | 1.94 | 1.76 | 1.59 | 1.75 | 1.55 | 1.93 |

| Business* | 1.18 | 1.18 | 1.26 | 1.39 | 1.27 | 1.51 | 2.92 |

| Annual Rates | |||||||

| Charge-Off Rate: Total | 0.53 | 0.40 | 0.42 | 0.40 | 0.42 | 0.54 | 0.82 |

| Consumer Loans | 2.44 | 2.18 | 2.15 | 1.84 | 2.06 | 2.75 | 2.78 |

| Residential Real Estate | 0.16 | 0.13 | 0.11 | 0.09 | 0.11 | 0.08 | 0.16 |

| Business* | 0.39 | 0.31 | 0.31 | 0.26 | 0.30 | 0.26 | 1.14 |

Carol Stone, CBE

AuthorMore in Author Profile »Carol Stone, CBE came to Haver Analytics in 2003 following more than 35 years as a financial market economist at major Wall Street financial institutions, most especially Merrill Lynch and Nomura Securities. She had broad experience in analysis and forecasting of flow-of-funds accounts, the federal budget and Federal Reserve operations. At Nomura Securities, among other duties, she developed various indicator forecasting tools and edited a daily global publication produced in London and New York for readers in Tokyo. At Haver Analytics, Carol was a member of the Research Department, aiding database managers with research and documentation efforts, as well as posting commentary on select economic reports. In addition, she conducted Ways-of-the-World, a blog on economic issues for an Episcopal-Church-affiliated website, The Geranium Farm. During her career, Carol served as an officer of the Money Marketeers and the Downtown Economists Club. She had a PhD from NYU's Stern School of Business. She lived in Brooklyn, New York, and had a weekend home on Long Island.

More Economy in Brief