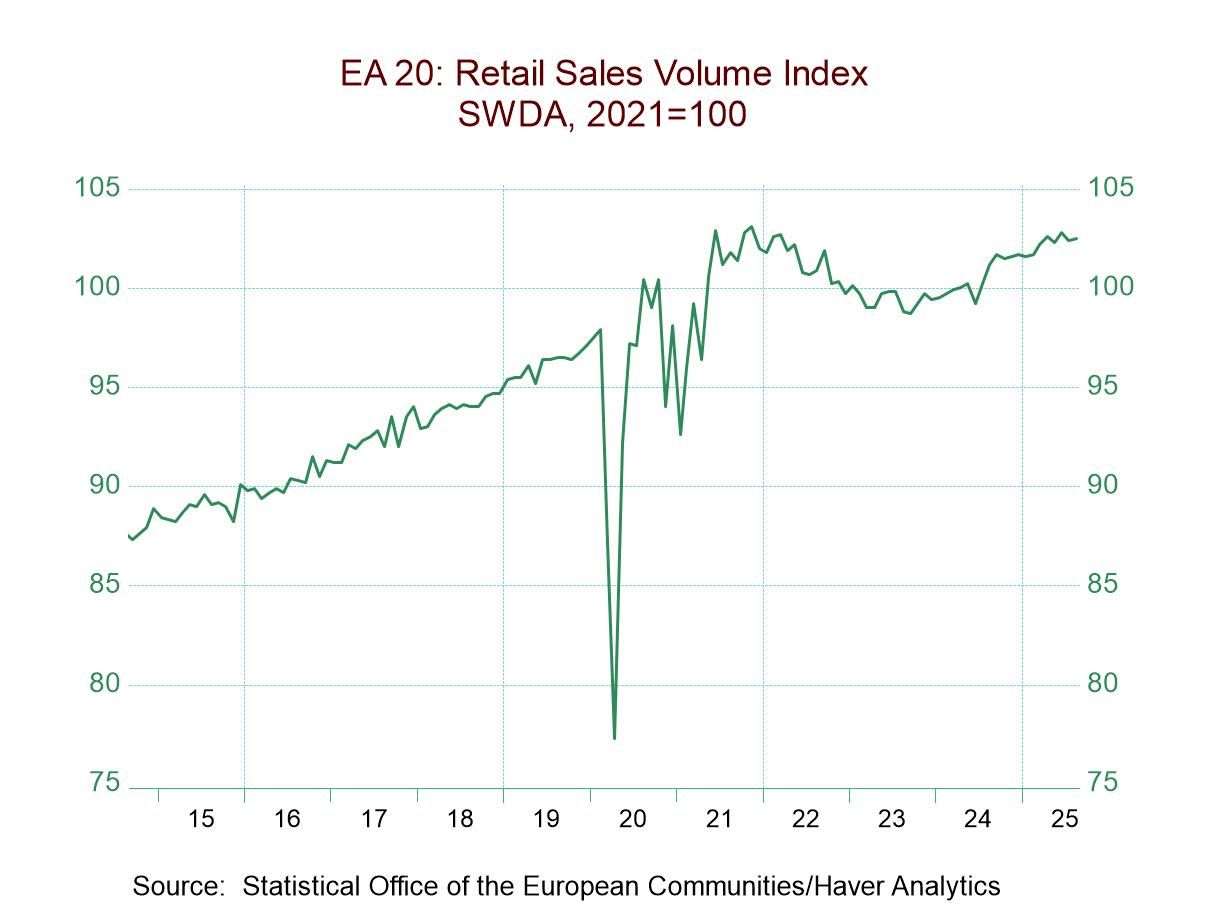

EMU Retail Sales Show Unevenness

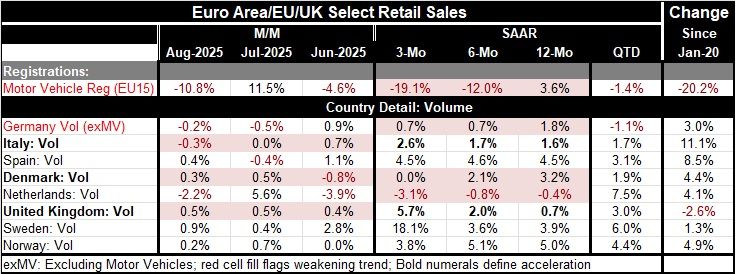

Motor vehicle registrations fell sharply in August, dropping 10.8% after rising 11.5% in July, which had followed a 4.6% drop in June. This sort of ragged action in monthly activity is not really very unusual. It's characteristic of the auto market; however, if we look at the sequential data in the table, we see motor vehicle registrations up 3.6% over 12 months, falling at a 12% annual rate over six months, and then falling at 19.1% annual rate over three months, clearly an escalating pattern of weakness that is hidden by the monthly volatility.

Aggregate sales for the monetary union are not available yet; however, we have sales for eight key European countries. Not all of them members of the monetary union. Still, they tell a story.

We see in August sales dropped month-to-month in Germany and Italy and the Netherlands; sales rose in the other five reporting countries. There was repeat fall for Germany since sales also fell in July month-to-month; sales had fallen in two countries in July, the drop in Spain was reversed by an August gain. Italy, that has seen a drop in August, had flat sales in July. But only two countries had clear net declines in sales for July and August combined. In June, sales dropped in Denmark and the Netherland, while they turned up flat in Norway; sales grew in the other reporting countries.

We can recalibrate by looking at the sequential growth rates from 12-months, six-months, and three-months. On that basis, we see that there is weakness in play for Germany, Denmark, and the Netherlands over this span. Only Italy shows sales volumes are steadily expanding at an increasingly more rapid rate. Technically Spain is not on the list of countries showing acceleration, but Spain is showing growth of 4.5% or 4.6% in each one of these periods, a very steady and solid result. Sweden also fails the ‘every period improvement test’; however, its 3.9% growth over 12 months with growth down only to 3.6% over six months that explodes to an 18.1% annual rate over three months is clearly a candidate for a country that is percolating and doing better.

Quarter-to-date we've seen that motor vehicle registrations are falling at a 1.4% annual rate. But retail sales QTD are as strong as 7.5% in an annual rate in the Netherlands and 6% in Sweden. With the weakest result, apart from Germany's decline, there’s a gain of 1.7% at an annual rate in Italy. These data, through August, are for two months into the new quarter.

We also made the comparison of sales gains since COVID struck. On that basis, we see that motor vehicle registrations have fallen from their level in January 2020 by 20.2%. U.K. sales are contracting, falling by 2.6% in this lengthy period. Over this period, the U.K. conducted its operation Brexit in which it exited its membership from the European Union. As you can see, they paid a price for the exit- the weakest sales in this group and the only net decline. In Italy, sales are up very strongly at 11.1%, in Spain at 8.5%. After that, sales rates are clustered around net growth rates of 4 or 5% or slightly weaker; since we're looking at a 5 ½ year period, these sales translate into real consumer spending of less than 1% per year.

The graphic on retail sales shows that there's not a great deal of momentum for sales. We can see from the growth statistics of the individual countries in the table where three of the countries in the sample showing ongoing sales decelerations against only one with a clear acceleration.

Manufacturing has been flirting with its own expansion-contraction line showing weak numbers in the PMI surveys that have hovered above and below the key level of ‘50’ which is the expansion/contraction dividing line. And then post-Covid growth has been nursed back to health without insisting that interest rates move up to drive inflation back down to target.

However, Europe is also on the doorstep of a war involving the Ukraine-Russia was in full swing with new flirtation or incursions over NATO members by Russia…will that mushroom? As it stands, there is no clear path to resolution.

Policies globally are still being watched; see what the next move is for central banks now that an easing cycle gas has been engaged at the Fed in the U.S. However, using its own basic metrics <Taylor Rule; R-Star>, the Fed doesn't seem to have a lot of room to continue to cut interest rates even though the President endorses more cuts and lower rates. However, this policy path seems to be getting ingrained in markets prematurely.

The recent retail sales in the U.K. on paper show few concerns. But at the Bank of England, there is talk that a more aggressively stimulative monetary policy is going to be needed to deal with emerging weakness that has been showing its hand.

Contrarily, events in the U.S. are made more complicated to disentangle since a failure to lift the agreement to set spending standards for the federal government has stuck federal spending in nominal terms. We can now see what the future holds and we'll see how the economies deal with that and what it is clearly a lot more uncertainty.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief

Global

Global