UK Sales Values Increase as Volumes Implode

UK nominal sales and sale volume trends create completely different pictures of reality. But surveys join the volume data in seeing pronounced weakness and even the potential for a gathering storm.

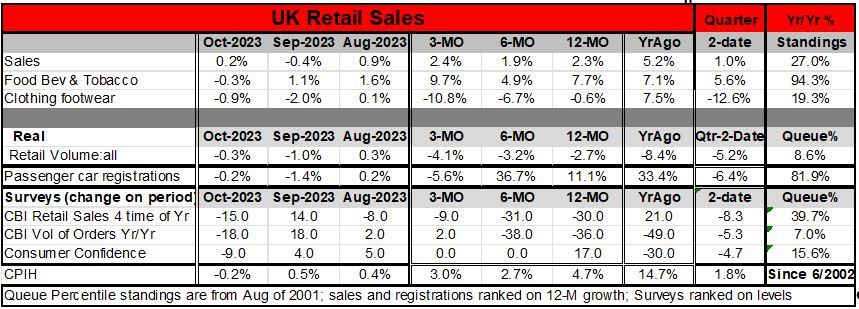

Volume vs value assessments - UK sales values increased by 0.2% in October, but sales volumes fell at the same time; sales volumes have fallen for two-months in a row by -0.3% in October and by -1% in September. Nominal retail sales increased by 2.3% over 12-months and are expanding at a 2.4% annual rate over 3-months, giving the appearance of steady, if somewhat slow, expansion in sales. But retail sales volumes, adjusted for the effects of inflation, show declines of 2.7% over 12-months and a decline at a 3.2% annual rate over 6-months followed by a decline at a 4.1% annual rate over 3-months. Sales volumes are contracting, and the degree of contraction is growing over more recent periods.

Quarter-to-date - Similarly on the quarter-to-date, nominal retail sales show a 1% increase as sales volumes are contracting at a 5.2% annual rate.

Turn signals from autos? - Passenger car registrations have fallen for two months in a row, falling by 0.2% in October and by 1.4% in September. The progression of passenger sales registration shows a rise of 11% over 12-months, that accelerates to a very strong 36.7% annual rate over 6-months but then registrations weaken and fall at a 5.6% annual rate over 3-months. In the quarter-to-date passenger car registrations are falling at a 6.4% annual rate.

Survey results: the CBI

UK surveys on retail sales provide some additional perspective on how sales are performing and how merchants tend to view sales trends.

-The Confederation of British Industry (CBI) shows retail sales for the time of year falling to a -15 index reading from a + 14 in September. The progression of changes for sales shows a decline of 30 points over 12-months, a decline of 31 points over 6-months, and a decline of 9-points over 3-months. Retail sales for the ‘time of year’ declined by 8 points in October compared to their Q3 average; their October value has a 39.7 percentile standing in its historic queue of responses. On balance these are weak retail signals.

-The CBI assessment of the volume of orders judging from year-on-year growth rates, plunges to a minus 18 response from plus 18 in September. However, the progression of changes shows this order metric lower by 36 points over 12-months and lower by 38 points over 6-months then higher by 2-points over three months.

Consumer Confidence - Consumer confidence (also plotted on the chart above) drops to -9 in October from +4 in September. Consumer confidence has been flat, over 3-months and 6-months but is up by 17 points over 12-months. Still, confidence is lower by 4.7 points in October compared to the Q3 average. And its queue standing is in the 15th percentile of its historic queue of results, quite weak.

Conclusion: Weak! Weak is the bottom line on UK retail sales in October. The nominal signals are copacetic but misleading. Passenger car registrations have a high queue standing in their 81st percentile but show some near-term weakening. Food and beverage spending is holding to high ground as well. But overall nominal sales, and total sales volumes, the CBI metrics, as well as consumer confidence, all score extremely weak readings. Fortunately, inflation in the UK is turning lower - still excessive - but moving in the 'right' direction. Still, there will be no 'relief' from monetary policy anytime soon and, in the meantime, retailing is weakening.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Global

Global