U.K. CPIH Inflation: Stable and Excessive

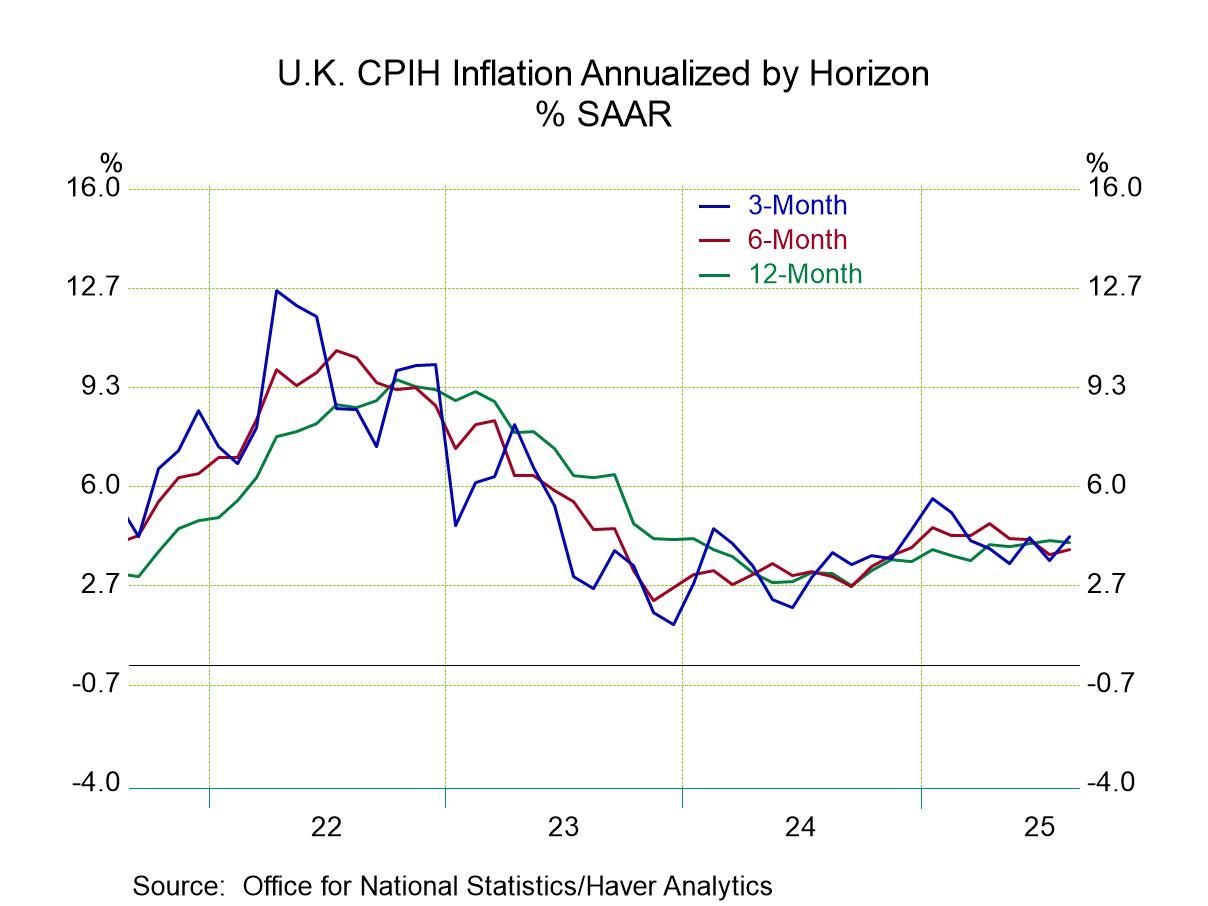

Inflation in the United Kingdom in August rose by 0.3% on the CPIH measure; excluding food, alcohol, energy, and tobacco (core), the increase was a milder 0.2%. Headline inflation in the U.K. runs at a 4.3% annual pace over three months; the core measure runs at a 3.6% annual rate pace, a bit weaker but still over the top of the U.K. 2% target.

Sequential trends: Sequential inflation in the U.K. is stubborn at 4.1% over 12 months, at a 3.9% annual rate over six months, and at 4.3% an annual rate over three months - a pace that is consistent, steady, and excessive. Core inflation runs at 4% over 12 months, edges down to a 3.6% annual rate over six months and stays at 3.6% over three months - still relatively steady and excessive but with a hint of progress.

Inflation monthly: In August among the 10 detailed categories, inflation accelerated in five of them, in July it also accelerated in five of them, and in June there was an acceleration in four of them. Diffusion calculations show that the tendency for inflation to accelerate across categories, the headline and core has been slightly below the 50% mark making inflation slightly disinflationary.

Sequential diffusion: Sequentially diffusion has been behaving better, with 12-month inflation higher than 12-month-ago inflation by a slight margin with the diffusion reading of 54.5%. However, over 6 months comparing inflation to 12-months across categories, diffusion is only 45.5%, and over 3 months comparing inflation to inflation over 6 months, the diffusion calculation steps down to 36.4%. When diffusion is above 50%, inflation is accelerating in more categories than it is decelerating; when it's below 50%, inflation is showing more deceleration than it is acceleration. These diffusion calculations are encouraging, although they are only indications of breadth not of importance because they just compare across categories and they are executed without weighting. The headline and the core measures bring weighting into play, and we see the impact of that by comparing those measures sequentially. Still, diffusion is an interesting measure on its own because it helps to show how widespread pressures are.

U.K. unemployment- At the same time, that inflation has been stubborn. The unemployment rate in the U.K. has gradually been creeping up. The U.K. claimant rate of unemployment, which is just a little bit more topical, has been slightly more stable sequentially than the overall unemployment rate and in June and July that rate of unemployment gauge edged slightly lower. However, it's a different concept than for overall unemployment although the two readings are similar in terms of their levels when ranked over the same. They're very different with the unemployment ranking through June 2025 at 34.5% while the June claimant unemployment rate ranking is high relative to its historic experience at its 75.3 percentile - much higher.

Summing up Both the headline and core CPI measures were last below 2% in July 2021 and that previous episode of moderate inflation had lasted for a relatively long period of time. However, now, the overshoot has lasted for a long period of time -over four years- and it's occurring at a time when economic growth has been less than robust. This puts the Bank of England at a difficult spot at a time when there's also a great deal of political pressure in play in the United Kingdom.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief