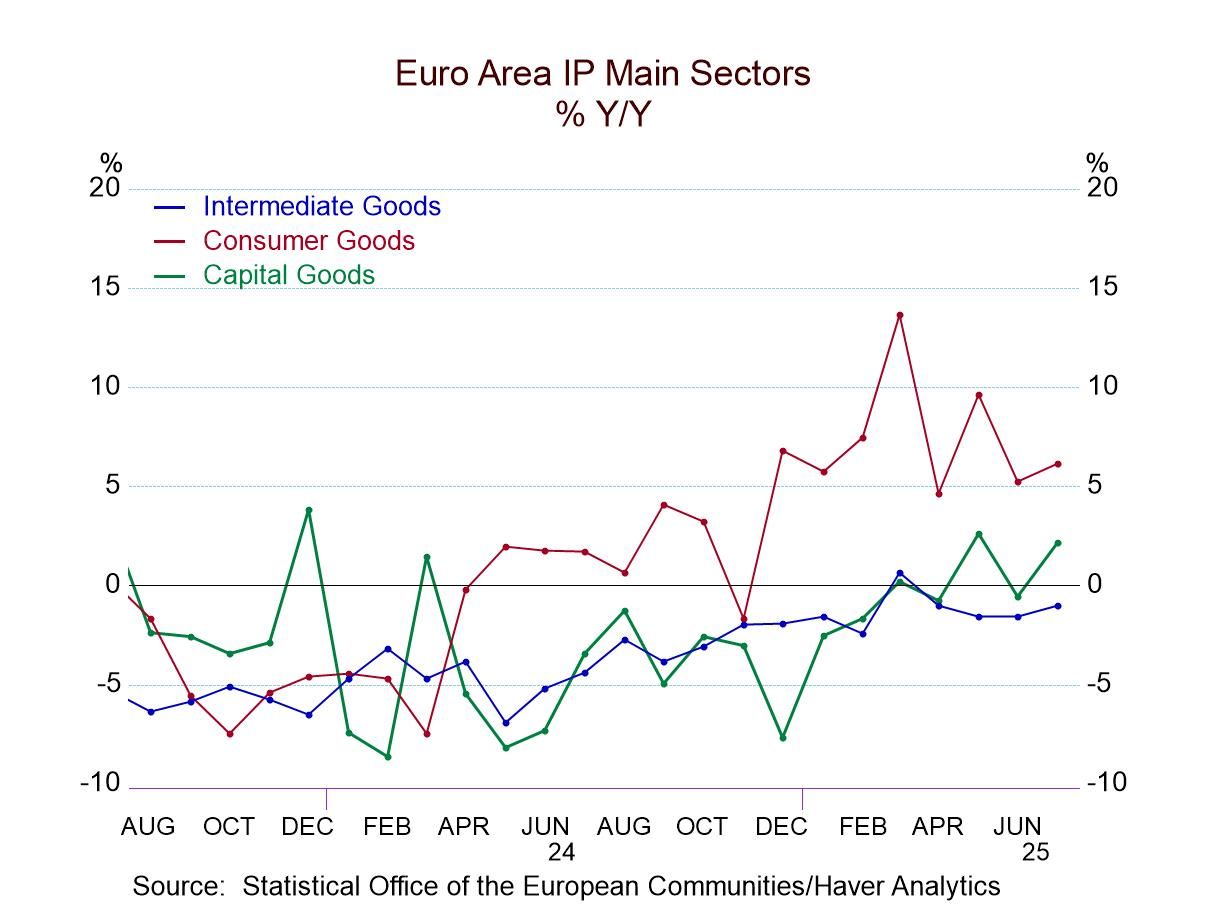

Finalized EMU IP Shows More Strength

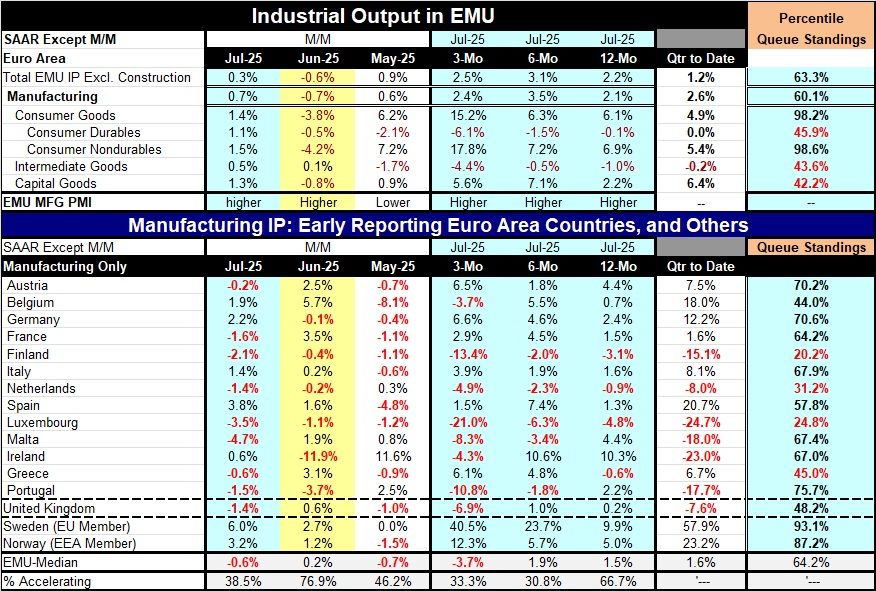

The finalized version for EMU industrial production in the European Monetary Union in July showed that much better than preliminary data had suggested. Overall output rose 0.3% in July, but output in manufacturing on the month rose by 0.7%. Consumer goods output rose by 1.4% on the month with consumer durables output up by 1.1% and nondurables output up by 1.5%. Intermediate goods output rose by 0.5% with capital goods output rising by 1.3%. All of these are very solid numbers.

The median result for reporting European Monetary Union members had shown a decline of 0.6% for manufacturing output. And, of course, the problem with that is that it's a median among countries without weights being applied to account for size. Germany, for example, showed an increase in output in July of 2.2% in its manufacturing sector, France showed a decline of 1.6%, Italy showed an increase of 1.4%, with Spain showing a rise of 3.8%. That's three of the largest 4 monetary union members showing solid increases in output.

Sequential data showed that output is holding up quite nicely with growth 2.2% over 12 months, up 3.1% at an annual rate over six months and up by 2.5% in an annual rate over three months. For manufacturing, the results are roughly the same, with a 2.1% gain over 12 months, 3.5% annualized over six months and 2.4% annualized over three months.

The quarter-to-date numbers showed that output is developing nicely in the third quarter with overall output up at a 1.2% annual rate as of July, the first month in the quarter with that growth rate representing annualized growth in July over the second quarter average; manufacturing output on the same basis is up at a 2.6% annual rate. All the sector growth rates are positive as well QTD except for intermediate goods.

Percentile queue standings rank current growth rates among past historic growth rates (back to 2007) and on this basis, overall production growth has a 63.3 percentile rank, manufacturing has a 60.1 percentile rank, consumer goods IP is extremely strong with a 98.2 percentile rank, pushed ahead by nondurables that have a 98-percentile rank. Consumer IP growth is held back somewhat by consumer durables that have only a 45.9 percentile ranking, below its median for the previous period. Intermediate goods and capital goods also have below-median rankings (rankings below 50%) at the 43.6 percentile for intermediate goods and 42.2 percentile for capital goods. Still, none of the sectors is particularly weak; being at the 42nd percentile or better means that the shortfall from the median is not extreme and the weighted average for overall production and for manufacturing still stands in its 60th percentile or better.

As we look down the column to look at country-specific manufacturing readings, we find that there are only 4 of 13 reporting monetary union members with manufacturing output below its median in July. And those countries are Finland, the Netherlands, Luxembourg, and Greece, all moderate to small-sized economies.

On balance, the performance the monetary union output in July is quite solid. And these readings are joined by an August reading for IP in the United States that showed a surprising positive turn on the month. It's too soon to say that conditions globally are improving faster or more than had been expected; however, there is a whiff of that in the air despite some sour readings on job growth in the United States.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Global

Global