Global| Mar 09 2006

Global| Mar 09 20064Q Debt Fueled By Government Budget Deficit, 2005 By the Consumer

by:Tom Moeller

|in:Economy in Brief

Summary

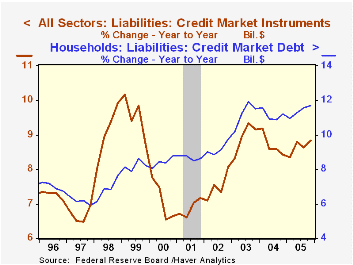

Growth in total credit market debt outstanding surged 11.4% (AR) last quarter. Faster growth rates often occur during 4Q but that was the quickest since 2002. The acceleration from 3Q was due to a jump in Federal Government borrowing [...]

Growth in total credit market debt outstanding surged 11.4% (AR) last quarter. Faster growth rates often occur during 4Q but that was the quickest since 2002.

The acceleration from 3Q was due to a jump in Federal Government borrowing at a 10.1% rate (7.0% y/y) versus 6.6% in 3Q.

Growth in household sector borrowing continued strong at a 13.2% rate. That was down from the heated pace of the prior quarter but it capped off the fastest yearly rate of household sector borrowing on record by edging out the 11.5% rate of growth during 2003.

Home mortgage obligations grew at a 14.6% rate (14.1% y/y) last quarter capping the fourth consecutive year of double digit growth. Consumer credit growth slowed substantially to a 4.7% rate from 8.5% during 3Q and the 2.9% yearly rate of growth was the slowest since 1992, likely reflecting mortgage refinancings.

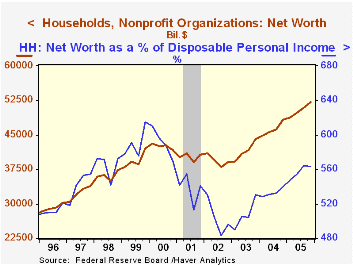

Household sector asset values rose at a 9.8% annual rate (8.5% y/y) during 4Q powered by a 14.0% (14.9% y/y) rise in the value of real estate holdings. Financial asset values rose 8.0% (5.6% y/y) due to an 11.2% (12.9% y/y) rise in the value of mutual fund shares but the value of corporate equities held directly fell 4.4% (-5.0% y/y).

The net worth of the US household sector in 4Q improved 2.3% (8.0% y/y) to a record $52.107 trillion. The gain, however, did not lift net worth as a percentage of income which fell slightly q/q to a still high 5.635 times income. During 2004 that ratio was 5.403 times.

| Flow of Funds | % of Total | 4Q 05 (AR) |

3Q 05 (AR) |

Y/Y | 2005 | 2004 | 2003 |

|---|---|---|---|---|---|---|---|

| Total Credit Market Debt Outstanding | 11.4% | 8.1% | 8.8% | 8.8% | 8.4% | 9.2% | |

| Federal Government | 12% | 10.1% | 6.6% | 7.0% | 7.0% | 9.0% | 10.9% |

| Households | 28% | 13.2% | 14.3% | 11.7% | 11.7% | 11.2% | 11.5% |

| Nonfinancial Corporate Business | 14% | 7.0% | 4.4% | 5.7% | 5.7% | 3.6% | 2.2% |

| Financial Sectors | 32% | 11.9% | 3.4% | 7.5% | 7.5% | 7.6% | 10.1% |

| Net Worth: Households & Nonprofit Organizations (Trillions) | -- | $52.107 | $50.957 | -- | $52.107 | $48.250 | $44.127 |

| Tangible Assets | -- | $25.558 | $24.816 | 13.3% | $25.558 | $22.556 | $20.040 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief