Global| Jan 24 2022

Global| Jan 24 2022Flash PMIs...Flash in the Pan?

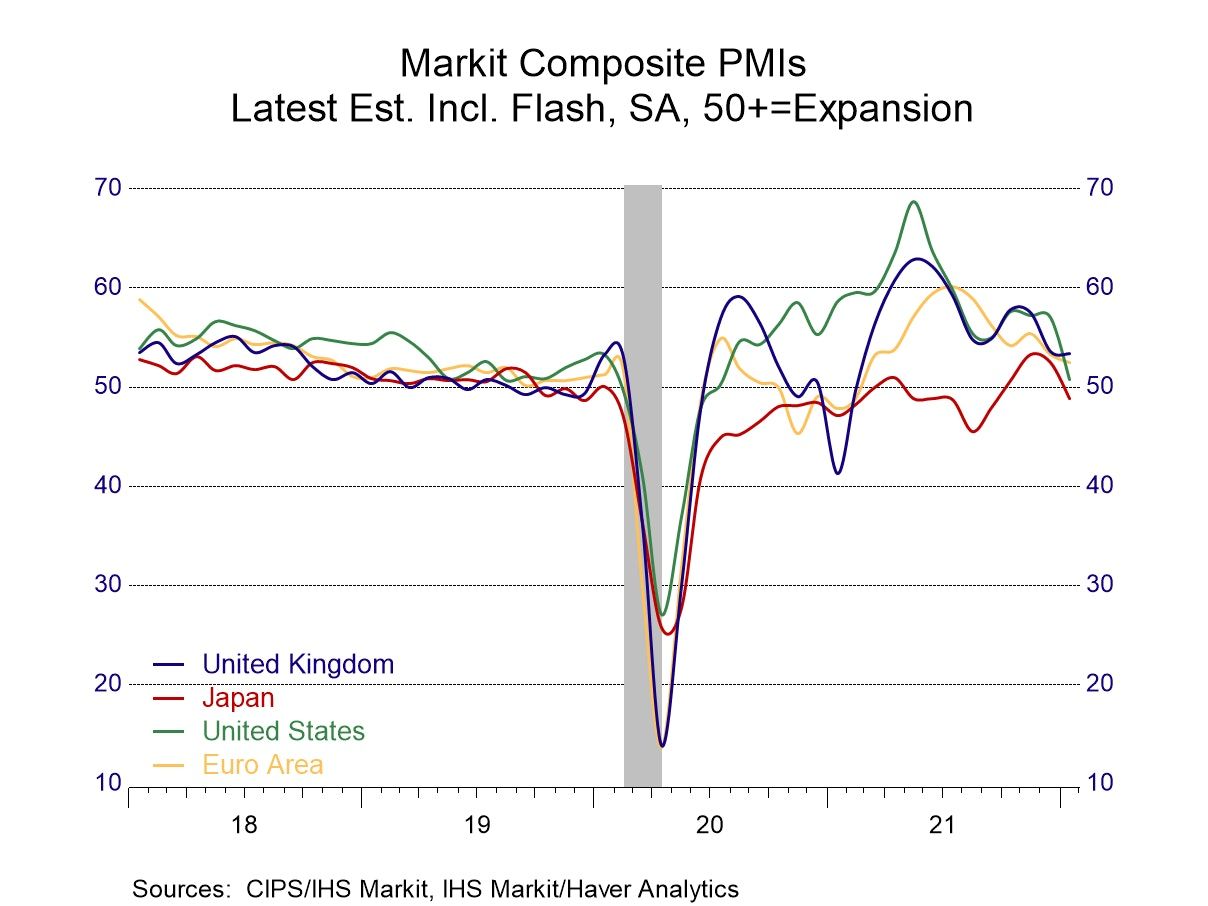

Markit PMI flash readings from Markit for January 2022 weakened broadly. The clear exception was Germany where the composite, manufacturing and services readings all bucked the trend to make solid to strong month-to-month gains. Maybe there are additives in the gas in the pipeline from Russia? Or simply catch up since Germany's PMI standings are not standouts. The German gains were strong enough for an improvement in the manufacturing reading to post for all of the EMU due to Germany's large weight in that index. However, the EMU composite and services PMIs weakened.

France, the U.K., and the U.S. saw broad declines with each of the Markit indexes falling on the month. Japan witnesses a small gain in manufacturing with a sizeable fall in services and a step back in the composite. The U.S. fared the worst of all with a large setback in services to couple with a significant setback in manufacturing that produced a much weaker composite as well. The U.S. services drop is the third largest in the past four years and is exceeded only by the spectacular drops logged when Covid struck.

The U.S. is not only the weakest on the month; it is also riding three consecutive months of three sector deterioration and is alone among these reports with that distinction (and U.S. manufacturing extends that to weaken month-to-month for six months in a row). France weakened in all sectors for two months running while the U.K., Japan, and the EMU weakened in five of six month-to month-comparisons over the last two months. While Germany made across the board sector gains in January, it weakened across the board in December.

The monthly data, except for Germany, show a weakening as the color-coded back 'stronger' entries give way to the 'weaker' red entries in recent months. The historic averages which are formed excluding January (e.g., the three-month average is December, November, and October) show (1) predominate weakening over three months, (2) mixed conditions over six months, and (3) those contrast with uniform strength and improvement over 12 months (that is 12-months compared to the 12-month average of 12-months ago).

There are clear country differences as well, however. The U.S. is the only entry in the table with three- sectors weakening over three months as well as over six months. However, all the other members, except Japan, show three-month and six-month weakening for manufacturing alone.

The index standings- both the high-low position and the rank or queue standings show less strength than there has been recently as only Japan has ranking for its manufacturing sector in the 90th percentile decile. In the high-low range the EMU, Germany, and France mount 80th percentile decile standings, the U.K. has a low 70s standing, and the U.S. is just below a 70th percentile standing in manufacturing in the high-low column.

However, the queue percentile standings show less strength indicating that current performance does not stand up well to the standards of the past four years. Manufacturing is an exception with 80th percentile standing in the EMU, Germany, and France with the U.K. in the upper 70th queue percentile range and Japan again in its 90th percentile. The is U.S. alone below its median with a 49-percentile queue standing. The real weakness comes from services where four of the six entries in the table (the EMU, Germany, Japan, and the U.S.) log queue percentile standings for services that are below their respective medians and in most cases below by quite large margin. France and the U.K. are the exceptions here but only with queue rankings in their respective 50th percentile decile range.

This performance is the clear mark of the virus. As manufacturing, for the most part, has held much of its strength and resilience while the rapid spread of Omicron has taken a large bite out of activity in the service sector globally. The U.S. and Japan have been hit exceptionally hard looking at the queue standing assessments.

Services have been hit so hard recently that among the six reporters in this table four of them have service sector readings that stand below their pre-Covid readings of January 2020. The two exceptions have little to brag about since the U.K. is higher than its January 2020 level by only 0.4 points in services, while France is higher by 1.4 points. That's not much gain over a 24-month period.

Average manufacturing standings for this group are at the 79th queue percentile in manufacturing but only at the 36th percentile for services which is the jobs sector. The composite index averages a standing in its 46.6 queue percentile below its median.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief