Asia| Sep 29 2025

Asia| Sep 29 2025Economic Letter from Asia: Tariff Medicine

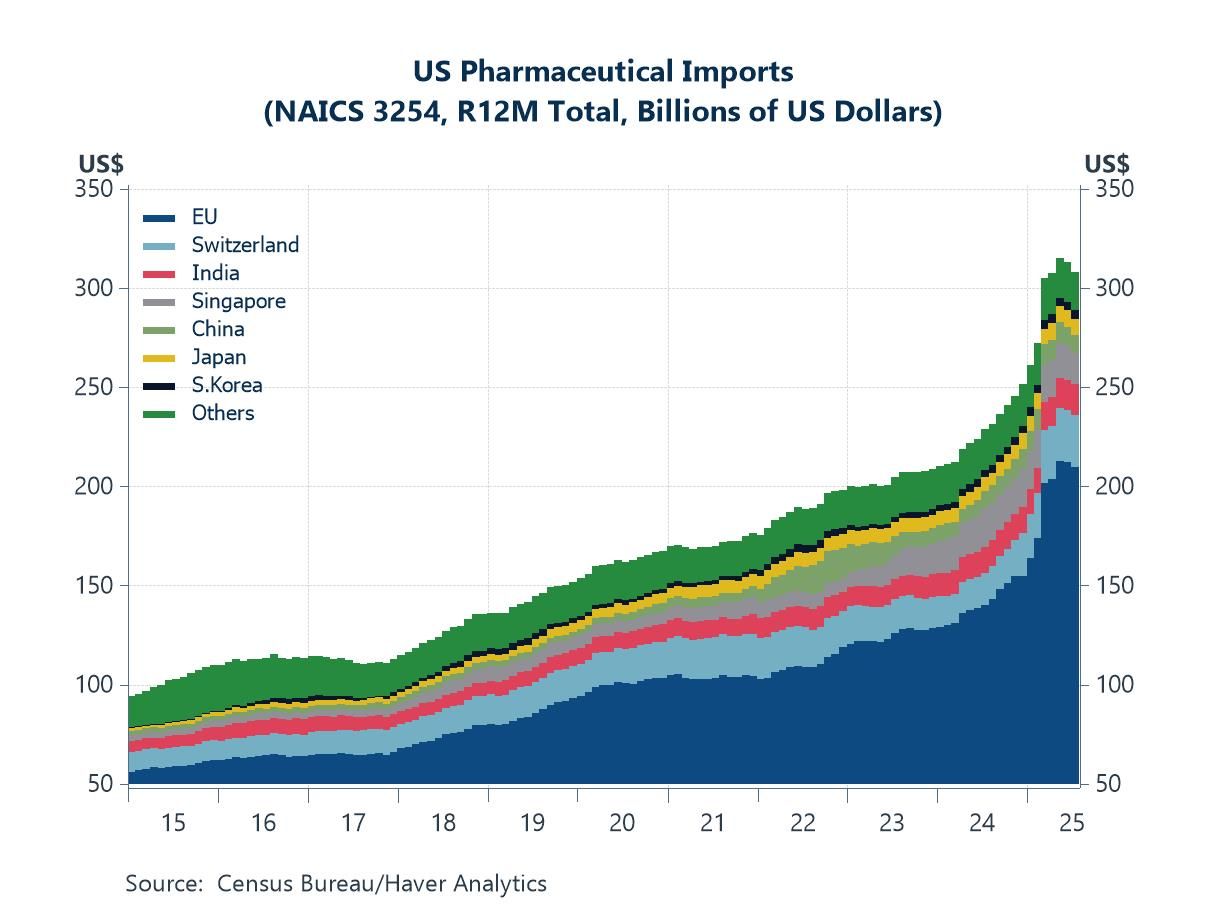

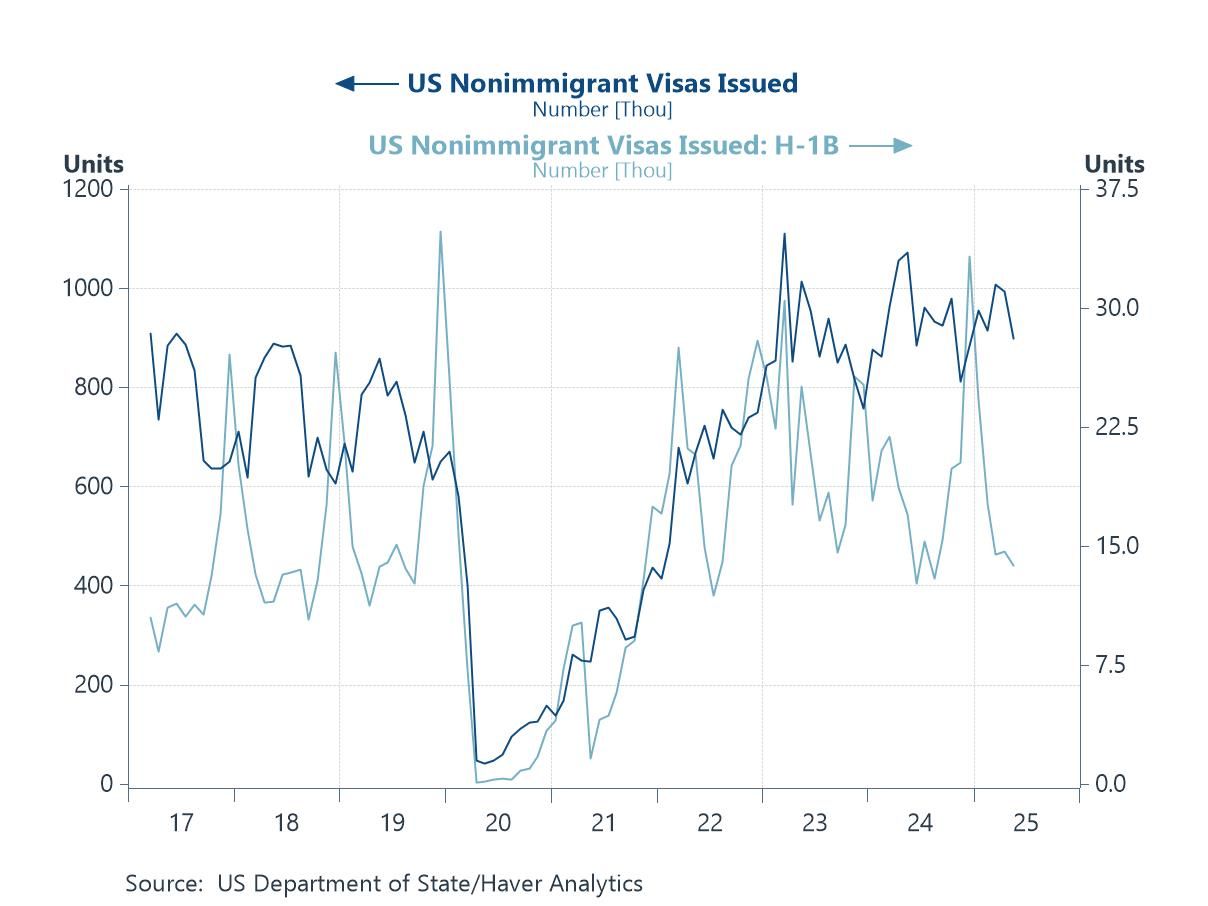

This week, we examine the recent flurry of global trade developments and their potential impact on Asia. The previous multi-week tariff calm proved short-lived after US President Trump announced 100% tariffs on branded and patented pharmaceutical products last week. A point of relief lies in the exemption of economies such as the EU and Japan, owing to prior agreements on lower sectoral rates. On the flip side, other major exporters to the US, including India and Singapore, now face increased uncertainty (chart 1). Adding to the pressure, Trump also introduced a $100,000 fee on new H-1B visa applications, disproportionately affecting Indian nationals and workers in IT-related sectors, though visa issuance had already been declining in recent months, partly due to seasonality (chart 2).

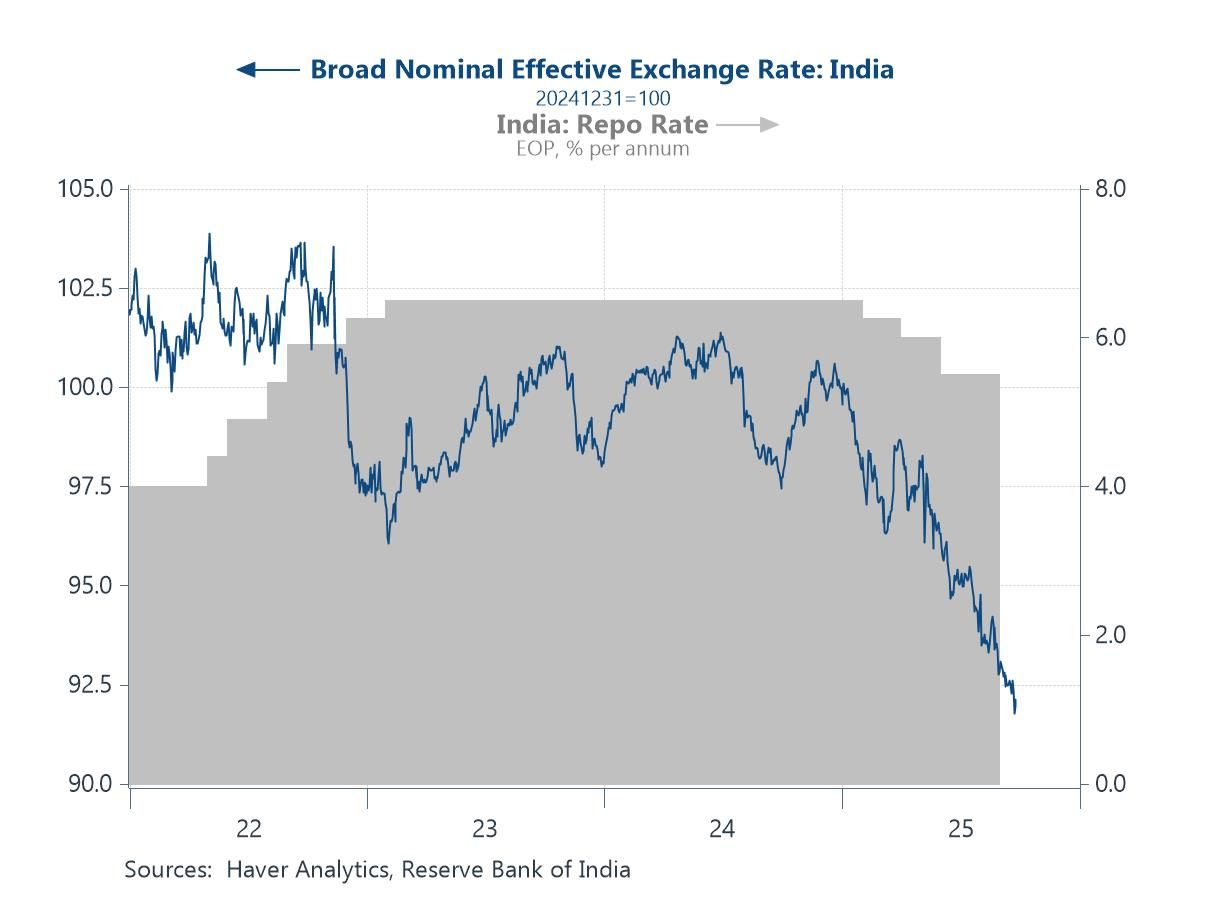

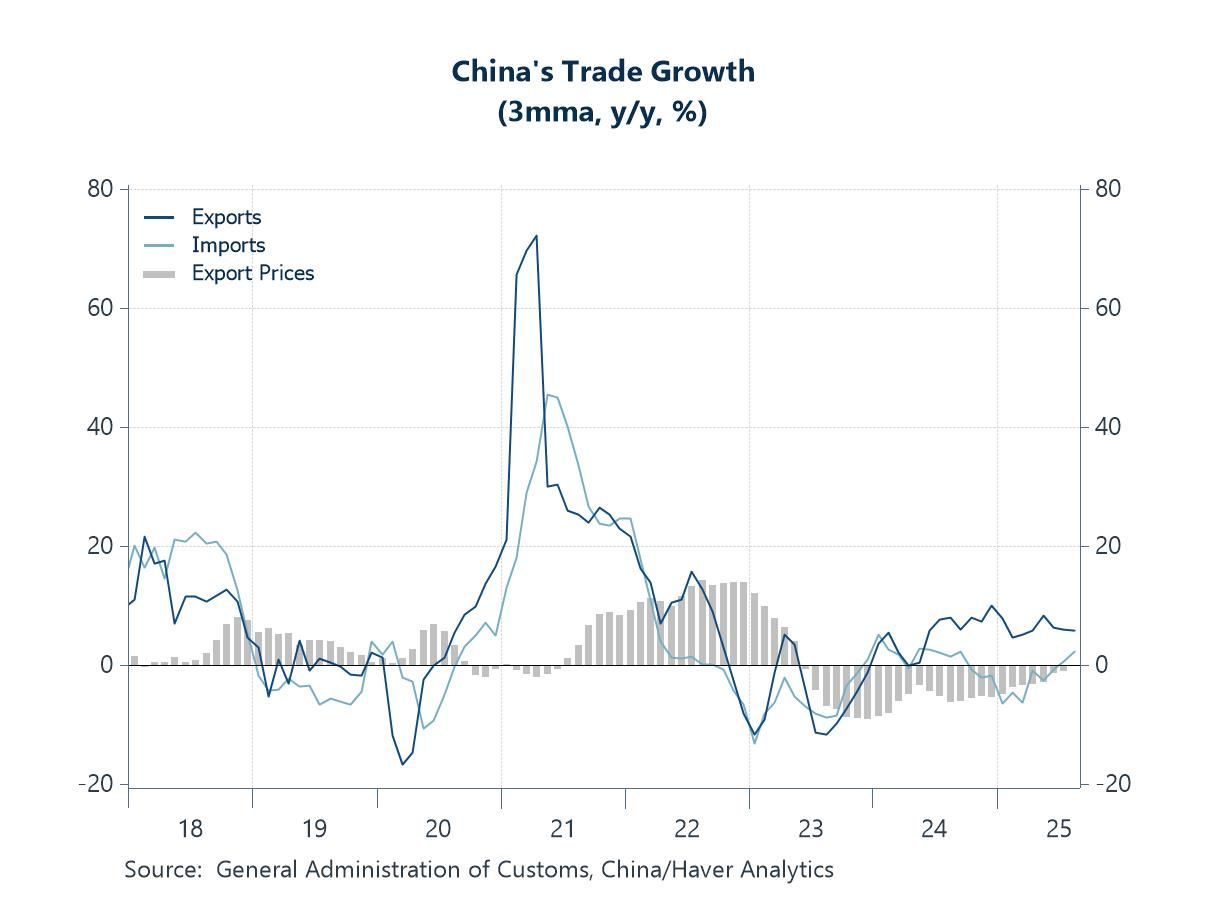

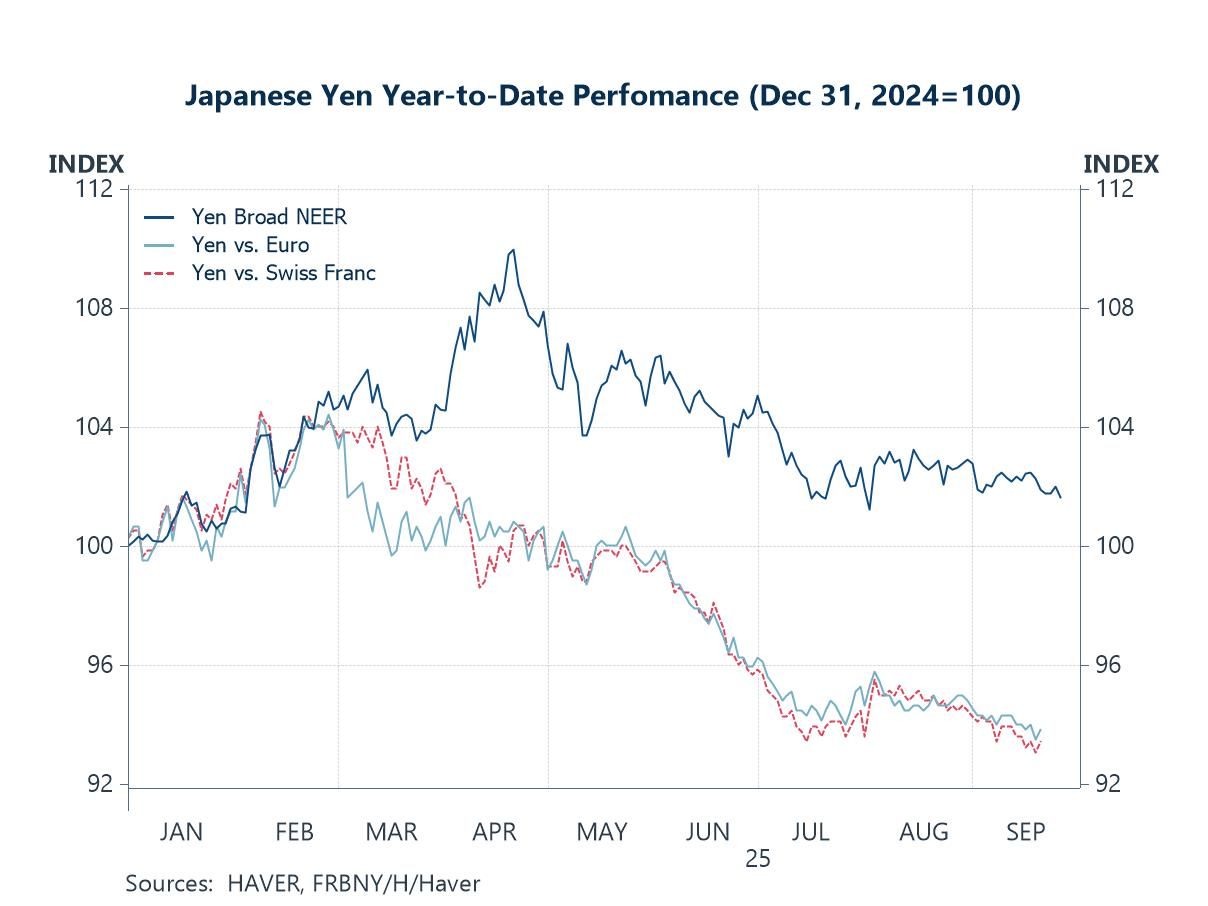

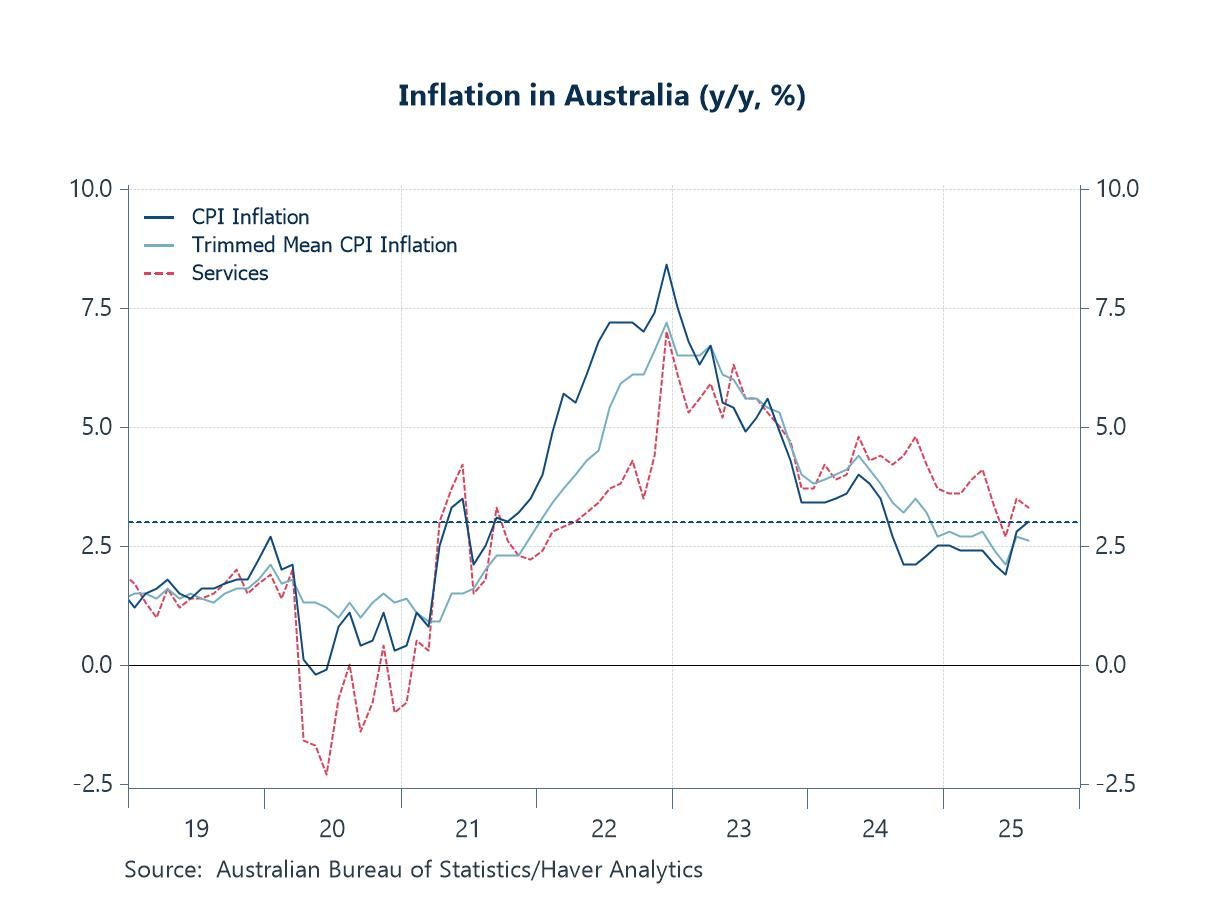

In India, the central bank meets this week and is likely to pause again on rate cuts, as concerns over rupee weakness (chart 3) take precedence despite lingering growth risks from US tariffs and other headwinds. In China, the government announced it will no longer seek Special and Differential Treatment (SDT) in future WTO negotiations—a significant policy shift. The move comes amid slowing trade growth (chart 4) and ongoing efforts to pivot toward a consumption-led economy. Japan has experienced moderate currency weakness (chart 5) as investors reassess central bank policy ahead of the ruling party’s leadership vote on October 4th. Australia also faces a monetary policy decision this week, with markets expecting a rate hold amid rising price pressures (chart 6) and signs of economic stabilization.

US pharmaceutical tariffs Last week, US President Trump announced new sectoral tariffs, imposing 100% duties on imports of brand-name or patented pharmaceuticals, effective October 1. This marks the first major tariff action in weeks, ending a brief lull in trade tensions. A key point of relief is that prior agreements with certain US trading partners, including the EU and Japan, provide exemptions, meaning the new steep tariff rate will not apply to them. In contrast, countries without such provisions will face the full 100% duty, which is likely to weigh on their growth through reduced export revenues. This includes major exporters to the US such as Switzerland and, in Asia, India and Singapore, among others (see chart 1). It should be noted, however, that the data shown below do not distinguish between generic and branded or patented pharmaceutical products. Additional points of possible relief include the fact that most of India’s pharmaceutical exports are generics, and that many exporters from Singapore already have plans to expand manufacturing capacity in the US.

Chart 1: US pharmaceutical imports

US immigration policy Also of recent concern is US President Trump’s move to impose a $100,000 fee on any new H-1B visa petitions submitted from September 21st. This measure aligns with the administration’s broader hawkish stance on immigration and is likely to raise varying degrees of concern across countries. Although the fee applies to all H-1B applications, its impact will be particularly pronounced for Indian workers, who accounted for 71% of total applications in fiscal year 2024. Chinese workers came at a distant second, at 11.7%. By sector, applications remained concentrated in IT roles. Even before this latest clampdown, H-1B visa issuance had already declined toward last year’s lows (see chart 2), though some of this may reflect seasonal patterns, as visa issuance historically often dipped in the early months of the year. The new fee has raised concerns over the cost of securing top global talent and fears that highly skilled workers may increasingly seek more immigration-friendly advanced economies, such as the UK, which has been exploring initiatives to attract skilled talent.

Chart 2: US non-immigrant visas issued

India Given ongoing growth risks from US trade policy, investors are now focused on the Reserve Bank of India’s policy decision this Wednesday, with expectations for another rate pause. While supportive for growth, any additional rate cut would make India’s yield differentials less favourable, putting further pressure on the rupee, which has already depreciated about 8% on a nominal trade-weighted basis, according to our calculations (chart 3). A persistently weaker currency could also create a feedback loop with foreign portfolio outflows, reinforcing further depreciation. At the same time, a weaker rupee has mixed effects: it can boost India’s export competitiveness, but as a net importer, it also raises the cost of foreign goods.

Chart 3: India’s repo rate and the rupee

China Moving to China, a major development last week saw the country announce it will no longer seek developing country Special and Differential Treatment (SDT) in current and future WTO negotiations. SDT benefits include longer implementation periods for agreements, enhanced trading opportunities, capacity-building support, and safeguards for developing countries’ trade interests. That said, China’s self-declared status as a developing nation remains unchanged. The announcement follows months of friction with the US, which has long criticized China for still benefiting from these advantages. While it resolves a key point of contention, significant US concerns remain over the sizable bilateral trade deficit and industrial overcapacity. On the domestic front, recent data showing slowing export growth alongside rising imports (chart 4) highlight a near-term challenge, as trade contributes less to overall growth. Although unfavourable in the short term, this dynamic also aligns with China’s broader shift toward a more consumption-led economy.

Chart 4: China’s trade growth and export prices

Japan Next, in Japan, investors are closely watching the ongoing leadership race for the ruling Liberal Democratic Party (LDP), as the winner is likely to become the country’s next prime minister. This week, attention will focus on candidates’ speeches and debates ahead of the party vote on October 4. Meanwhile, the yen has shown temporary weakness, particularly against the Euro and Swiss franc (chart 5), though it has held against the US dollar amid the latter’s recent decline. Recent yen weakness reflects investor reassessments of the Bank of Japan’s potential tightening path, uncertainty surrounding the leadership race, and its implications for Japan’s economic and fiscal outlook.

Chart 5: Japanese yen performance

Australia Lastly, in Australia, investors will watch the Reserve Bank of Australia’s (RBA) interest rate decision, though the central bank is widely expected to hold rates steady amid rising inflation pressures. Key measures, including the RBA’s preferred trimmed mean, have edged toward the upper target of 3%, while headline CPI rose 3% y/y in August, driven by a 24.6% surge in electricity prices. Tight labour market conditions continue to support elevated wage growth and buoy services inflation. Additionally, signs of stabilization in the broader economy following prior rate cuts may further deter the RBA from easing this week.

Chart 6: Australia inflation

Tian Yong Woon

AuthorMore in Author Profile »Tian Yong joined Haver Analytics as an Economist in 2023. Previously, Tian Yong worked as an Economist with Deutsche Bank, covering Emerging Asian economies while also writing on thematic issues within the broader Asia region. Prior to his work with Deutsche Bank, he worked as an Economic Analyst with the International Monetary Fund, where he contributed to Article IV consultations with Singapore and Malaysia, and to the regular surveillance of financial stability issues in the Asia Pacific region.

Tian Yong holds a Master of Science in Quantitative Finance from the Singapore Management University, a Master of Science in Analytics from the Georgia Institute of Technology, a Bachelor of Science in Mathematics from the Singapore University of Social Sciences, and a Bachelor of Science in Banking and Finance from the University of London.

More Economy in Brief