Global| Oct 31 2019

Global| Oct 31 2019A Halloween Potpourri of Weakness

Summary

China's manufacturing PMI dipped back below 50 in October. The manufacturing PMI has moved to exceptional weakness in 2019. In October, the manufacturing sector is contracting. The chart shows the abject weakness in manufacturing. The [...]

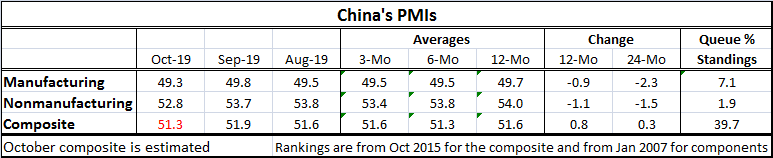

China's manufacturing PMI dipped back below 50 in October. The manufacturing PMI has moved to exceptional weakness in 2019. In October, the manufacturing sector is contracting. The chart shows the abject weakness in manufacturing. The table supplements the chart with data in nonmanufacturing. The table creates ranking statistics on the composite back to January 2015 and for the components manufacturing and nonmanufacturing to January 2007. All PMI queue rankings are below 50; the components ranked over a much longer horizon are especially weak. China is not doing well.

China's manufacturing PMI dipped back below 50 in October. The manufacturing PMI has moved to exceptional weakness in 2019. In October, the manufacturing sector is contracting. The chart shows the abject weakness in manufacturing. The table supplements the chart with data in nonmanufacturing. The table creates ranking statistics on the composite back to January 2015 and for the components manufacturing and nonmanufacturing to January 2007. All PMI queue rankings are below 50; the components ranked over a much longer horizon are especially weak. China is not doing well.

Missing the target on the only thing that matters with no remorse

Turning from China to Europe, the EMU region shows that EMU inflation is nowhere near 2% and moving away from it rapidly. The ECB has a single goal unlike the Fed whose objectives are split between growth and an inflation target. The ECB's sole mandate is to keep inflation a bit below the 2% mark. And we can see that it has kept inflation below 2% usually well below 2% since 2013. Still, some ECB members are bristling about the degree of accommodation the ECB has especially the adoption of negative interest rates. Clearly, some ECB members think the rate should be below 2% but close to it. Others seem content with almost any pace below 2% even though that is not the mandate. Not only is EMU inflation undershooting, but growth has been weak.

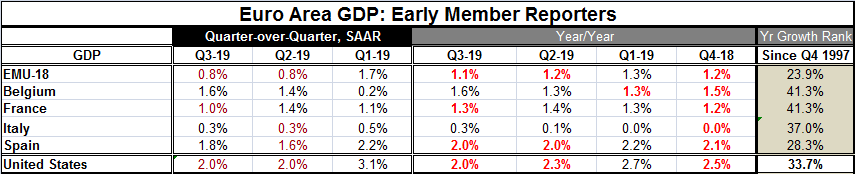

Today EMU GDP growth of Q3 was released and several members also have released their individual statistics. Growth in the EMU is at 0.8% (annualized) in Q3, the same as in Q2. Year-on-year growth is at 1.1%. The EMU 1.1% growth rate has a 23.9 percentile standing among all year-on-year growth rates since 1997. That ranking is well below its median. The median growth rate has a ranking at the 50th percentile.

Understanding growth rankings

Note that the ranking of growth rates is an individual country or regional concept. For comparison, I include the United States in the table. Q3 U.S. growth is up at a 2% pace year-on-year in Q3. And that pace has a 33.7 percentile ranking for the U.S. Note that the U.S. growth rate is substantially stronger than the pace of French growth (2% vs. 1.3%). Yet, the French rank standing is above the U.S. standing (41.3% vs. 33.7%). This is statement about how much stronger U.S. growth has been, compared to French growth over the ranking period back to 1997.

EMU growth

While only four EMU members have reported their GDP, three of them are among the EMU's four largest economies. None have percentile standings above their respective medians for this period. France, the second largest EMU member, has a 41.3 percentile standing. Italy, the third largest EMU economy, has a 0.3% year-on-year GDP rise and that has a 37.0 percentile standing. Both of those figures for Italy are shocking. It is shocking that Italy's four-quarter growth rate is only 0.3% and more shocking that that such a low growth rate has a standing as high as its 37th percentile! Since 1997, thirty-seven percent of Italy's year-on-year growth rates have been at or below 0.3%. That, is a testament to how weak the Italian economy has been especially since the Great Recession and financial crisis as it has borne the yoke of austerity with great weight. Spain grew at a 2% pace year-on-year in Q3 and that pace has a 28.3 percentile standing. Belgium, a smaller economy, has a 1.6% year-on-year growth rate that carries a 41.3 percentile standing.

State of the global economy

Data from China to Europe and on inflation underscore the ongoing global weakness. These data also underscore why the Federal Reserve in the U.S. acted to cut rates in its meeting yesterday; the global environment is still chilling. Central banks have done just about all that they can – and maybe even more than they should- and still growth is not clearly restarting. The trade war is taking a toll on China, but China's slowdown is multi-dimensional encompassing the services sector and the goods sector. China has tried to fight off the growth-depressing effects of the trade war using debt to stimulate activity. But the effectiveness of debt to stimulate growth has been blunted. When the trade war is done, there will again be trade deflecting competition from China, the country that is the original source of a lot of this global dislocation.

Global economy on thin ice

The global economy is not crashing into recession. But there are significant issues and risks that could either be surmounted or that could bring on recession. Hong Kong's political protesting has helped to push that country to its first recession in a decade. U.K. growth is also weak with recent reports on reduced auto production and dropping consumer confidence are testament to the impact of Brexit uncertainty. The U.K. is trying to decide if it has a love or hate relationship with Brexit. Japan has issued some mixed reports as industrial production rebounded and consumer confidence edged up (from a very low reading); Japan housing starts fell. Recent U.S. data revealed weak U.S. income and spending reports in September with an October PMI reading for the Chicago area that was chillingly weak. None of this says slippage into recession and yet nothing says that growth or economic conditions are back to anything like normal. Apart from economic risks, geopolitical risks of various sorts continue to swirl…

Is the U.S. still the trusted center for growth?

U.S. employment data for October due out Friday will be weakened by the GM strike. But apart from that, job growth has been slowing and wages have not continued to accelerate in the U.S. Moreover, the quality of U.S. job creation has not been ‘good.' These economic conditions are woven into the fabric of the U.S. political discourse in an environment that has just become decidedly more hostile as the U.S. House of Representative did finally take a vote and define some of the terms its will employ to consider the impeachment of President Donald Trump. The vote, however, was wholly on partisan lines a fact that makes the act look more like a political stunt than a real needed investigation of presidential wrong-doing. If you can't get members to cross the aisle to take up an impeachment hearing, that is not a bipartisan effort and it begins to look like a concocted trial. Then there is the fact the Republicans hold a decisive majority in the Senate where an impeachment trial would be held and decided. The prospect of removing Mr. Trump is extremely remote and that begs the question of what the House is really up to? Are they just trying to sully his name ahead of U.S. elections due up in one year's time? It sends all the wrong signals overseas about the U.S. All of this undermines U.S. credibility. It will impair the conduct of U.S. foreign policy to some degree. It will impact the President's standing and affect his ability to govern and to interact with foreign leaders. All of this matters.

As we look ahead, there are a lot of clouds, a lot of risks and yet policymakers still do not have much ammunition to use if economic conditions deteriorate. While some object to the conditions of super stimulus in monetary policy, what is the alternative? Do we really think that this is the time to try to undo ‘excessive stimulus,' to paste the peeled layers back onto the onion? I doubt that would be productive. The die has been cast.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief