German PPI Shows Ongoing Release of Inflation Pressure

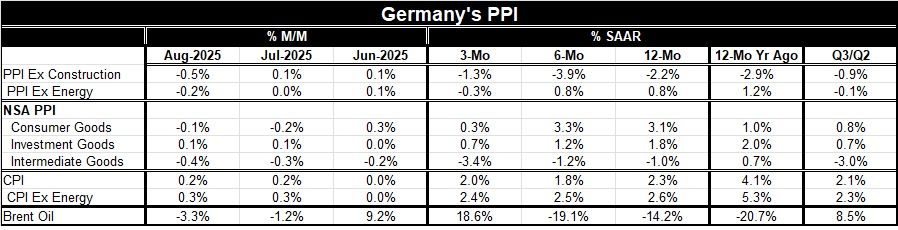

The German PPI report showed a drop of 0.5% in the August headline, continuing a string of inflation data on the producer price front that is laying a solid disinflationary trend for the German economy. The PPI rose by 0.1% in July and in June. Sequentially the PPI falls 2.2% over 12 months, falls at 3.9% annual rate over six months, and falls at a 1.3% annual rate over three months, an impressive record of inflation discipline at a time that consumer inflation has been running hot globally.

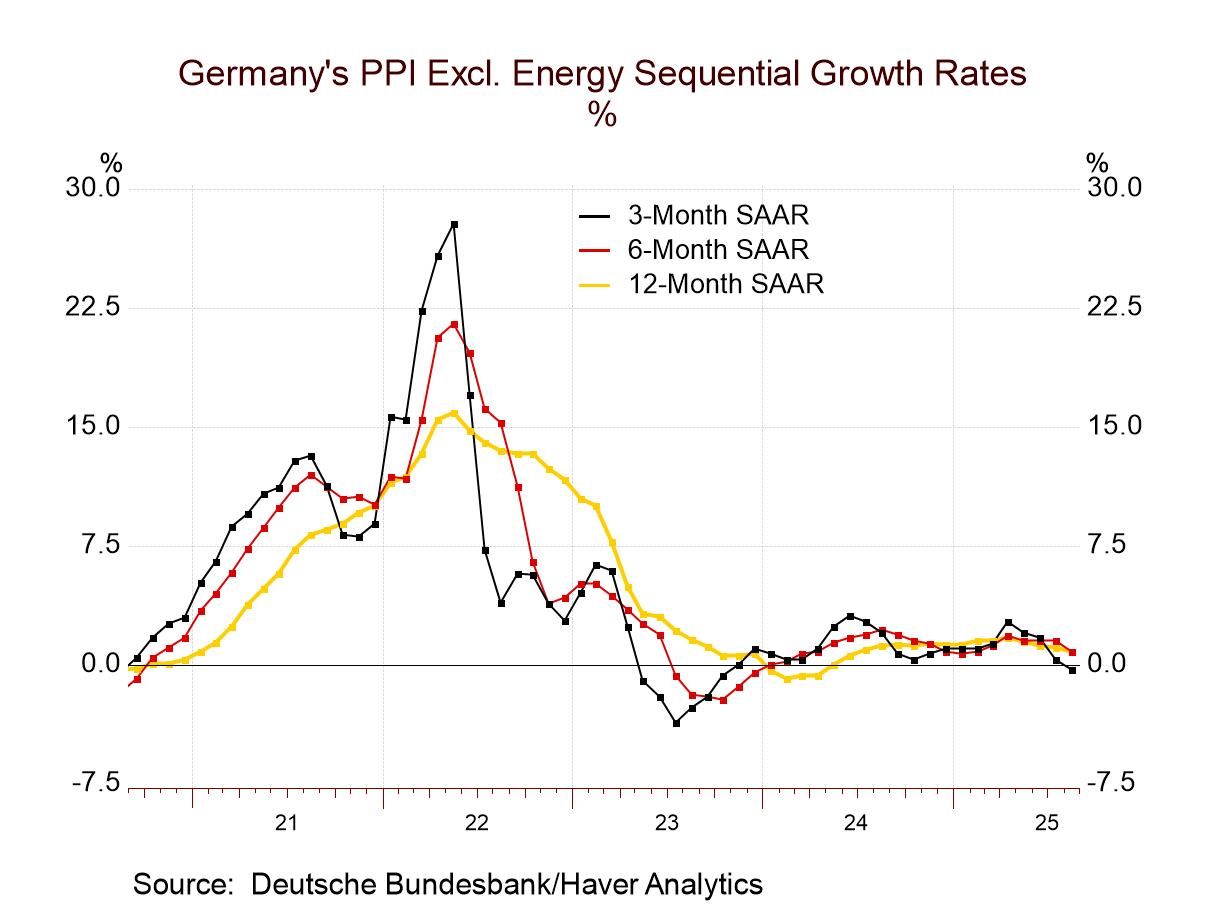

Germany's PPI excluding energy also fell in August, dropping by 0.2% on the month after being flat in July and rising 0.1% in June. The PPI excluding energy for Germany rises 0.8% over 12 months, rises at a 0.8% annual rate over six months, and falls at a 0.3% annual rate over three months. The inflation discipline extends past energy; it is not simply disciplined energy prices although that has been part of the story.

Sectoral German PPI data are not seasonally adjusted making their sequential patterns a little bit less dependable. However, sequentially German consumer prices show inflation has been dropping, the same is true for investment goods, whereas for intermediate goods, not only is inflation dropping but prices are dropping too; inflation is negative over 12 months, six months and three months with the 3-month drop in intermediate prices at a -3.4% annual rate.

The behavior of producer prices compares to modest results on the CPI front where, sequentially, the German CPI rose 2.3% over 12 months, at a 1.8% pace over six months, and then at a 2% pace over three months, all well-contained changes. The CPI excluding energy rose by 2.6% over 12 months, 2.5% over six months, and 2.4% over three months showing a very slight deceleration with inflation looking still very sticky at about 1/2 of a percentage point above what is the target pace set by the ECB for the European Monetary Union as a whole.

The global picture and risk The inflation picture globally continues to be on the sticky side and now the Federal Reserve appears to be about to lead a new trend in central bank interest rates lower. To understand this, I think you really have to have Fed technician in your bloodstream and have to have completely drunk and enjoyed the Fed Kool-Aid pertaining to the concept of R-Star. R-Star holds that the equilibrium Fed funds rate is extremely low and therefore that the current federal funds rate is too high and that there's room for the Fed to cut interest rates. The problem with the R-Star measure is that it is not robust and in addition to that the U.S. economy has not been acting like the Fed funds rate is far too high. As an example, the Atlanta Fed's GDP-Now report for the third quarter is looking for 3.3% real GDP growth in the United States. Meanwhile, all of the talk and concern about Trump tariffs and the uncertainty that's created and how that's interrupted growth is still in play and the economy is still producing this kind of growth -as well as stock market performance. Retail sales are still relatively strong. Moreover, inflation is still over target and creeping higher and so, you know, excuse me, if I have a hard time sipping that Kool-Aid on R-Star.

Time will tell whether the Fed and the economists were right. Frankly when I take a trip in the car, I love to take my cue from GPS, and to follow the signals, but I also like to look at the road signs to see if they're telling me I'm headed in the right direction. Right now, we have a case where the Fed’s GPS is telling us to go one way, but the road signs seem to tell us that we're winding up in a place we don't want to be. We'll see if this Fed leadership spreads and if globally central banks begin to follow the Fed into these rate reductions. Then, time will tell whether it's the right thing to do or not.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Global

Global