Global| Dec 26 2018

Global| Dec 26 2018As 2018 Ends, Japan's Inflation Is Going Nowhere

Summary

Japan has been trying to restore modest inflation to its environment for a long time. The Bank of Japan runs a dedicated policy of pegging the 10-year JGB rate to zero, of pinning short rates below zero and of pumping up its balance [...]

Japan has been trying to restore modest inflation to its environment for a long time. The Bank of Japan runs a dedicated policy of pegging the 10-year JGB rate to zero, of pinning short rates below zero and of pumping up its balance sheet all to no avail on inflation. Japan had put its phased-in consumption tax hike on hold to spare weak economic growth. But now with still marginal growth and no inflation, the one-postponed consumption tax hike again is pending for 2019.

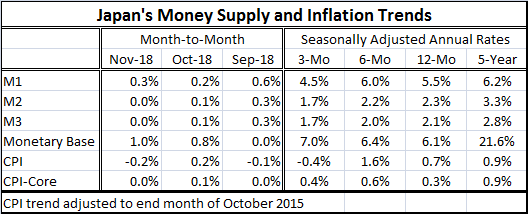

Japan has sloshed reserves into the banking system with little impact on money supply, defying what 'academics' expected. Over five years, Japan's monetary base is growing at a 21.6% annualized pace. That has only generated a 2.8% pace for M3, 3.3% pace for M2, and a 6.2% pace for M1. With interest rates so low and negative rates for short-term deposits, BOJ policies have stimulated some cash hoarding but that has not fueled more consumer spending.

One of the main reasons why inflation is not being generated is Japan's population whose profile is presented in the chart (on the right). For simplicity, this is a chart of population size, not of growth. But as you can see, the absolute size of Japan's population is shrinking. It is also an aging population. And while the population calculation was res-set in 2010, it is clear that population has reached a peak and is well on its way lower. Expanding- even greatly expanding- the size of the BOJ balance sheet has not be able to rekindle inflation in this environment

Another consumption tax hike is scheduled for this year after its previous postponement. PM Abe has signaled that he plans to go ahead with it later in 2019. Chart on the left (above) shows the impact of the consumption tax on measured inflation. Since we plot the CPI on the chart, the tax adds to the plotted level of consumer prices. On the first day of the tax implementation, the price level rises sharply and this translates into a stronger year-on-year price gain. For the next 11 months (12 months in all), the consumption tax boosts all inflation calculations made over 12 months. Then on the 13th month, the price level comparison will be made between the 13th month of the consumption tax hike and the first month of the hike. At that point, the impact of the consumption tax on the price level will no longer affect the inflation rate and the year-over-year rate calculation will drop sharply as it does in the chart. Chart on the left shows so clearly that as inflation humps up then snaps down the price level gain over the 12 months period of the consumption tax which was in place in 2014 to 2015 creates an inflation bubble that balloons then pops on a strict 12-month cycle. In the end, inflation was not boosted by that tax even though it added to the price level. Moreover, growth was weakened by the tax; there was a 2014 recession. And the tax led to slightly weaker post-consumption tax inflation compared to pre-consumption tax inflation by making the economy and consumption itself weaker.

However, there is the paradox here as when the consumption tax is announced it will create incentives for people to spend more now and it will boost growth first! Especially for any soon-to-be-higher-taxed item of substantial costs, consumers will see the wisdom of buying it 'now' instead of waiting. So an announced and credible date for the start of the consumption tax will also create leads and lags for consumer spending as it will drive spending and growth higher ahead of the tax then in the post-tax period ahead the shifted spending will take a bite out of growth for some months to come and might may even create the onset of recession. All this will complicate any assessment of the impact of the tax as well as complicate policymaking.

Inflation now

As 2018 comes to a close, inflation seems to be trending sideways-to-weaker. Global oil prices are weakening and there is the nascent tumble in global equity markets that may or may not presage a period of weaker growth ahead. In any event, weaker equity market prices are not going to stimulate any growth. With a mountain of its own fiscal debt, Japan is in no position to use fiscal policy to stimulate growth. Combined with its demographic circumstance, Japan faces huge impediments to getting growth or inflation higher.

Japan: Tradition impedes options

Japan has options, but it also has domestic social policy priorities. Japan has been very interested in preserving its population's homogeneity and its culture. These two objectives have made it difficult for Japan to unlock growth solutions which in the end might also be better inflation solutions. In the third calendar quarter of the year, PM Abe did introduce two new visas to allow low skill workers to stay longer and to permit higher skill workers to stay longer and to bring their families. Still, Japan is limiting immigration that might have been one way to mitigate the impact on growth of its population drop. It also has been reluctant to encourage more women to work professionally in the labor force, opting to preserving old cultural norms. But many of Japan's youngest also have opted to not have families because child rearing is so difficult and so expensive in this country of extremely high land values. Japan could open and support more daycare centers to encourage families to form, but as of yet values and policies in Japan remain on a mostly traditional track.

Outlook: Japan 2019

In this environment, the outlook for Japan in 2019 has to be guarded. The global economy has been weakening. Trade wars threaten to break out and spread more malaise. Meanwhile, Japan is on auto-pilot to its own policy move that will take growth down a peg or two then it is not clear that Japan has a peg or two to spare. And in the meantime, there is no sense that any progress on inflation is or will be made. After all its efforts, the BOJ will find itself back a square one with an even lower population once the new consumption tax has gone through its paces and likely weak growth to contend with as well.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief