Global| Nov 23 2009

Global| Nov 23 2009Although Stresses Vary, All States Endure Doubling Of Unemployment

by:Tom Moeller

|in:Economy in Brief

Summary

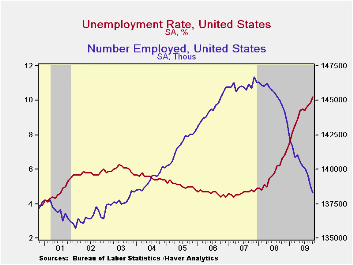

Overall, the U.S. unemployment rate touched 10.2% during October, just shy of the 10.8% postwar-record reached in December 1982. That, however, understates the severity of joblessness. In virtually all 50 states, since 2007 there has [...]

Overall, the U.S. unemployment rate touched 10.2% during

October, just shy of the 10.8% postwar-record reached in December 1982.

That, however, understates the severity of joblessness. In virtually

all 50 states, since 2007 there has been a doubling of the unemployment

rate. Currently, unemployment rates range from the high of 15.1% in

Michigan to the low of 4.2% in North Dakota. The jobless rate may even

rise further as it did after the last two recessions ended when the

labor force increased faster than employment. Conversely, a

"double-dip" recession this time, as some foresee, would raise

unemployment significantly higher.

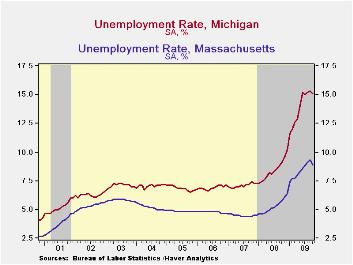

Michigan tops the list of states with the highest unemployment rate. (See table.) With its large exposure to the auto industry, Michigan saw its unemployment rate more-than-double to 15.1%. Since early last year, the number of unemployed in Michigan also has doubled to 733,000.Last month's cash-for-clunkers vehicle sales incentive program briefly stemmed the increase, but only a sustained rise in sales will encourage vehicle manufacturers to increase hiring.

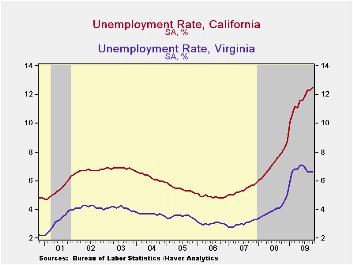

Amongst other large states, California has suffered the

enormously. The downturn in the high-tech sector and red-ink in the

state's budget has caused the unemployment rate also to

more-than-double to 12.5% from its low, but that understates the

severity of the situation. With its larger population, the rate

increase represents a 1.4 million gain in the number of unemployed.In

Florida, the severity of the unemployment rate's near-tripling to 11.2%

is due to a depressed tourism industry and reduced construction

activity. The number of unemployed rose by three-quarters of a million

persons. In Ohio, employment also relies heavily on the auto industry

though some stabilization is provided by the food-processing industry

and Wal-Mart's headquarters. Thus, the near-doubling of its

unemployment rate to 10.5% from last year reflects lower motor vehicle

production and an increase of roughly 300,000 in the number unemployed.

Perhaps a more diverse pool of industries has helped those states with unemployment rates lower than the national average. In Texas, with 12.1 million in the labor force, the strength in oil prices and the stability of the food industry have held the unemployment rate below the national average. Nevertheless, the number of unemployed has risen by one-half million since its 2007 low and the jobless rate has nearly doubled to 8.3%. In Massachusetts, with the workforce heavily exposed to the education & government sectors, the unemployment rate also has held below the national average at 8.9%. Virginia also has its disproportionate exposure to the government sector to help explain a relatively low unemployment rate of 6.6% last month. Nevertheless, the number of unemployed has doubled by 160,000.

Agriculture is the mainstay of North Dakota's economy which

has enabled its unemployment rate to remain the lowest in the country.

Nevertheless, at 4.2% the rate is up from the 3.0% low as the number of

unemployed rose by one-quarter to 15,100 from last year. In Nebraska,

unemployment also remained low due to a large agriculture sector as

well as large education & health sectors.

Currently, the National Association of Business Economists forecasts 3.0% growth in the economy for 2010. That would result in little, if any, reduction in the unemployment rate since 3.0% barely exceeds the economy's growth potential. Some near-term boost to GDP growth could always occur due to a rebound in inventories, which have been depressed, or from heightened government spending, a sure bet. However, the more potent source for a quicker recovery would be consumer spending, but two factors suggest that a sustained boost is unlikely. For one, too much debt accumulation caused the savings rate to crater from 1980 through 2008. It only recently has edged higher. Secondly, the aging of the big-spending, baby-boom generation as a percent of the total has been underway for more than ten years and will continue. That means less force behind purchases of homes and consumer durables. Thus, relatively high unemployment rates seem likely for the foreseeable future.

The data used in this report can be found in Haver's EMPLR and USECON databases.

The long and large decline in state employment growth volatility from the Federal Reserve Bank of Philadelphia can be found here.

| Unemployment (%) | October | September | August | Oct. '08 | 2008 | 2007 | 2006 |

|---|---|---|---|---|---|---|---|

| Selected Highest States | |||||||

| Michigan | 15.1 | 15.3 | 15.2 | 9.1 | 8.4 | 7.1 | 6.9 |

| Nevada | 13.0 | 13.3 | 13.2 | 7.7 | 6.7 | 4.7 | 4.3 |

| California | 12.5 | 12.3 | 12.3 | 8.0 | 7.2 | 5.4 | 4.9 |

| South Carolina | 12.1 | 11.7 | 11.4 | 7.8 | 6.9 | 5.6 | 6.3 |

| Florida | 11.2 | 11.1 | 10.8 | 6.9 | 6.2 | 4.1 | 3.4 |

| Ohio | 10.5 | 10.1 | 10.8 | 6.9 | 6.5 | 5.6 | 5.4 |

| U.S. Average | 10.2 | 9.8 | 9.7 | 6.6 | 5.8 | 4.6 | 4.6 |

| Selected Lowest States | |||||||

| Indiana | 9.8 | 9.7 | 9.9 | 6.4 | 5.9 | 4.6 | 5.0 |

| Massachusetts | 8.9 | 9.3 | 9.1 | 5.8 | 5.3 | 4.5 | 4.8 |

| Texas | 8.3 | 8.2 | 8.0 | 5.3 | 4.9 | 4.4 | 5.0 |

| Maryland | 7.3 | 7.2 | 7.1 | 4.8 | 4.4 | 3.5 | 3.8 |

| Virginia | 6.6 | 6.6 | 6.6 | 4.3 | 4.0 | 3.0 | 3.0 |

| Nebraska | 4.9 | 4.9 | 5.0 | 3.6 | 3.3 | 3.0 | 3.0 |

| North Dakota | 4.2 | 4.1 | 4.3 | 3.2 | 3.1 | 3.1 | 3.2 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief